May consumption data is out.

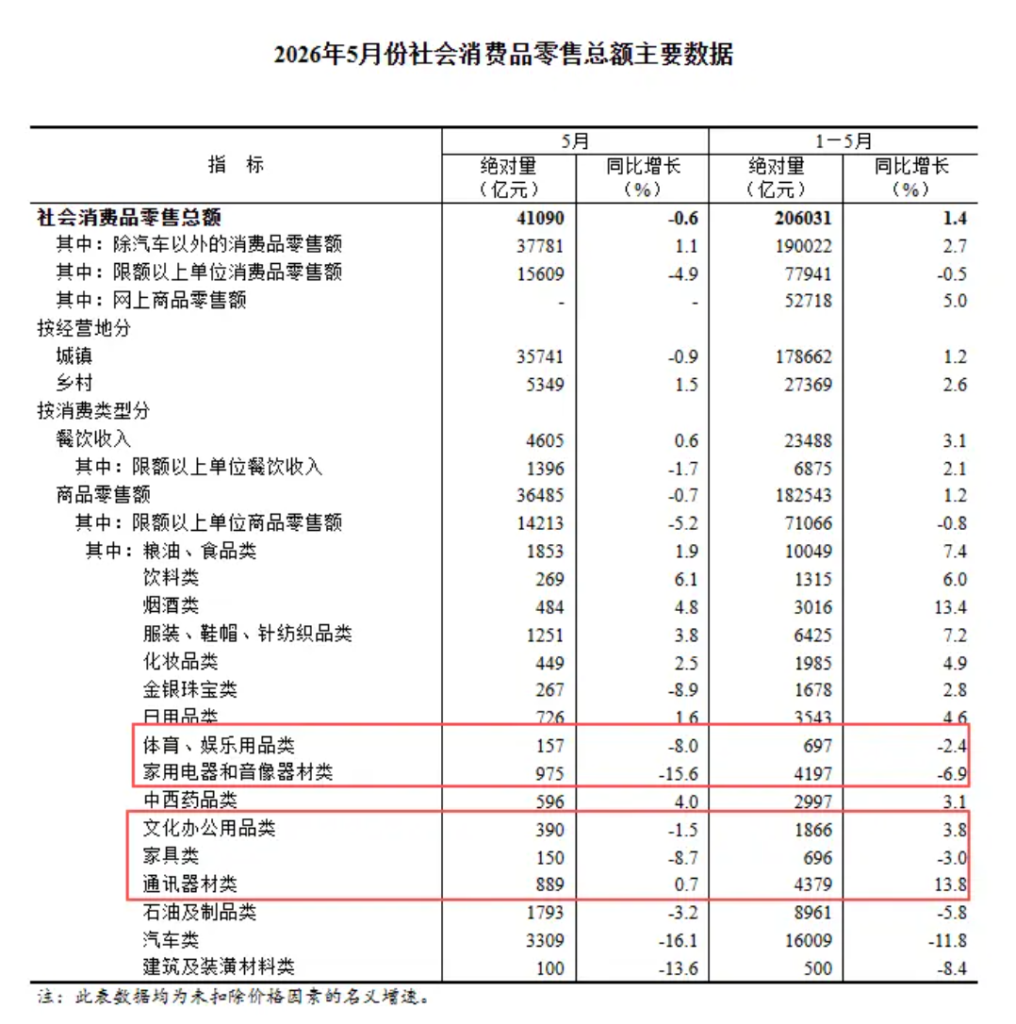

Total retail sales of consumer goods were 4.109 trillion yuan, a year-on-year decrease of 0.6%.

Market expectations were for flat or slight growth, but the reality is more than a little off. Year-on-year growth turned negative, and month-on-month also decreased by 0.38%.

To say it “exploded” isn’t to say it was good, but rather that in the history of statistics, total retail sales year-on-year falling below the zero line has only happened three times.

The previous two times were February 2020 and April 2022, both during COVID-19 lockdowns.

This time, there were no lockdowns, no large-scale physical blockades, the economy is operating normally, and the data has slipped on its own.

This fact alone gives this data extraordinary significance.

Where the significance lies is hard to elaborate on.

However, that such data can still be made public, discussed, and written about in articles means at least the era has not regressed.

The value of data has never been in whether it’s good or bad, but in its visibility.

Let’s break down the specific data first.

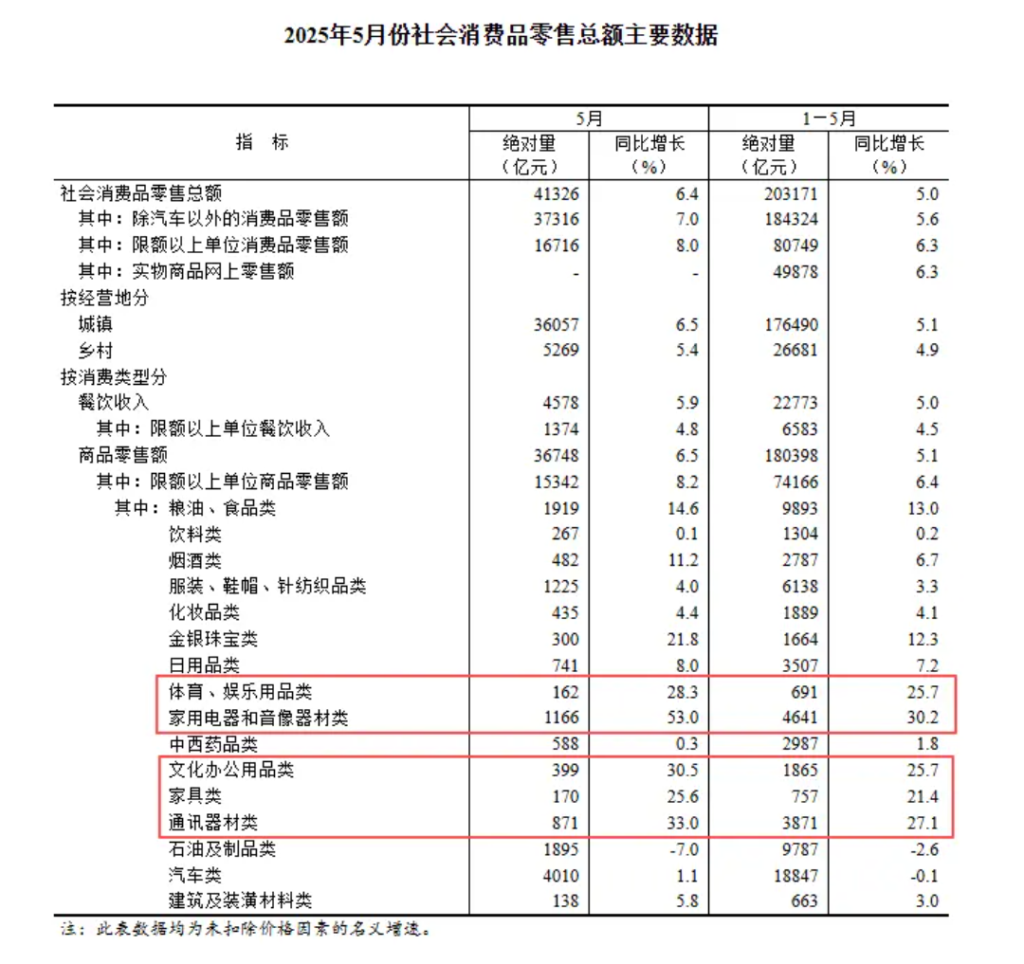

The biggest pitfall is still automobiles.

Automobile retail sales in May fell by 16.1% year-on-year. The monthly scale exceeded 300 billion yuan, with a deep decline and a large volume, directly dragging the overall market down.

Excluding automobiles, the growth rate of total retail sales was a positive 1.1%. This statement feels somewhat familiar.

Some say this indicates consumption is actually okay, but this metric itself is problematic.

We cannot simultaneously talk about new energy vehicle penetration exceeding 60% and the automotive industry “overtaking on a curve,” and then kick it out when calculating consumption.

Isn’t automobile a part of consumption?

Automobiles are the largest expenditure for most families besides housing. Their contraction is precisely the most direct evidence of consumption shrinkage.

Then, catering revenue only increased by 0.6%, and catering above a designated size even decreased by 1.7%.

The May Day holiday boosted service retail sales growth to 5.4%, but catering, the most fundamental indicator of daily life, is actually cooling down.

Holidays can create short-term peaks in travel and accommodation, but people won’t suddenly change their eating habits just because they had a few days off. Service consumption is resilient, but not strong enough to offset the decline in commodity consumption.

Home appliances fell by 15.6%, furniture by 8.7%, and building materials by 13.6%.

These three, taken together, correspond to the same story: housing.

From January to May, new home sales area decreased by 10.8%, new construction starts by 22.6%, and completions by 23.4%.

As long as the scale of real estate sales continues to shrink, there will be no improvement in demand for home appliances, furniture, and building materials. This is the long-tail effect of the real estate cycle, not something that can be recovered with one or two months of trade-in promotions.

Let’s look at urban and rural areas. In May, urban retail sales decreased by 0.9%, while rural areas grew by 1.5%.

The negative growth in urban consumption is more significant than the negative growth in the total figure, because urban areas account for the absolute majority of the total retail sales.

The weakening of urban consumption reflects adjustments in urban households’ expectations for employment stability and income growth, hesitation in large expenditures, and contraction in discretionary consumption.

Then let’s look at categories.

Cereals, oils, and food increased by 1.9%, beverages by 6.1%, and tobacco and alcohol increased by 13.4% cumulatively in the first five months.

Eating and drinking have not decreased, and have even increased.

But cars fell, home appliances fell, furniture fell, building materials fell. Communication equipment appears to have risen by 13.8%, but upon closer inspection, the price increase offset the decline in sales volume, meaning fewer units were actually sold.

In essence, it’s the same conclusion as before: necessities are rising, discretionary items are shrinking.

The more basic, the more stable; the more upgraded, the colder.

People aren’t not spending money, they are not spending big money.

Daily expenses continue as usual, but decisions like buying a new car, renovating, replacing home appliances, or purchasing large furniture, which require careful consideration, are being postponed.

Combined with CPI, this logic is further confirmed.

In May, CPI rose by 1.2%, lower than the market expectation of 1.3%, and core CPI even fell from 1.2% to 1.1%.

PPI, however, reached 3.9%, higher than expected.

The price increase of upstream raw materials pushed up PPI, but this price increase did not translate into vitality in consumer demand; instead, it became a cost burden for downstream enterprises.

CPI and social consumption growth are diverging – prices are rising, but volume is shrinking.

This is a typical picture of imported inflation superimposed with insufficient domestic demand.

The price increase in energy and core components is not due to strong demand, but due to supply-side tightness.

This type of price increase transmitted to the consumer side means passively accepting higher prices, rather than actively consuming.

Therefore, CPI appears to be rising, while total retail sales are probing downwards.

The policy direction of promoting price recovery is correct, but if the driving force behind price increases is cost-push rather than demand-pull, then the divergence between CPI and total retail sales will not end, and may even widen.

There is also a unique variable this year: the phasing out of subsidies.

May 2023 was one of the months with the strongest national subsidies. Home appliances, 3C products, and automobiles – anything that could be subsidized was subsidized, giving consumption a concentrated boost that month.

Here’s a look at last May’s total retail sales data: a year-on-year increase of 6.4%, a scene of vigorous vitality and flourishing development….

This left a very high base for this May. Therefore, the turn to negative growth this month is understandable.

More importantly, subsidies have a pulling-forward effect.

Last year’s concentrated subsidies brought forward some consumption that should have occurred this year to last year. This year, the subsidy intensity is not as strong as last year, so this year faces a double blow: not only is there no subsidy support, but also that money that should have been spent today is gone.

If we view subsidies as a policy cycle, it generally looks like this:

Low investment in the germination phase, heavy investment in the high-growth phase, and gradual withdrawal of subsidies as competition intensifies.

We are currently in the final stage.

New energy vehicles are the most typical example – for the past few years, a considerable portion of automakers’ profits came not from selling cars, but from subsidies.

As subsidies phase out and car prices fall, consumers are more willing to wait, because the later they buy, the cheaper it will be.

This is typical consumption postponement under deflationary expectations.

The 16.1% drop in automobile sales in May is not entirely due to subsidies, but the phasing out of subsidies is definitely an accelerating factor.

Let’s also bring in the export data for May, and the picture becomes even more striking.

In May, exports increased by 19.4%, exceeding expectations, with exports to the US increasing by a large margin of 37%.

It’s still strong external demand and weak domestic demand.

Strong exports have been a great help. Without export support, the impact of insufficient domestic demand on employment and CPI would be more direct.

However, export growth is mainly concentrated in price-increasing categories like chips, while labor-intensive categories are experiencing negative growth across the board.

The growth in export value has not translated into employment and income for ordinary workers. This is typical “jobless growth.”

Factories have earned foreign exchange, but workers on the assembly lines have not earned more wages to spend.

So the problem becomes a cycle:

Weak consumption leads to weak employment; weak employment leads to weak income expectations; weak income expectations lead to even weaker consumption.

This cycle didn’t start in May; it’s been going on for a while.

Breaking it requires ensuring workers have more stable incomes and more time to consume, not just good-looking export data.

Returning to the initial qualitative assessment of the data: in a period of normal operation, total retail sales have fallen below the zero line on their own for the first time. This fact will not be diluted by any explanation.

We say “normal operation” because there were no force majeure events this month.

Factories are running, ports are busy, May Day holidays were observed, 618 (a major shopping festival) is being prepared for, everything seems to be proceeding as planned.

But beneath these normally operating machines, residents’ consumption behavior has undergone a substantial contraction.

Consumption that doesn’t involve going out is rising, while large-ticket items that require loans and the mortgaging of future income are shrinking.

This is everyone voting with their wallets, and when the votes add up, they become total retail sales.

What’s next?

In the third quarter, the base effect of last year’s national subsidies will fade, and the year-on-year data for total retail sales may improve.

However, don’t expect too much improvement in magnitude, because the base for the same period last year was itself boosted by policies, not a naturally formed low point.

The base effect game can only solve the problem of year-on-year readings, not the problem of insufficient consumption capacity.

Until then, act within your means. Both investment and consumption.

End of article. Thank you for reading. If you found it helpful, please like, share, and in-watch.

-end-

A final note: I’ve created a ‘Planet’ community group that has been running for 600 days. Friends with similar values are welcome to join.

Every day, I share some of my observations and thoughts in the group, and you can also ask me questions, and we can progress together at a steady pace, enjoying uniform progress.

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.