本文全面阐述我对中国经济的观点。

全文约3万字,撰写花了我14个月。阅读需要60分钟。如果完全读懂,能受益30年。

一个人的命运固然要靠自身的奋斗,但也要考虑历史的进程。我们这些普通人,无法选择自己生活的年代,更无法对抗历史趋势。历史的车轮滚滚驶过,掀起的一粒灰尘,对个人来说可能便是一座大山,导致灭顶之灾。所以必须看清历史趋势、少踩坑。而决策者如果能认清经济在历史趋势中的位置,出台恰当的政策,避免不恰当的政策,少走弯路,就可以泽被苍生了。

引言:为什么要撰写本文?

我希望通过本文,阐述以下问题:

1、中国经济是如何陷入到今天这样的困境的?

2、不恰当的财政政策和货币政策,是如何助推经济走差的?

3、为什么说中国经济已经陷入“腹背受敌阶段”?

4、这个阶段具有什么特征?

5、对资本市场有什么影响?

6、政府应该如何延缓投资回报率的下降?

7、普通人如何应对?

从2022年初开始,中国经济快速陷入资产负债表衰退,出现螺旋下降的通货紧缩;房地产崩盘:价格大跌,居民大面积断供弃供,房企濒临倒闭,酝酿着金融风险;各行业倒闭企业增多,失业率明显上升;财政收入增速下降。

2022年四季度,中央放弃疫情封控政策、放松房企融资政策。所有人都以为,会出现“报复性消费”,经济很快就会修复。但事与愿违。2023年初至今(2024年7月),消费增速一直很弱,企业投资意愿持续低迷;PPI持续大幅负增长,CPI在0附近徘徊,处于通货紧缩状态(点击);M1、M2、社会融资规模、信贷余额同比增速等指标迭创新低;人民币汇率贬值压力巨大;货币政策效果日益下降,财政政策动作缓慢;目前中央、地方财政收入同比都是负增长,国税部门为了增收,倒查税收;地方政府债务压力巨大,无力进行民生投资,纷纷预征过头税,或者增加行政罚没款;房地产调控政策已经彻底放开,并且2024年5月17日开始试图通过降低首付比例和按揭利率来刺激居民购房,但效果堪忧(点击);全社会弥漫着悲观的气氛,自杀、恶性案件增多。

总之,如果说2022年之前,中国经济行驶是在相对平静的河面上航行,那么2022年之后就是在激流险滩上跌宕起伏,险象环生。

面对这样的经济困境,出现了各种各样的声音。官媒认为关键在于居民和企业“缺乏信心”,却说不出为什么会缺乏信心;体制内的学者连发生了“资产负债表衰退”和“通货紧缩”都不敢承认,有的“学者”还受命在媒体上发文,说根本没发生“资产负债表衰退”,简直是掩耳盗铃,自欺欺人;金融机构的首席经济学家们受到严格的监管,不能对外公开提及“衰退”、“通缩”等敏感词语;也有人在幻想新一轮库存周期或产能周期会很快启动,带来股市大牛市。

学术界不对这些问题发表正确的见解,不知不觉就把话语权让给了缺乏专业素养的自媒体作者。这些人为了吸引眼球,胡编乱造一些缺乏常识、毫无逻辑的观点,冠以骇人听闻的标题,到处传播,把仇恨的矛头引向金融行业、资本、外国人,来误导民众,激发民粹主义甚至极端民族主义(点击)。这对解决经济问题有弊无利。

官员们对经济陷入困境的原因,要么缺乏清晰的认识,懵懵懂懂;要么抱残守缺,心存幻想;要么心知肚明,却无能为力。而没有正确的认识,就无法做出正确的决策。有的地方官员以为,居民不消费是因为缺乏消费场景,只要组织烧烤节、夜市街就能拉动消费;地方政府为了度过财政困难,在应该放水养鱼时,却预征过头税、罚没款,破坏营商环境,并纷纷提高公用事业价格(点击1、2);央行应该大幅降息,却犹豫不决、缩手缩脚,导致实际利率居高不下(点击1、2);中央财政应该尽快大幅加杠杆,却瞻前顾后、畏首畏尾;在应该大力刺激消费时,以为发放一点补贴就能带动居民采购耐用消费品、带动企业更新设备。

显然,这些做法只会浪费更多时间,走更多弯路。必须先搞清楚中国经济的症结在哪里,然后才能对症下药,避免浪费时间,错过时机,做无用功。

2023年5月,我开始思考经济为什么难以修复的问题,逐渐从以前习惯用凯恩斯主义和货币主义理论分析问题,转向用真实经济周期理论分析问题。循着这个思路,可以完美地解释近年来中国经济的所有现象。随后我围绕着这个思路,撰写了十几万字的研究报告。

2023年初,辜朝明的新书《被追赶的经济体》中文版上市。我发现可以把他的“资产负债表衰退”、“被追赶的经济体”概念都纳入到我的分析框架下。在我的框架下,必然可以推出这两个经济现象。

2023年3月中旬,我计划将这些思路和观点汇总成一本书。但随后家里连遭变故,不得不每日奔波于医院之间,只能挤出一些碎片时间做研究。

本文是对已经完成部分的汇总。限于篇幅,以阐述观点为主,具体的逻辑、数据、图表、论证和参考文献,都放在文中带下划线的超链接里,可以点击查看。还有更多问题有待深入讨论。

一、宏观经济分析框架:以TFP和自然利率为核心

(一)分析框架

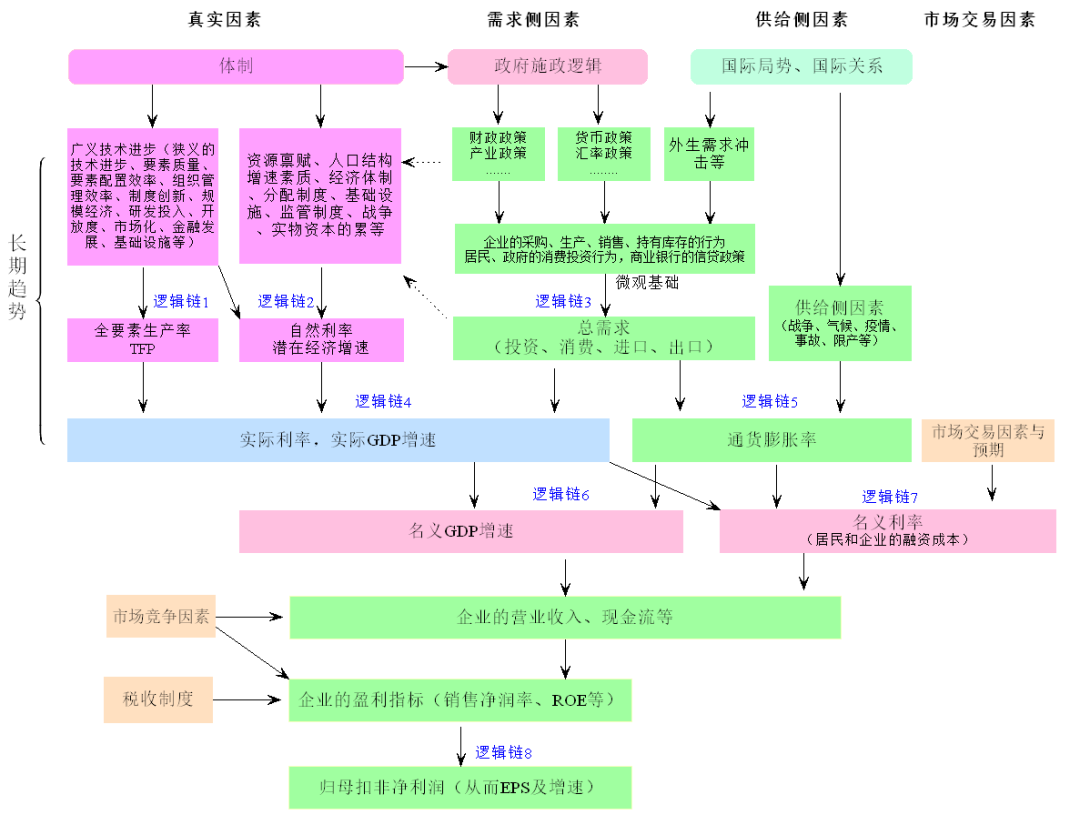

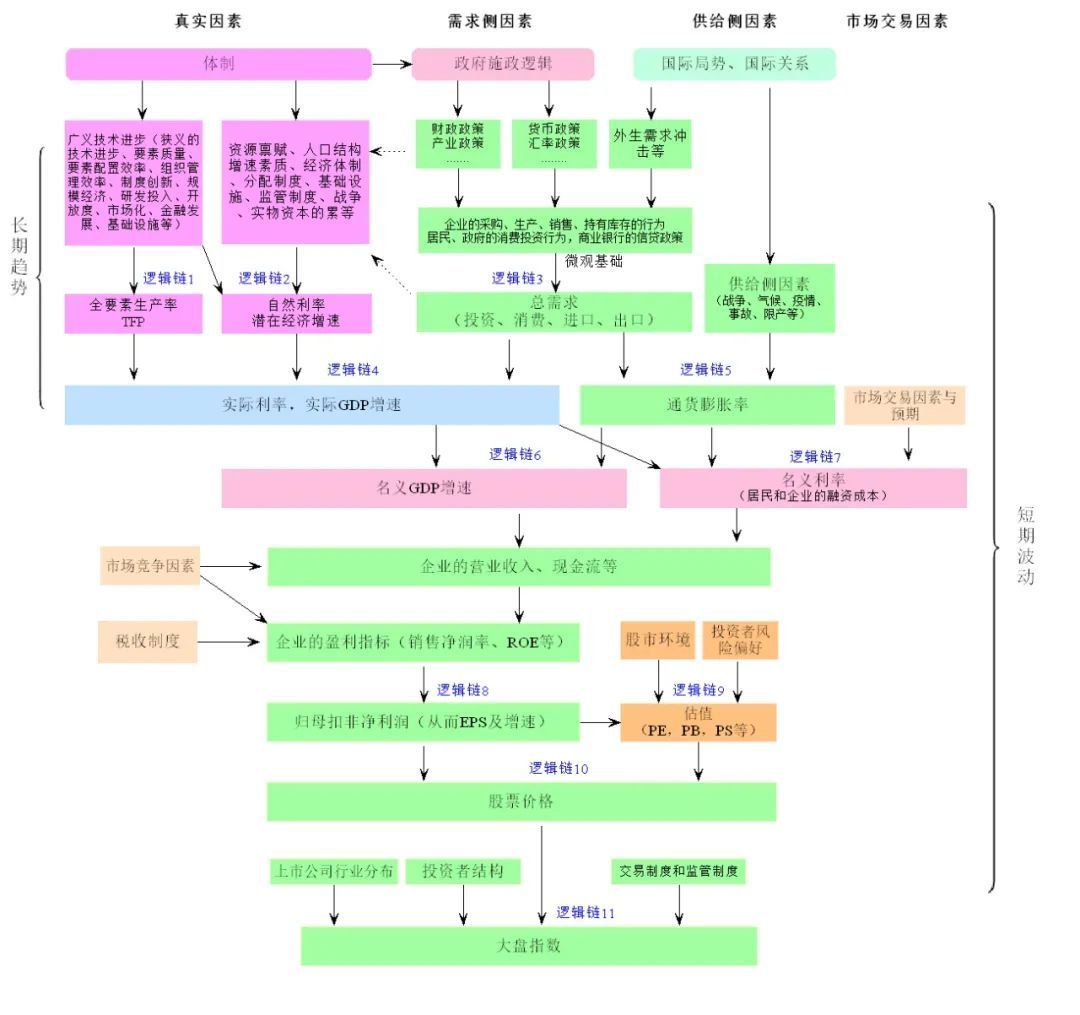

为了清楚地说明问题。首先介绍我分析中国经济的框架(图1)。具体来说:

逻辑链1:长期内,广义的技术进步(包括狭义的技术进步、要素质量、要素配置效率、组织管理效率、制度创新、规模经济、研发投入、开放度、市场化、金融发展、基础设施等)决定全要素生产率(TFP)。

逻辑链2:长期内,经济中的真实因素(广义的技术进步、资源禀赋、人口数量质量结构、经济体制、分配制度、监管制度、战争、资本积累等)决定自然利率和潜在经济增速。

逻辑链3:短期内,需求侧因素(财政政策、货币政策、产业政策、外生的需求冲击等等)决定企业的采购、生产、持有库存、销售行为,商业银行的信贷政策,居民和政府的投资和消费行为。这些是宏观经济的微观基础。进而决定总需求的短期波动。

逻辑链4:慢变量(TFP、自然利率)决定现实中的实际利率和GDP的长期趋势;短期快变量(总需求)决定现实中的实际利率和GDP的短期波动。

逻辑链5:短期内,供给侧因素(战争、气候、疫情、事故、限产等)与总需求一起决定通货膨胀率。

逻辑链6:短期内,实际利率、实际GDP增速、通货膨胀率一起决定名义GDP增速。

逻辑链7:短期内,实际利率、通货膨胀率、市场交易因素与预期,一起决定名义利率。

逻辑链8:名义GDP增速、名义利率、市场竞争因素等一起决定企业的营业收入、现金流情况。进而与税收制度一起决定企业的盈利指标(销售净利率、ROE等)。进而决定企业的扣非归母净利润,从而决定企业的EPS、EPS增速。

这些逻辑链(传导机制)在学术上都是无懈可击的,详细的讨论和分析见这里。

图1 分析宏观经济的框架

资料来源:自己绘制

这个分析框架的特点是:

1、将真实因素纳入分析,抓住了经济增长的最本源。

面对中国经济的乱象,有人认为是总需求走弱导致的,有人认为是经济结构不合理导致的,有人认为是资产负债表衰退导致的。在我看来,这些都是表象。

根源在于:改革滞后;国企民企二元结构扭曲资源配置,导致低效率;创新能力不足;人口老龄化、人口结构恶化;要素成本上升;地区、行业发展不平衡;等等。这些共同导致实体部门投资的边际回报率下降。要解决问题,必须从真实因素着手,才能够治本。

2、以全要素生产率和自然利率为核心,投资的边际回报率贯穿始终

在图1中,真实因素决定TFP和自然利率,进而决定了经济中的所有回报率(名义利率、实际利率、企业净利率、ROE等等)。核心是TFP和自然利率。

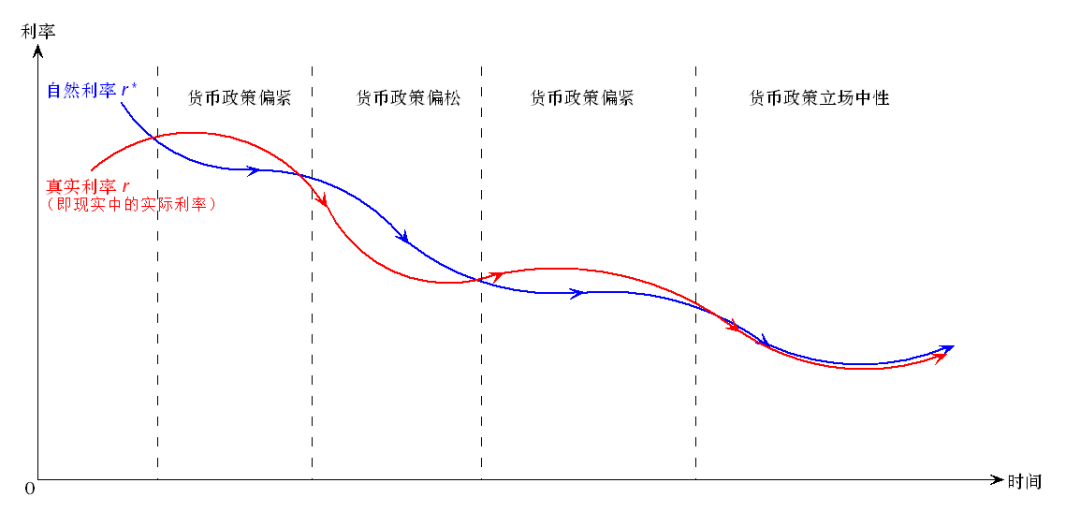

自然利率本质上是经济处于均衡状态下资本的边际投资回报率,它是经济的真实因素决定的,与货币政策本身和价格因素无关。

自然利率是衡量货币政策宽松程度的标准,或者说是货币政策的锚。如果自然利率高于现实中的实际利率,则货币政策是紧缩的;如果自然利率低于现实中的实际利率,则货币政策是宽松的;如果二者相等,则货币政策是中性立场。点击1、2、3、4可以查看相关观点、讨论和参考文献。

整个分析框架都以全要素生产率和自然利率为核心,它们的变化决定了所有的经济现象。

图2 自然利率作为货币政策的锚

资料来源:自己绘制

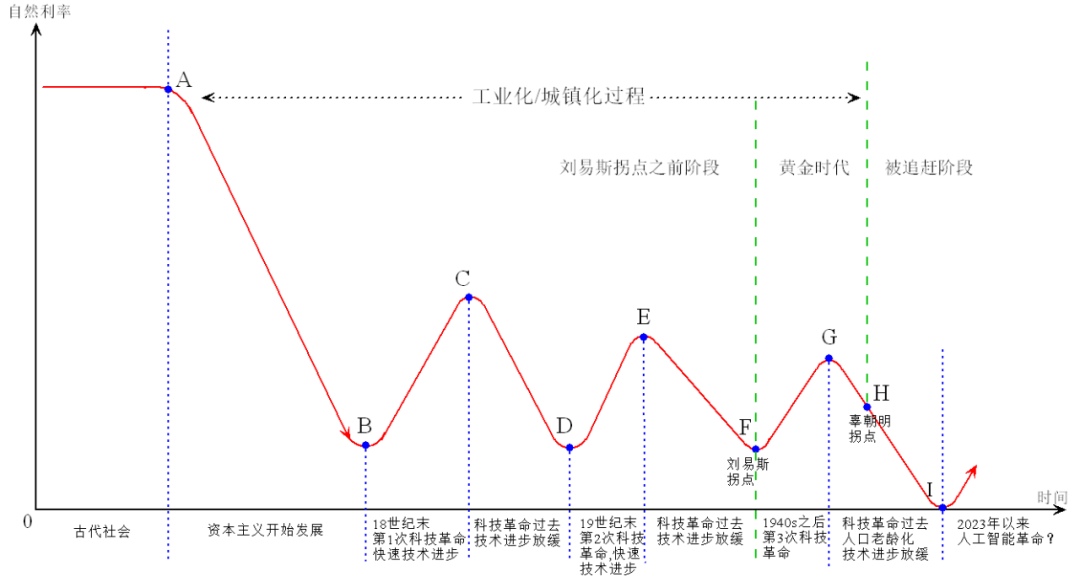

(二)自然利率的长期趋势:从公元前到AI科技革命

一个“典型”国家的自然利率长期趋势可以如下(点击查看具体论证):

图3 自然利率的长期趋势

资料来源:自己绘制

在漫长的封建专制时代,它的自然利率水平很高(点击查看原因)。

17世纪,它像英国一样进入资本主义社会,市场经济得到快速发展。同时开启了工业化/城镇化过程,大量农村剩余劳动力开始向城市转移。随着资本主义的发展,金融机构、金融组织、金融制度、金融市场逐渐完善,自然利率不断下降。

到18世纪末期(图3中B点),它像英国、西欧一样开始第一轮科技革命,进入蒸汽时代。技术进步带来了投资回报率的快速上升,自然利率从B点反弹到C点。这次科技革命在1840s结束,机器大生产成为普遍现象。

1850s之后,随着蒸汽革命过去,技术进步放缓,投资的边际回报率下降,自然利率从C点下降到D点。这正是马克思(1818-1883)和恩格斯(1820-1895)生活的年代。他们观察到资本家的投资回报率在下降,将其当作资本主义的普遍规律,并且认为无法解决。他们观察到无产阶级处于非常悲惨的境地,贫富差距在急剧扩大,认为这必然会激起无产阶级的反抗,资本主义制度必将灭亡。不过辜朝明(2023)认为,贫富差距扩大是经济在城镇化/工业化过程中,跨越刘易斯拐点(F点)之前必然出现的现象。

到19世纪末,它像美国、西欧一样开始第二轮科技革命(电气革命)。这次科技进步带来了投资回报率的上升,自然利率再度反弹,从D点反弹到E点。这是熊彼得(1883-1950)生活的时代,他观察到了创新对生产率的极大提升,于是非常推崇创新的作用,将其加以理论化。

第二次世界大战之后,1950年前后,这个经济体像美国一样开始第三轮科技革命(核能、电脑、空间技术、生物工程等)。技术进步使自然利率从F点反弹到G点。到了1960s,技术进步速度逐渐放缓,自然利率从G点开始下降。

到1970s,它像美国一样,技术进步速度放缓,要素成本上升,人口红利消失,自然利率下降。此后2008年金融危机、2020年疫情,都使它的自然利率降得更低,接近于0,甚至是负值。

从2022年底、2023年初开始,人工智能技术有了突破性的进展,人们将其视为新一轮科技革命,认为能带来生产效率的提升。如果真的是这样,那么自然利率将从I点再度反弹,但是目前尚不确定。

图3是一个典型的经济体,现实中每一个经济体都可以在图3中找到自己所处的阶段。迄今为止,学术文献揭示,1960s之后的美国、加拿大,1970s之后的欧元区、1980s之后的日本、1990s之后的韩国、2000s之后的中国以及其他各国,自然利率是普遍下降的。原因在于,它们研究的恰好是第三次科技革命之后、技术进步放缓的阶段。

自然产出(潜在GDP)增速的趋势,与自然利率的趋势基本上是相同的。

从图3还可以看出,自然利率的上升和下降阶段持续的时间很长,长过一个人的一生。政府(决策者)可以决定一部份真是因素,例如通过体制改革、基础设施建设、鼓励创新和技术进步等,提高自然利率,延缓它的下降,但很难扭转它的长期下降趋势。个人更难与它的长期下降趋势对抗。

所谓“一个人的命运固然要靠自身的奋斗,但也要考虑历史的进程。”用在这里恰如其分。我们这些普通人,无法选择自己生活的年代,更无法对抗历史趋势。历史的车轮滚滚驶过,掀起的一粒灰尘,对个人来说可能便是一座大山,导致灭顶之灾。因此必须看清历史的趋势、少踩坑。而决策者如果能认清经济所处的位置,出台恰当的政策,避免出台不好的政策,就可以泽被万民了。

(三)辜朝明的理论作为上述分析框架的一部分和必然结果

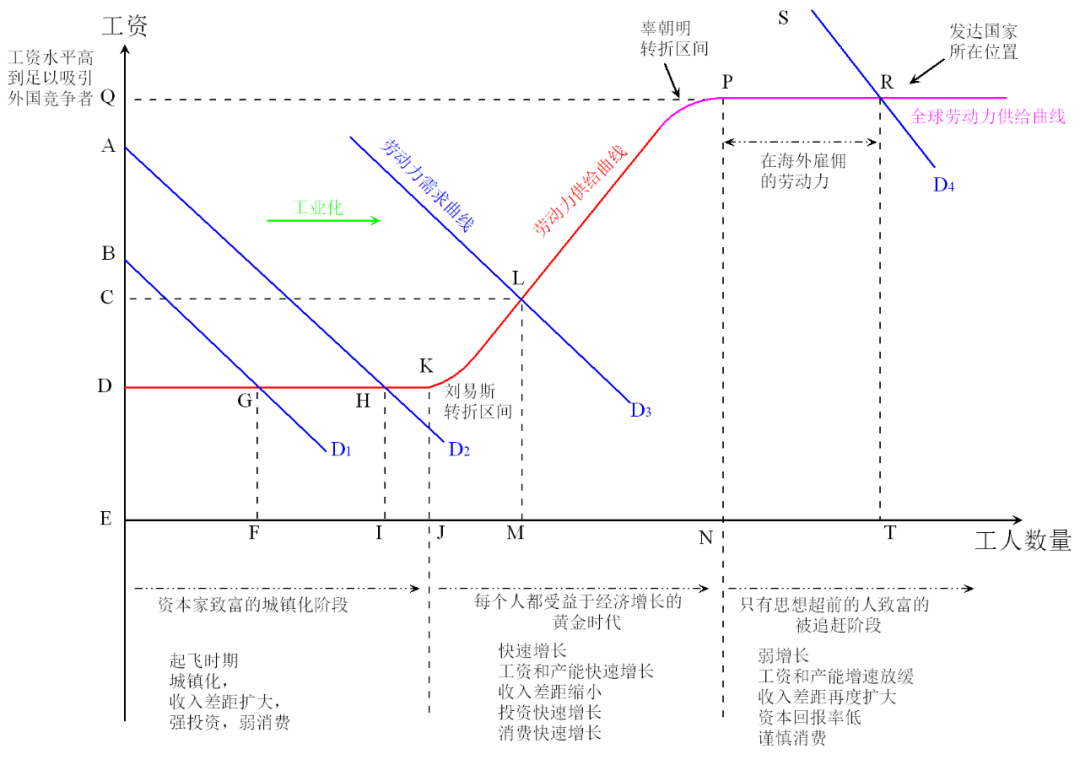

辜朝明(2008,2023)提出了“资产负债表衰退”、“被追赶的经济体”等概念。在辜朝明(2023)中,他拓展了刘易斯(William A. Lewis,1954)的“二元经济”发展理论,提出了“被追赶的经济体”(Pursued Economy)的概念,把工业化/城镇化过程划分为三个阶段(点击),分别是:

1、刘易斯拐点前的“城镇化阶段”

在经济达到刘易斯拐点(图3中F点,图4中K点)之前,农村劳动力无限供给,但工资基本不上涨。在这一阶段,厂商获得的报酬总额增速远高于劳动力获得的报酬总额增速。并且由于厂商的人数远远少于工人人数,因此厂商快速完成资本积累,工人则只能维持较低的收入水平,消费能力有限,贫富差距会扩大,收入不平等加剧。

2、跨越刘易斯拐点之后的“黄金时代”

当经济跨越刘易斯拐点之后,企业为了扩大再生产,不得不提高工资水平,于是居民收入上升,消费能力得到提升,贫富差距缩小。所有人都从经济增长中受益,甚至低学历、缺乏技能的人也很容易找到工作,投资和消费都比较强劲,人们对未来预期非常乐观。因此辜朝明将这一阶段称为“黄金时代”。

在这一阶段,由于企业和居民对贷款需求旺盛,很容易推高货币乘数,因此货币政策非常有效,容易出现通货膨胀。而财政政策由于会挤出私人部门投资,因此效果有限。只有在发生资产负债表衰退时,财政政策才比货币政策有效。

3、“被追赶的阶段”

随着国内劳动力逐渐被吸纳,工资上升,导致企业生产成本上升,利润率下降。对应图3中,自然利率降低到H点。相比之下,一些比本国经济起飞较晚、比较落后的经济体存在大量剩余劳动力,工资和其他要素价格低,投资回报率高。因此企业开始“出海”,去后进国家投资。

企业出海投资,一方面导致本国经济增速放缓,消费增速下降,只有那些具有创造力、能够通过学习提高自身能力的人才能获得高收入,而那些不能适应发展的人(尤其是被其他国家竞争对手替代的制造业的工人)将失业。于是贫富差距再度扩大。另一方面会带动落后国家经济开始起飞,追赶先进国家。因此辜朝明将这一阶段称为“被追赶的阶段”。表现在图4中,即劳动力需求曲线移到了D4,与水平的“全球劳动力供给曲线”交于R点。

为了方便,我参照“刘易斯拐点”,把图4中的P点称为“辜朝明拐点”。

经济体处于“被追赶阶段”时,国内缺乏投资机会,企业融资意愿低,居民消费意愿低。换言之,国内储蓄大于投资,利率下降,甚至利率降到很低都无法吸引投资,货币政策的效果大大下降。此时财政政策不会挤出私人部门投资,因此财政政策效果更好。如果恰好又发生资产负债表衰退,就更是如此。

图4 对辜朝明(2023)“被追赶的经济体”框架的改进

资料来源:自己绘制

辜朝明没有深究经济陷入“资产负债表衰退”和“被追赶阶段”的根源。图3已经展示了我的观点,即根源是真实因素导致投资回报率下降。例如在图3中,当自然利率下降到H点时,国内投资回报率下降,也缺乏低成本的劳动力,导致企业在国内投资无利可图,只好出海投资,造成本国制造业空心化。也正是因为投资回报率下降,经济特别容易发生“资产负债表衰退”(详见下文)。

以中国为例:

在1978年之后,制度变迁释放的制度红利、低廉的要素价格、学习国外的技术和管理经验、大量的要素投入、人力资本的发展等真实因素,共同带来了广义技术进步;进而导致TFP增速、潜在GDP增速、自然利率上升;进而带来了现实中GDP增速上升、较高的投资回报率。这个过程,也就是工业化过程;也是农村剩余劳动人口不断向工业部门转移,推进城镇化的过程。

但是2008年之后,TFP增速下降到0附近(点击);2000年之后,自然利率一直在下降;2010年之后,潜在GDP增速逐步下降;最终带动现实中GDP增速下降,边际回报率下降。2004-2012年之间,人口红利逐渐消失,跨越了“刘易斯转折区间”,劳动力成本开始快速上升。

从2010年至2021年,自然利率和潜在GDP增速虽然在下降,但下降比较缓慢。由于房地产、基建、出口的拉动,以及新兴产业的崛起,GDP增速还算较高,工人工资上升。这就是辜朝明(2023)说的“黄金时代”。

但是2022年的疫情封控,严重压低了中国的TFP增速、自然利率和潜在GDP增速,使经济陷入了资产负债表衰退(点击)。叠加人口老龄化,投资边际回报率快速下降,迫使企业加快出海,经济跨越“辜朝明拐点”,进入“被追赶阶段”,或者说进入了前有围堵(美日欧),后有追兵(东南亚、南亚、拉美)的“腹背受敌阶段”(点击)。

换言之,辜朝明只指出了“资产负债表衰退”和“被追赶的经济体”现象,没有深究其根源。而按照我的框架,秉承真实经济周期理论,认为随着真实因素决定的投资回报率下降,到一定程度时,经济必然陷入“资产负债表衰退”,或进入“被追赶阶段”。这样辜朝明的范式就成为我的分析框架的一部分,“资产负债表衰退”和“被追赶的经济体”就成为我分析框架的必然结果。

二、中国经济是如何陷入当前的困境的?

(一)2022年的严格封控,压低了自然利率和自然产出(点击)

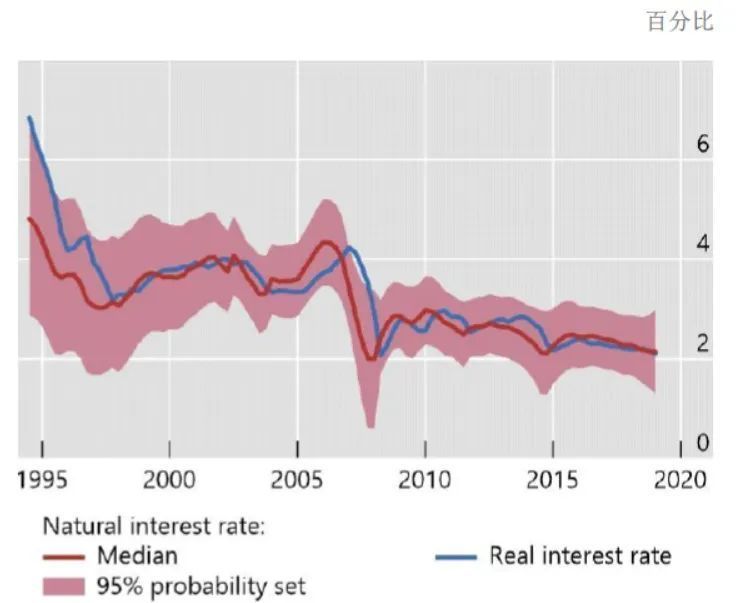

在2020年之前,中国自然产出(潜在GDP)增速大约是6%。按照孙国峰和Rees(2021)的估算,2000s初中国自然利率约为4%,2019年底降到约2%。

图5 中国的自然利率

资料来源:孙国峰和Rees(2021)

在2020年一季度,中国经济短暂地受到疫情的影响。到2020年5月,疫情就得到了控制,经济基本恢复正常。此后欧美陷入疫情,经济活动停摆,供应链中断,对我国商品需求增加,我国出口大幅增长。因此直到2021年底,中国经济增速都还不错。

但是,2022年初,欧美经济逐步正常化,对我国商品的需求下降。同时Omicron开始在我国蔓延。面对这一传染性强、毒性下降的变种,我国没有及时放松封控政策,而是更加严格地封控。各地纷纷实施了严格的、长期的封控,压低了TFP增速、自然利率和自然产出增速。主要传导机制包括(点击查看详细分析):

1、迟滞效应(hysteresis effect)导致企业投资开支和研发开支下降。

2、大量人力物力财力投入疫情防控,导致投入生产、研发的要素减少。

4、疫情防控导致全要素生产率下降。

5、导致居民边际消费倾向下降。

6、疫情期间劳动人口下降,人口老龄化加快,少子化加重。

7、劳动参与率下降。

这些传导机制与2008年金融危机类似,使TFP增速、自然利率、潜在GDP增速下了一个台阶。在2023年7月,我认为中国的自然产出增速已经下降到了5%左右,自然利率被压低到了1.5%甚至以下(点击)。

这样,2022年以来,经济陷入“资产负债表衰退”,企业边际投资倾向、居民边际消费倾向下降,人口老龄化延续,技术进步继续放缓,国进民退导致的低效率继续存在,因此自然产出增速、自然利率还在继续下降。

(二)严格封控和行业整顿政策,推高了自然失业率(点击)

2020年以来,尤其2022年以来的疫情、封控政策及迟滞效应还推高了我国的自然失业率,传导机制如下:

1、疫情封控导致人员流动不畅,信息不畅,推高摩擦性失业;

2、疫情期间的产业结构变化、技术进步,导致部分人失业;

3、实施了行业整顿政策,包括:

【1】2020年开始整顿平台经济,到2022年4月29日的政治局会议,告一段落。

【2】2021年开始整顿教育培训行业,到2022年告一段落。

【3】2020年8月央行、银保监会等机构针对房地产企业提出“三道红线”指标,限制房企融资,一方面导致大量房企无法融资,濒临倒闭,只好于2022年10月之后又放开房企融资;另一方面,没有及时放松限购限贷,导致房价暴跌,居民资产缩水,资产负债表恶化,一直到2024年5月17日才基本放开。

【4】2023年开始整顿金融行业。

这些整顿政策中,有的有民粹主义的意味。对房地产调控过头之后又没有及时调整。这些整顿政策恰好与疫情重叠,使这些行业运行受到双重打击。在行业整体萎缩和人员流动不畅的情况下,这些专业性较强、就业面较窄的失业者很难再就业,推高了结构性失业。

4、企业的理性选择(往届生困境)

疫情导致应届毕业生就业困难,毕业即失业,只能在家啃老,考研或考编。疫情过去之后,他们再找到专业对口工作的难度会成倍增加,因为:【1】企业会怀疑他的能力;【2】他毫无相关工作经验,只能当应届生用;同时他又有一定的社会经验,企业会觉得不如应届生好管理。这在企业看来是最优的理性选择,但客观上导致了结构性失业上升。

5、迟滞效应。

疫情导致短期经济波动,进而导致劳动力失业,不仅他的工作意愿受到打击,还可能失去工作技能,导致他难以再就业,永久地退出劳动市场。即自然失业率上升了。

自然失业率的上升一直持续到现在,目前很可能还在上升。2023年7月,国家统计局发布2023年6月城镇16-24岁青年调查失业率高达21.3%。2023年 8月开始停止发布该数据,对统计口径进行调整。2024年1月开始发布城镇16-24岁青年(不含在校学生)调查失业率,2023年12月是14.9%,2024年5月是14.2%。从草根了解来看,实际情况肯定更严重。

由于上升的是自然失业率,因此很难通过需求扩展降低。当然,需求也很难扩张。

(三)2022年的严格封控,损害了各经济主体的资产负债表(点击)

1、非金融企业主动缩表

2022年各地长时间大面积封城,纷纷成为经济孤岛,供应链中断,企业现金流受到影响,营收和利润增速下降,杠杆率上升。虽然2022年底已经放弃了动态清零政策,但悲观预期叠加PPI同比转负,导致企业收入、利润增速下滑的态势难以扭转。企业发现自己的收入、利润增速在下降,库存在减值,资产在缩水,但负债却没有减少,即资产负债表恶化了。企业被迫收缩资产负债表,归还贷款、减少投融资,准备过冬。

甚至一些高科技企业都出现裁员、倒闭,这无疑会导致中国科技进步的速度放缓,埋下未来全要素生产率、自然利率、潜在GDP增速进一步下降的隐患(点击1、2)。

2、居民资产缩水,主动削减消费。

2022年各地长时间大面积封城,居民收入下降,疫情结束遥遥无期,逐渐形成悲观预期;叠加房价、股市、基金大跌,居民资产缩水,负债却没变,即资产负债表恶化。于是居民主动削减消费,归还债务,追求负债最小化。

3、政府财政吃紧,有心无力。

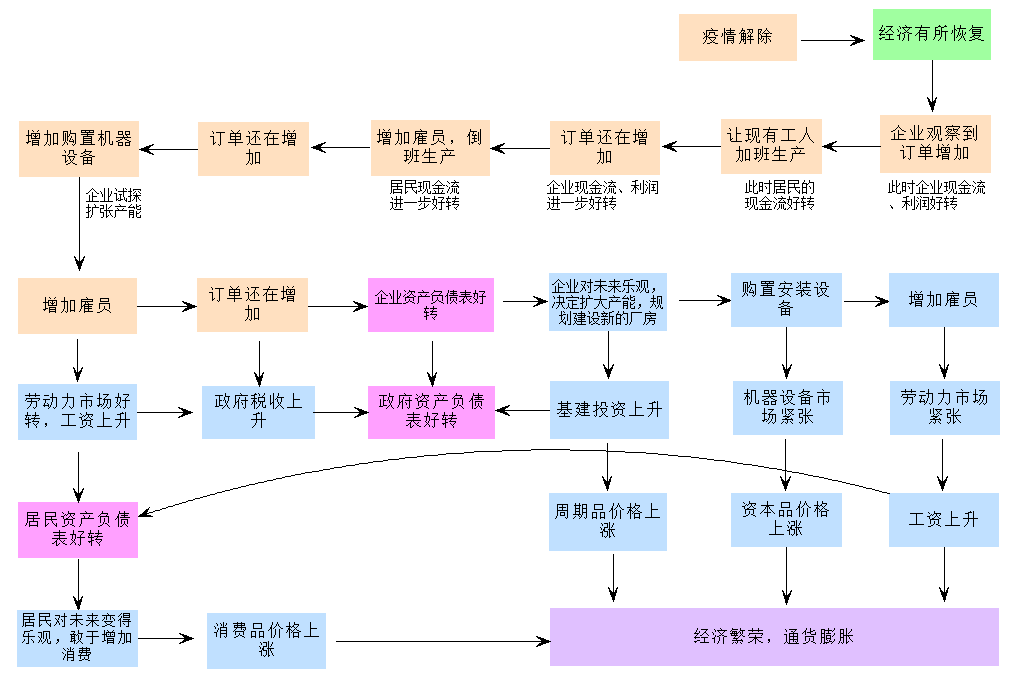

2023年6月,我在分析投资和消费为什么复苏缓慢时,认为中国经济在下图6右上方绿色方框那里。如果没有强有力的政策配合,单纯靠经济自发地调整、然后复苏,是一个非常漫长的过程,随时可能被各种因素打断,导致复苏中断。

图6 漫长的自发传导机制

资料来源:自己绘制

总之,从2022年开始,中国经济发生了严重的“资产负债表衰退”,同时陷入“腹背受敌阶段”(点击)。必须尽快采取强力的刺激政策:

1、中央财政主动加杠杆,扩张中央财政,代替地方财政、企业和居民来拉动经济。

2、把刺激消费作为重点,直接改善居民的财务报表,刺激消费。建议中央财政直接给边际消费倾向较高、符合特定条件的中低收入家庭发现金、大幅减税,降低存量房贷的按揭利率。而不是只给消费者购买耐用消费品减免税收或发放一点补贴,或者发放几元钱的消费券,这样毫无意义。

3、直接改善企业的财务报表,扭转企业的预期。降低一些行业的准入门槛,吸引民营资本进行投资;继续改善科技企业融资环境等。

4、货币政策进行配合,大幅下调LPR利率。

然而不幸的是,央行和财政部门抱残守缺,反应缓慢,导致至今经济依然在图6右上角的绿色方框那里。

三、中国经济在2022年陷入“腹背受敌阶段”

图3和图4给展示的都是“典型”国家的经济发展过程。按照辜朝明(2023)的观点,美国在1947年跨越刘易斯拐点,进入“黄金时代”;1970s跨越“辜朝明拐点”,进入“被追赶阶段”,被日本追赶。

日本在1960s中期至1990s中期处于“黄金时代”,持续了30年。1990s中期之后处于第三阶段,被韩国、台湾省和中国大陆追赶。

韩国和台湾省在1985年越过刘易斯拐点。1985-2005年处于第二阶段“黄金时代”,持续了20年。2005年进入“被追赶阶段”,被中国大陆追赶。

辜朝明对这些时间点的划分,显然是基于学术研究做出的。例如南亮进(Minami,1968)论证过,日本在大约1960 年到达了刘易斯拐点。

对于中国,辜朝明(2023,p.105)认为,中国在2012年之前处于第一阶段,2012年跨越刘易斯拐点,进入“黄金时代”。认为目前中国依然处于“黄金时代”。

我认为,中国经济很可能从2022年开始已经进入了“被追赶阶段”,开始被东南亚国家甚至拉美国家追赶。具体论证见这里。大体来说:

第一,2022年,中国的自然利率已经下降到与1970年的美国、1990s中期的日本类似的水平。

第二,中国的投资回报率已经低于潜在竞争对手。

第三,2022年开始,企业被迫开始加快“出海”。

从2022年开始,企业家普遍意识到:【1】东西方走向对抗的背景下,逆全球化加剧,美欧在东南亚、拉美加快培育供应链,来替代中国企业;【2】国内投资回报率下降严重。出海俨然成为很多企业为了自救、生存的必然选择。中国企业出海,在东南亚、拉美甚至非洲建厂,意味着这些地方的经济将起飞,实际上,东南亚、印度、非洲很多国家的GDP增速已经远远超过中国。只要有需求,它们的供应链将逐渐完善起来,逐渐替代中国。越南、泰国、老挝、缅甸、印尼、印度等国将成为中国的主要追赶者。

第四,中国从2022年开始陷入资产负债表衰退,驱使中国进入“被追赶阶段”。

总而言之,2022年的严格封控,一方面导致中国陷入资产负债表衰退,另一方面压低了中国潜在GDP增速和自然利率,导致中国投资回报率大幅下降,使中国在2022年已经跨越了“辜朝明拐点”,进入了“被追赶阶段”。

中国所处的“被追赶阶段”,与当初的美国、日本、韩国等完全不同。主要在于美国、英国、加拿大、澳洲、欧洲、印度等对中国抱有严重的敌意,试图在科技、贸易、供应链乃至国际政治、军事等方面全面挤压和遏制中国;并且企图扶持东南亚、印度、墨西哥,打造新的供应链来代替中国供应链。

即中国面临的是前有围堵、后有追兵,腹背受敌的状况。

因此,我更愿意将其称为“腹背受敌阶段”。

四、央行没有及时大幅降息,导致实际利率居高不下,放大经济波动

(一)央行错误地坚持所谓的“黄金法则”,刻舟求剑(点击)

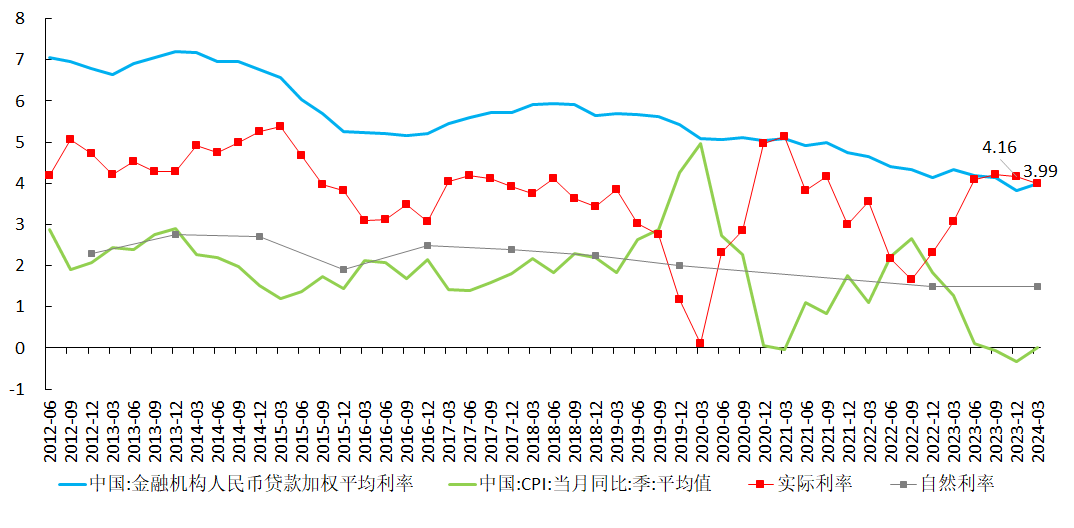

如前所述,2022年以来的疫情、封控政策和迟滞效应压低了我国的自然利率和自然产出。在2019年底,中国自然产出增速大约是6%多一点,2022年下降到了5%左右;2019年底,自然利率大约是2%(孙国峰和Rees,2021),2022年很可能已经下降到了1.5%甚至更低。

2022年开始,中国经济已经陷入严重的通货紧缩,实际利率在4%以上。实际利率高于自然利率,意味着货币政策是紧缩的,需要大幅降低名义利率(LPR),把实际利率压到低于自然利率。

然而,当时央行一直遵循所谓的“黄金法则”,即实际利率与潜在GDP增速大体相等。时任央行行长易纲(2021、2023)曾经多次阐述为什么要遵循“黄金法则”。他认为:

“理论上,自然利率是宏观经济总供求达到均衡时的实际利率水平…….中长期看,宏观意义上的利率水平应与自然利率基本匹配。由于自然利率是一个理论上抽象出来的概念,具体水平较难估算,实践中一般采用“黄金法则(Golden Rule)”来衡量合理的利率水平,即经济处于人均消费量最大化的稳态增长轨道时,经通胀调整后的真实利率r应与实际经济增长率g相等。

若r持续高于g,会导致社会融资成本高企,企业经营困难,不利于经济发展。r低于g时往往名义利率也低于名义GDP增速,这有利于债务可持续,即债务杠杆率保持稳定或下降,从而给政府一些额外的政策空间……总体上r略低于g是较为合理的,从经验数据看,我国大部分时间真实利率都是低于实际经济增速的,这一实践可以称之为留有余地的最优策略。但r也不能持续明显低于g,若利率长期过低,会扭曲金融资源配置,带来过度投资、产能过剩、通货膨胀、资产价格泡沫、资金空转等问题,超低利率政策难以长期持续。”

当时央行的利率政策正是遵循他的这一思路。例如2023年5月25日发布的央行《货币政策执行报告》专栏1就表达了同样的思想。一直到2023年,易纲(2023)还坚持认为:

“经济学理论中,一般参考泰勒规则和黄金法则等来衡量合适的利率水平。比较来看,泰勒规则强调短期逆周期调节,黄金法则(Phelps,1961)阐述了一条储蓄和投资的最优路径,此时消费也得到了持续满足,因此效用函数最优化。黄金法则是长期稳态的最优解,给我们的启示是实际利率应约等于潜在增长率,利率太低或太高都会产生不良后果。黄金法则对货币政策短期操作指导意义不大,但对较长时期时间序列验证是有意义的。黄金法则可以提供一个长期最优增长轨迹的衡量标准。”

2023年7月,我撰文指出“黄金法则”是在一系列假设条件下,用一个非常简单的模型推导出来的(点击)。这些假设条件包括:

【1】 经济是完全竞争性的;

【2】技术进步是外生的,且完全是劳动扩张型的。

【3】不存在外部性。

【4】生产函数满足规模报酬不变。

【5】劳动的供给是无弹性的,劳动力总量按照外生的速度γ指数增长。

然而这些条件在现实中都是不可能成立的。

【1】我国经济显然不是完全竞争性的,国企民企二元结构使民企始终处于弱势地位;经过2016年以来的供给侧结构改革,每个行业的集中度都在提高;技术进步不是外生的(点击)。

【2】几乎所有研究我国技术进步的论文都指出,我国技术进步不完全是劳动扩张型的。大多数研究发现,我国的技术进步是偏向劳动扩张型,美国的情况也是类似的(点击)。

【3】经济中不可能不存在外部性;

【4】生产函数当然也不是规模报酬不变的。

【5】劳动供给绝不是无弹性的。尤其是中国在2012年已经跨越了“刘易斯转折区间”,劳动力短缺日益严重(点击)。

等等。总之,“黄金法则”的前提是不成立的。因此在现实中,“黄金法则”不可能成立。

退一步说,“黄金法则”说的是“实际利率约等于潜在GDP增速”。由于CPI在不断变化,因此按照“黄金法则”,应该根据CPI调整名义利率,使实际利率保持相对稳定。

2022年三季度之后,随着经济走弱,CPI下降很快,名义利率下降缓慢,实际利率在快速上升(图7中红线),已经远高于自然利率。这意味着货币政策其实是收紧的。那么即使根据“黄金法则”,也应该大幅下调名义利率,把实际利率压低到2%以下。

图7 中国的实际利率

来源:国家统计局;中国人民银行;孙国峰和Rees(2021)

(二)在应该大幅降息时,却按兵不动,人为放大了经济波动

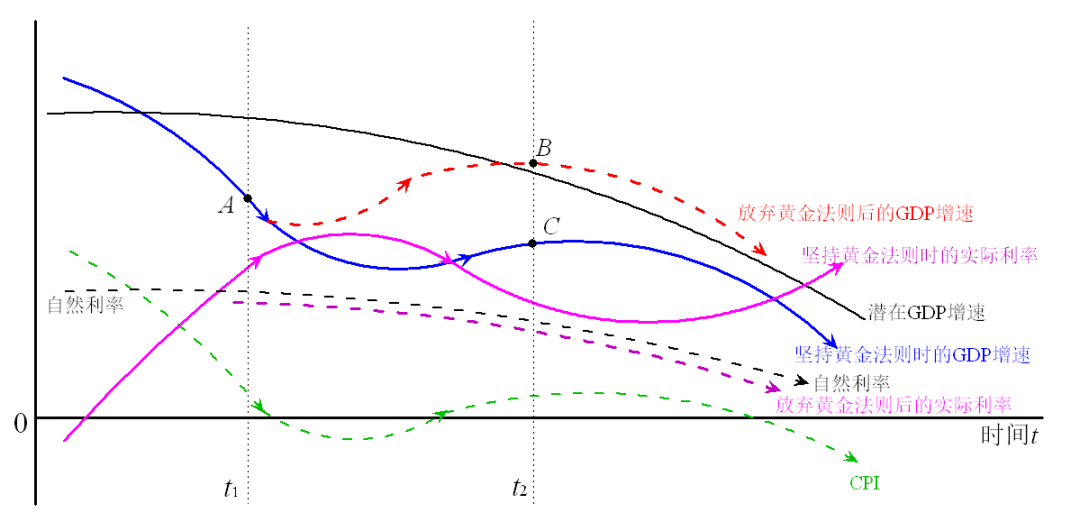

但是央行没有这么做,而是迂腐地坚持名义利率不变,导致实际利率居高不下。这是一种刻舟求剑的做法,会放大经济的波动。我当时用下图8来说明这个问题。图8中,潜在GDP增速(即自然产出增速,黑色实线)和自然利率(黑色虚线)长期下降,这符合我国当时的实际情况。

在t1时刻,经济处于A点,此时GDP低于潜在GDP增速,存在负的产出缺口,物价低迷(绿色虚线)。这也符合我国2022年以来的实际情况。

如果央行坚持黄金法则,不下调名义利率(没画出来),或者下调的幅度很小,则实际利率(粉色实线)会不断攀升,经济主体不堪重负;于是GDP增速沿着蓝色实线持续下滑。由于缺乏政策的支持,经济自发调整非常缓慢,若干个季度之后,到t2时刻,经济处于C点。此时依然存在负的产出缺口,CPI较低,实际利率较高,经济非常疲软,经济主体(企业、居民、政府)处于漫长的痛苦之中,利润表和资产负债表持续恶化,并且企业和居民对未来预期悲观,倾向于收缩资产负债表,削减投资和开支,导致经济持续疲软。

相反,如果央行放弃黄金法则,决定遵循泰勒规则、或参照自然利率行事,及时下调名义利率(没画出来),使实际利率下降沿着粉色虚线前进,等于或略低于自然利率,则经济主体的融资成本下降,利润表和资产负债表不再恶化。GDP增速将沿着红色虚线前进。若干个季度之后,到t2时刻,经济处于B点,大体和潜在GDP增速一致。如果能一直维持实际利率和自然利率一致(即央行保持货币政策中性立场),则GDP增速也可以保持与潜在GDP增速一致。

图8 坚持黄金法则与放弃黄金法则下的经济走势比较

资料来源:本文作者绘制

总之,在经济疲软、物价低迷阶段,如果央行拒绝下调名义利率,就需要居民和企业扛过经济低迷,痛苦地走完整个经济周期,再慢慢复苏。这需要漫长的时间,还会加大经济的波动,使经济主体遭受不必要的痛苦(福利损失),与央行福利最大化的初衷背道而驰,并且复苏过程还可能因为各种因素被打断(图6)。

基于这些分析,我建议央行尽快大幅下调LPR,至少使实际利率下降到2%附近(点击)。即便这不能刺激消费和投资,也可以营造宽裕的流动性环境,使地方政府、企业、居民能够以很便宜的利率贷到资金,将其持有的高息负债置换出来,改善资产负债表,延缓资产负债表衰退的速度和势头。

2023年7月25日,央行行长易人。此后央行《货币政策执行报告》中再也没有出现过关于“黄金法则”的描述。但是一直到2024年2月20日,才下调了LPR。

2024年4月30日中央政治局会议提出:“要灵活运用利率和存款准备金率等政策工具,加大对实体经济支持力度,降低社会综合融资成本。”意味着未来会继续降准降息。我认为这是对之前降息迟缓的矫正。认为未来一年LPR应该降低50-70BP。另外,应该加快深化改革和鼓励创新,推迟零利率和负利率时代的到来(点击)。

(三)惯性思维,跟不上形势

既然“黄金法则”有那么明显的弊端,为什么央行前行长会坚持这个法则?我认为,这是惯性思维导致的(点击)。

经济处于“黄金时代”和处于“被追赶的阶段”,表现是完全不同的。在“黄金时代”,居民收入快速增长,中产阶级队伍快速发展壮大,人人分享到经济发展的红利,对未来充满希望和自信,投资和消费增速强劲,货币乘数较高,经济有发生通货膨胀的倾向。但在“被追赶阶段”,大多数人收入增速下降,消费能力下降,货币乘数下降,通货膨胀问题要小得多。

但是人们(包括经济学家、央行行长和政府决策者)往往意识不到经济已经进入了“被追赶阶段”,还抱着“黄金时代”的思维惯性,容易把“黄金时代”经济指标的趋势简单外推。辜朝明(2023,p.159-160)认为,尽管所有发达经济体当前都处于被追赶阶段,但无论是经济学教科书还是这些国家的政策制定者,都无法摆脱“黄金时代”的惯性。

具体到Phelps(1961)的“黄金法则”来说,他提出“黄金法则”是在1960s,当时美国正好处在“跨越刘易斯拐点之后的黄金时代”,工人工资不断上升,投资和消费增长旺盛,技术进步迅速,投资回报率高。因此Phelps研究的问题是“什么样的储蓄(资本积累)路径,能够使居民的福利最大化?”带有强烈的时代色彩,完全没想到若干年后,会出现大规模的资产负债表衰退,导致储蓄过剩、投资不足的问题。

在中国,从1978年开始改革开放到2022年,中国从未出现过真正的资产负债表衰退。在1990s至2010年,地方官员一直在参加GDP锦标赛、投资饥渴症。2012年跨越刘易斯拐点之后,投资、GDP增速虽然有所回落,但还是比较高的,居民收入和消费也维持了较高增速。在这期间,虽然发生过总需求不足的问题(1998-2001,2008,2018),但都很快被改革或扩张政策熨平了。居民和企业对未来充满信心,即便是在2020年疫情爆发之后亦是如此。

在这种情况下,央行前任行长自然也会对未来抱着乐观心态,认为GDP将趋势性地维持较高的增速,自己要考虑的是,采取什么样的政策,能够使居民福利最大化。完全没想到2022年之后会突然出现投资回报率大幅下降,借款人消失,资产负债表衰退,过往的政策已经不再适合新的经济形势。

事实上,在2022年下半年经济回落的过程中,从政策制定者到市场研究者,几乎所有人都认为,总需求的回落是暂时的,是疫情封控限制了消费场景,影响了生产活动。只要放开疫情管控,居民就会“报复性消费”,企业就会开足马力生产,经济增速会很快恢复的疫情之前。一直到2023年4月之后,大家才意识到,居民和企业在继续缩表,消费和投资的恢复是非常弱的,需要漫长的过程。

这种惯性思维也影响到了对实际利率的认识。在“黄金时代”,由于需求旺盛,容易出现通货膨胀。尤其是,在2010年至2021年,中国的房价高速增长。央行自然倾向于维持较高的名义利率,以便维持较高的实际利率,这样一方面可以控制通货膨胀,另一方面可以控制房价。但是经济进入“被追赶的阶段”后,通货膨胀不再是个大问题,而是有发生通货紧缩的倾向,加上发生了资产负债表衰退,此时名义利率僵化就容易导致实际利率飙升,对经济造成损害。

(四)在应该改善居民和地方政府资产负债表时,却鼓励买房,将导致它们资产负债表更加恶化

2021年以来,房地产库存积累,价格大幅下跌,大量居民断供、弃供。房企无法回笼资金,银行无法收回贷款,面临金融风险。

5月17日,央行宣布了刺激房地产的政策:取消购买商品房贷款利率下限;下调个人住房公积金贷款利率0.25个百分点;把首套房的首付比例下限从20%降至15%,二套房从30%降至20%;设立3000亿保障性住房再贷款,支持地方国有企业以合理价格收购已建成未出售商品房,用作配售型或配租型保障性住房,预计将带动银行贷款5000亿元。保障性住房再贷款期限一年,可展期4次,利率1.75%。发改委则要求:商品房库存较多城市,政府可以需定购,酌情以合理价格收购部分商品房用作保障性住房(点击1,2)。

至此,房地产刺激政策已经是有史以来最宽松的了。

在地方政府和居民资产负债表恶化的大背景下,不仅没有帮它们改善资产负债表,反而推出了这样的房地产刺激政策,本质上是想让已经负债累累居民和地方政府继续加杠杆,增加负债,把房地产商和银行的杠杆接过来,降低房企和银行的违约风险。换句话说,决策者在“改善居民和地方政府资产负债表”与“为房企和银行纾困”之间,选择了后者。我猜可能是因为前者更遥远,而后者更紧迫。政策的时间不一致性表现得淋漓尽致。

从长期看,这会导致居民和地方政府的资产负债表进一步恶化,居民消费能力更加萎缩;地方政府负担将进一步加重,更加无力进行基建投资和民生建设。最终会给未来经济带来需求不足的隐患,导致资产负债表衰退更加严重。甚至可以说,房地产刺激效果越好,成交量越大,对未来经济的拖累会越严重(点击)。

五、财政政策不仅没有及时强力扩张,反而人为制造紧缩

(一)中央财政在应该尽快大幅加杠杆时瞻前顾后、畏首畏尾

2022年以来,中国经济陷入“资产负债表衰退”和“腹背受敌阶段”。居民主动削减消费,企业主动削减投资,追求负债最小化;而地方政府由于背负沉重的债务负担,无力扩张资产负债表。那么就应该由中央政府来扩张资产负债表、拉动经济、减缓经济下行。

用辜朝明(2023)的范式来说,就是企业和居民已经不愿意借款,那么政府应该充当最后的借款人,使信用创造过程能够持续下去,创造需求。

原则上说,在“资产负债表衰退”和“腹背受敌阶段”,货币政策的效果远远不如财政政策。

因此,2023年二季度,当发现经济恢复乏力、居民和企业仍在缩表时,中央财政就应该尽快扩表,主动扩大财政赤字,主动加杠杆(点击)。比如可以:

【1】通过重点建设项目拉动投资;设立各类大型产业基金,投资于高端科技项目、“卡脖子”项目,吸引民间资本一起进行投资等。

【2】给企业大幅减税,直接改善企业的负债表,放水养鱼。

【3】给特定家庭发放现金,直接改善家庭的资产负债表,刺激消费。

采取这些措施速度要快,力度要大,才能尽快扭转经济主体的悲观预期,切断资产负债表衰退的传导机制。

但是2023年开始,中央财政似乎对经济面对的困难认识不清楚,一直畏首畏尾:

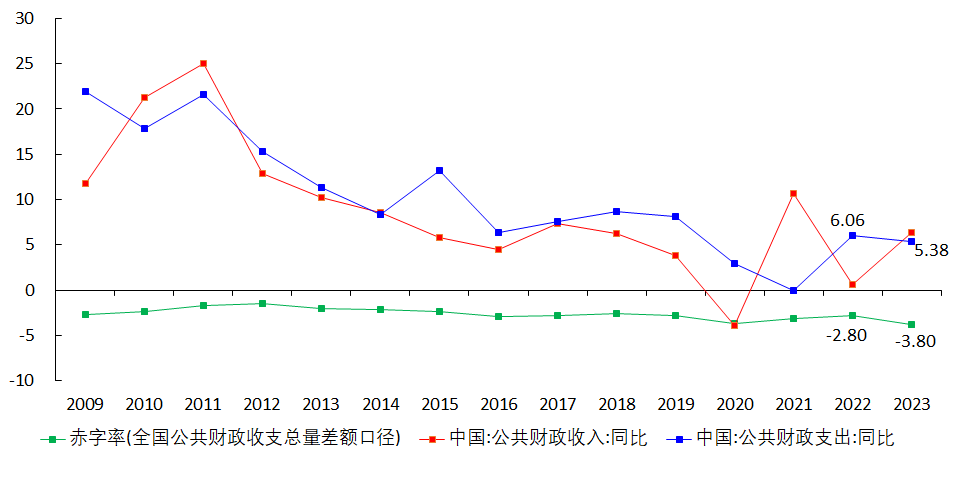

【1】财政支出扩张的力度不够大。2023年上半年,各界就不断呼吁发行特别国债挽救经济,但迟迟没有动静。一直到2023年10月25日(新财政部长上任的第二天)才宣布发行1万亿特别国债。2023年全年财政支出增速只有5.38%,比2022年还低。财政赤字比2022年只上升了1个百分点。

【2】不愿意直接给特定家庭发现金,似乎担心这会违背多劳多得、不劳不得的社会主义价值观。反映了决策者思想僵化、不知变通。

结果只有部分城市(上海、深圳、北京、杭州等)给居民发放消费券,但效果不佳。原因是:①金额太小,人均只有2-3元钱,不可能拉动消费;②地方政府发放消费券,受益的未必是本地企业,因此地方政府缺乏动力。其实这事最好中央财政来做。

【3】观念陈旧、抱残守缺,以为给消费者减免一点税收(例如减免车辆购置税),或者给企业一点补贴,就能刺激他们购买耐用消费品或更新机器设备。完全不理解,在资产负债表衰退阶段,居民和企业根本就不愿意消费和投资,这样做的效果非常有限。

图9 中国公共财政收入、支出增速与赤字率%

资料来源:财政部

2023年10月24日,新财政部长就职。次日财政部宣布将在2023年四季度增加发行1万亿元特别国债,这使2023年全国财政赤字由3.88万亿元增加到4.88万亿元,中央财政赤字由3.16万亿元增加到4.16万亿元,财政赤字率由3%提高到3.8%左右。

2024年3月5日《政府工作报告》提出,从2024年开始拟连续几年发行超长期特别国债,专项用于国家重大战略实施和重点领域安全能力建设,今年先发行1万亿元。

但是,我认为这个力度还是远远不够。

(二)国税部门在应该放水养鱼时,却预征收过头税、倒查税收,涸泽而渔

在企业和居民全面缩表的当下,原本应该减税,改善企业和居民的资产负债表,刺激消费和投资。然而税务部门的做法恰好相反,它们采取了两个措施:

一是倒查税收,追缴历史欠税(点击)。

追缴历史欠税是合法的,但时机不对。说小一点,此举会抽走企业现金,导致企业经营困难,被迫停产甚至裁员,营业收入和经营利润下降,进一步陷入困境。说大一点,会破坏营商环境,导致失业、居民消费下降、加大通货紧缩压力。

二是预征“过头税”,即预征未来的税款。

预征过头税对经济有害无益。即便一开始经济处于稳态增长路径,预征过头税也会使经济偏离稳态(点击)。并且随着时间推移,GDP规模将偏离稳态增长路径的GDP规模越来越远;应缴纳税款也将偏离稳态增长路径的应缴纳税款越来越远。

在经济高速发展阶段,预征过头税的负面影响很容易被后续的经济增长对冲掉,因此对经济的负面作用不那么大。

但是现在中国经济已经进入了“腹背受敌阶段”,GDP增速将长期下降,还将长期面临通缩压力,名义GDP增速的长期趋势也将下降,这会导致财政收入将逐年下降。此时再预征过头税,会导致经济增速下降的压力更大,雪上加霜。只能以后每年都预征过头税,否则财政就无法维持。而持续不断地预征过头税,会导致企业和居民更加缩表,经济增速雪上加霜,财政迟早会崩溃。

这些政策都是紧缩性的,体现了税务部门缺乏大局观,涸泽而渔,饮鸩止渴。

(三)地方政府在应该休养生息时,却杀鸡取卵

地方政府的支出普遍存在严重的刚性。2022年以来,随着经济下滑、财政收入下降,地方政府为了增加收入,普遍采取了如下措施:

一是削减对公用事业(水电煤气、公共交通)的补贴,推动公用事业涨价(点击1、2)。

这会导致居民:

【1】削减消费;

【2】居民担心公用事业开支未来会进一步上升,因此会提前增加储蓄,导致消费下降得更多。

【3】居民原本就对经济前景和收入前景不乐观。当政府削减补贴时,居民会把这当作经济进一步恶化的信号,因此会增加储蓄,以防未来经济下滑、自己失业。从而导致消费下降得更多。

结果,消费下降的金额将远远超过政府节约的补贴金额,可能达到政府节约的补贴金额的数倍。即便政府通过其他渠道(例如政府消费或投资),把节约下来的这部分补贴花出去,对经济的净影响也一定是紧缩性的。

公用事业价格上升本身会推高CPI和PPI。有些愚蠢的宏观分析师对此欢呼雀跃,认为这有助于经济走出通缩,却没注意到它会抑制消费,压低CPI和PPI,最终导致更严重的通货紧缩。

如果每个地方政府都提高公用事业价格,对整个经济将是灾难性的,它本质上是“以民为壑”,使居民的资产负债表更加恶化,消费意愿和消费能力更低。长期看,导致当地消费不振,经济增长乏力,最后政府的资产负债表也无法修复。

二是提高行政处罚力度,增加罚没款收入。

在一些城市,罚没款收入已经占到当地财政收入的40%以上。它对经济的影响与提高公用事业价格是类似的,并且更加恶劣,因为它不仅迫使居民和企业进一步缩表,还会严重破坏当地的营商环境。

目前中央正在酝酿对消费税进行改革,将其从全归中央,改为央地分成,使地方增幅能增加一个收入来源。问题在于,从国税预征过头税、倒查税收,地方增加罚没款收入来看,国税和地方都缺乏远见和大局观。在这种情况下,简单地进行央地分成,并不能解决他们涸泽而渔、杀鸡取卵的做法。

需要指出的是,在经济衰退时期加税这种蠢事,日本政府也干过。1990年日本泡沫破裂,1995年陷入“被追赶阶段”。1997年,IMF和OECD向日本政府施压,要求日本削减财政赤字。于是日本政府于1997年4月开始实施15万亿日元(占日本GDP的3%)的财政紧缩计划(加税、缩减开支),结果导致日本经济雪上加霜,GDP连续5个季度下降。一些成功熬过之前7年衰退的银行开始纷纷倒闭。2001年、2009年日本政府又两度犯了类似的错误。

中国政府应该摸着日本的尸体前进,而不是重蹈覆辙。

六、“腹背受敌阶段”的中国经济有哪些特点?

在“腹背受敌阶段”,经济将呈现出如下的特点:

(一)潜在GDP增速将长期下降

目前中国潜在GDP增速大约是5%。未来在自然利率下降的同时,潜在GDP增速也将逐年下降。现实中的GDP同比将随之下降(点击),20年后可能下降到1-2%。

值得注意的是,如果把全国看做一家公司,那么GDP相当于营业收入,而不是利润。这家公司的效率特别低,2023年GDP同比5.2%,对应规模以上工业企业利润同比只有-2.3%,股市处于熊市。如果不能尽快提高TFP,那么未来当中国GDP增速降低到只有1-2%时,企业利润增速可想而知。

(二)M1、M2、社会融资规模、信贷余额存量同比处于低位

2024年4月,M1、M2、社融、信贷余额同比增速都创出历史最低(点击),引起了广泛的讨论。在我看来,这是经济陷入“腹背受敌阶段”必然出现的现象。

在“黄金时代”,经济增长强劲,居民收入上升,甚至一些低学历、缺乏技能的人也很容易找到工作,人们对未来预期非常乐观,边际投资倾向和边际消费倾向较高,投资和消费增速都比较强劲。对贷款需求旺盛,很容易推高货币乘数,货币政策非常有效,容易出现通货膨胀。M1、M2、社融、信贷余额同比增速无疑将比较高。

但是随着经济陷入“被追赶阶段”,国内要素成本上升,投资回报率下降。由于缺乏有利可图的投资机会,企业的融资意愿和投资倾向下降,储蓄率上升,导致消费增速下降,失业率上升,居民收入增速下降,甚至负增长,贫富差距扩大。由于经济缺乏活力,因此M1同比将处于较低水平。

企业和居民的融资意愿大幅下降,导致货币乘数将下降,货币流通速度放缓,货币创造机制不那么顺畅,M2同比、信贷余额同比增速都将下降到较低的水平。

金融部门向实体部门融出的资金量下降,即社会融资规模的存量同比将下降到较低的水平。

2024年5月10日,央行发布了一季度《货币政策执行报告》,其中专栏1《信贷增长与经济高质量发展的关系》指出,随着经济转型升级和高质量发展,我国信贷增长与经济增长的关系趋于弱化。信贷增速下降至个位数,并不意味着金融支持实体经济力度减弱。主要原因是:【1】随着经济结构调整升级,房地产式微,地方债务风险防控加强,重化工业占比下降,对信贷的需求下降了。【2】随着信贷存量规模增长,信贷投放的边际效果递减。过度投放信贷会导致资金空转。【3】直接融资占比在上升。

这三点是有道理的。长期看,这三点都将继续存在,导致货币供给指标都将继续处于低位。未来很低的M1,7%甚至更低的M2,8%甚至更低的社融同比,9%甚至更低的信贷余额同比将成为常态。

(三)特别容易发生“资产负债表衰退”

“资产负债表衰退”可能发生在经济进入“腹背受敌阶段”之前,也可能发生之后。但是在“腹背受敌阶段”,特别容易发生“资产负债表衰退”,并且会反复发生。

这是因为,“腹背受敌阶段”的本质,就是真实因素导致本国实体部门投资的边际回报率下降,当下降到一定程度(图3中H点),低于后进国家时,本国企业为了盈利,只好出海投资,利用外国的低要素成本,赚取更高的投资回报。从而导致本国消费、投资、就业、经济增速全面下降。当企业在本国投资普遍无利可图时,它们就会主动缩表,削减投资,导致更多的失业;导致居民主动缩表,削减消费,即导致资产负债表衰退。

(四)将长期存在通货紧缩的压力,且很难逆转(点击)

在“腹背受敌阶段”,由于本国缺乏有利可图的投资机会,企业的融资意愿和投资倾向下降,储蓄率上升,导致消费增速下降,失业率上升,居民收入增速下降,甚至负增长。显而易见,此时经济容易发生通货紧缩。

2022年以来,我国一直存在较大的通货紧缩压力。如果通缩压力来自短期的需求下滑(像2008年那样),那么随着需求快速恢复,通缩压力就会消失。但是2022年以来的通缩压力,根源是真实因素变化导致自然利率下降,这是个长期趋势,很难逆转,因此它带来的总需求萎缩、通缩压力加大也是难以逆转的,将长期存在(点击)。地方政府和税务部门不合时宜的政策又加重了通缩的压力。

另外,目前我国制造业产能占全球的大约30%,其中大约15%供应国外(出口),15%供应国内。当外需走弱时,如果内需能走强,消化多余的供给,则可以化解通货紧缩压力。问题在于,我国进入“腹背受敌阶段”后,一方面国内消费和投资需求增速下降;另一方面,出口将受到欧美日的围堵(提高关税、限制进口),东南亚、南亚、墨西哥等竞争对手的追赶。这样内外需双双受到挤压,很容易造成产能过剩,加大通货紧缩压力。

(五)无法再采用行政措施去产能(点击)

那么,有没有可能再像2016-2017年一样,再搞一次行政去产能,用行政手段强迫(比如)环保不达标的中小企业退出行业,人为造成供给端产能收缩,使产品价格上涨,从而使经济摆脱通货紧缩,改善存活下来的企业的现金流和利润表?

我认为不会,也不应该。理由是:

第一,当前的经济环境与2016-2017年完全不同。

在2016-2017年,经济增速和企业盈利增速还比较高。当时迫使一些企业退出市场,让留存的企业改善处境,对整个经济影响不大。而现在整个经济状况很差,GDP增速下降,企业利润增速下降,在这种情况下再强迫一批企业退出,会造成严重的失业。

第二,目前的产能过剩与2012-2015年的产能过剩不同。

2012-2015年的产能过剩是此前十几年投资导向型发展模式造成的,主要集中在传统周期性行业(钢铁、煤炭、有色、化工、建材等)。其中很多产能确实比较落后,不能适应市场的要求,理应淘汰掉。2016-2018年供给侧改革后,升级改造或新建了产能。现在的“产能过剩”是2022年以来GDP增速下滑过快、需求不足导致的,而不是说产能已经太旧,不能适应市场需要了。如果去产能,把总供给曲线向左移动,会造成GDP增速进一步下降,那些竞争力弱、抗风险能力差的中小企业雪上加霜。而中小企业是吸纳就业的主力,如果中小企业大面积倒闭,势必危及社会稳定。

第三,通过行政手段去产能,被去掉的往往是民营企业,会进一步造成国进民退,降低TFP,导致投资边际回报率更低。

第四,频繁地用行政手段去产能会导致制造业空心化。在“腹背受敌的阶段”,投资、消费疲软将长期存在。假如一出现产能“相对过剩”和通缩压力,就通过行政手段去产能,那么长远来看,需要不断地去产能,最终加剧制造业空心化。在美国主导与中国经济脱钩、试图摆脱中国供应链的当下,制造业空心化无异于自杀。

(六)不宜再拿库存周期分析经济,期盼新周期启动

2023年9月,国家统计局发布的工业企业经济效益指标中,产成品库存名义同比出现小幅反弹。不少金融机构的宏观分析师欢欣雀跃,认为新库存周期即将启动,上升阶段会持续3-4个季度,带来股市大幅上涨。

这个观点显然是错误的。我当时撰写了几篇文章,来反驳这种观点,论证工业去库存过程并未结束,补库存遥遥无期(点击1、2)。事实证明我的分析是正确的。

另外,我从2012年开始,就反对拿理想化的库存周期模型硬套中国经济现实、认为周期的四个阶段会像春夏秋冬一样按顺序依次到来,每个阶段一定会按部就班地持续3-4个季度。

实际上,在2012-2015年的产能过剩、需求增速下滑时期,政府的稳增长政策扭曲了库存周期,导致去库存过程被拉长。库存周期的每个阶段都很短,幅度变小了。如果过剩产能如果不能及时退出,会持续抑制企业的利润率和利润增速,导致利润率和利润增速持续低位波动(点击)。这是2016年开启供给侧改革、去产能的逻辑基础。

随着目前中国经济陷入“腹背受敌阶段”,需求增速将逐年走弱。总需求即便有反弹,也是非常弱的,造成的库存周期将非常弱。并且不能再简单通过去产能来挽救PPI。在这种情况下,再试图分析库存周期、根据库存周期来判断行业的运行、拿美林时钟来做资产配置,必然不会什么效果。

(七)资金空转将成为常态

2022年以来,我国再度出现资金空转,引起了监管部门的关注。

2023年8月4日上午,国家发改委、财政部、央行、国税总局联合召开新闻发布会,央行货币政策司司长邹澜在回答记者提问时说:“(要)既根据经济金融形势和宏观调控需要,适时适度做好逆周期调节,又要兼顾把握好增长与风险、内部与外部的平衡,防止资金套利和空转,提升政策传导效率,增强银行经营稳健性。”

2023年11月22日,中国人大网发布《对金融工作情况报告的意见和建议》,其中提到:“近期,我国M2增幅高,M1增幅低,两者不相匹配,原因之一在于货币资金在银行间空转,或在银行与大企业之间轮流转,面向中小企业的信贷资金渠道不畅。”

2024年3月5日的《政府工作报告》指出要:“加强总量和结构双重调节,盘活存量、提升效能,加大对重大战略、重点领域和薄弱环节的支持力度。促进社会综合融资成本稳中有降。畅通货币政策传导机制,避免资金沉淀空转。”

这些都表明中央在试图防范资金空转。

问题在于,本轮资金空转的根源,是自然利率(投资回报率)下降,即出现了“资产荒”,实体企业不愿意投资,居民不愿意消费,大量资金无处可以投资,于是流向金融机构,被加杠杆投资于长端债券。未来随着自然利率的继续下降,这种情况将继续存在。

央行要想杜绝资金空转,只有两个办法:

一是收紧货币,回笼流动性。这显然会造成经济增速下降,央行肯定不愿意这么做。

二是把结构性货币政策做到极致,严格控制从银行体系流出的资金的流向。这样做的成本极高。

因此这两点都无法采取。

总之,在“腹背受敌阶段”,央行必须保持流动性宽裕局面,这样必然有一部分资金处于空转状态,无法完全杜绝。这是我一直看好长债的理由之一。

(八)财政赤字将逐步走高,需要政府解放思想,敢于提高赤字率

经济进入“腹背受敌阶段”之后,货币政策效果逐渐下降,财政政策效果更好。这意味着财政政策将成为稳定经济的主力,货币政策只要保持宽松局面,做好配合即可。

财政扩展,意味着财政赤字扩大。这就需要政府彻底转变思路、解放思想,敢于提高财政赤字率。

依然以日本为例。1990年日本陷入衰退之后,日本政府开始扩张财政赤字,稳定经济。但是:

“正统财政鹰派主导了日本媒体和学术界,试图给财政刺激设置障碍,表示巨额财政赤字将很快导致利率飙升和财政危机。一旦经济出现复苏迹象,鹰派就会给政客施压,(要求)削减刺激措施,从而引发新一轮经济衰退。由此产生的时断时续的财政刺激,并没有提升公众对政府处理经济方式的信心……..”(辜朝明,2023,p.069)。一直到1997年IMF和OECD给日本施压,要求削减财政赤字,导致日本衰退加重。

这就是为什么我在前文说,每年发行1万亿特种国债远远不够。财政政策应该是:只要经济没有好转,就继续扩大财政赤字。而不是提前设置严格的赤字率限制,捆住自己的手脚,不敢突破。

(九)长期看,国债收益率将持续下降到0或负值

自然利率下降导致全社会面临“资产荒”,上市公司ROE下降,股市缺乏系统性的投资机会。金融机构把大量资金投向债券市场,导致2023年下半年以来,长期国债利率一直在下降。

In the long run, if institutional reforms cannot be used to release institutional dividends, and if the new round of technological revolution cannot be seized to improve the investment return rate of various industries, then with the aggravation of population aging, the natural interest rate will continue to decline. Eventually, like the United States and Japan, the natural interest rate will fall to near 0 or even negative, and the growth rate of natural output (potential GDP) will also fall to a very low level. The actual GDP growth rate will decline year by year, falling to 1-2% in more than a decade.

Therefore, in the long run, the yield of treasury bonds will also fall to 0, or even fall to negative. Therefore, since the second half of 2023, I have been optimistic about interest rate cuts and the investment opportunities of long-term bonds (click), believing that any adjustment is an opportunity to buy.

In the summer of 2021, I still believed that the natural interest rate in China would fall to 0, which would happen in 20-30 years. Now, this day is getting closer and closer to us.

The central bank is quite wary of the decline in ultra-long-term yields. On April 23, 2024, the relevant department head of the central bank said in an interview with the Financial Times:

“In theory, long-term fixed-rate bonds have a long duration and are more sensitive to interest rate fluctuations, and investors need to pay close attention to interest rate risk. For trading investors, by increasing leverage and extending duration, they can obtain more returns in the short-term price increase, but it is also easy to aggravate market fluctuations and need to bear the loss of a sharp decline in prices. For institutional investors such as banks and insurance companies, if a large amount of funds are locked in long-duration bond assets with excessively low yields, they will face a passive situation where revenue cannot cover expenditure if the cost on the liability side rises significantly.”

And the collapse of Silicon Valley Bank in the United States in March 2023 was used to remind investors to pay attention to risk control.

On July 1, 2024, the central bank entered the market and sold treasury bonds, leading to a sharp drop in treasury bond prices. On July 2 and 3, 2024, bond prices rose, and the 10-year treasury bonds completely recovered their losses, while the 30-year bonds recovered some. The central bank can use this to exercise its ability to manipulate the yield curve, but it cannot reverse the long-term downward trend.

(X) The central bank will be forced to enter the market to trade treasury bonds and implement fiscal deficit monetization, and take QE when necessary.

On April 23, 2024, the relevant department head of the central bank also said in an interview with the Financial Times:

“The central bank’s trading of government bonds in the secondary market can be used as a way of liquidity management and a reserve of monetary policy tools… Some developed economies’ central banks are forced to buy government bonds on a large scale in a single direction to achieve monetary policy goals when conventional monetary policy tools are exhausted, while China adheres to the implementation of normal monetary policy. The People’s Bank of China’s buying and selling of government bonds is completely different from the quantitative easing (QE) operations of these central banks.”

Indeed, the natural interest rate in China is currently positive, and the investment return rate of the real economy is positive, so it can still “adhere to the implementation of normal monetary policy”, so the central bank’s buying and selling of government bonds is completely different from the QE of the West. But in the long run, with the natural interest rate, the growth rate of natural output, and the investment return rate continuing to gradually decline, sooner or later, it will be like Europe, America, and Japan, with the natural interest rate approaching 0 or becoming negative. At that time, QE operations will have to be frequently adopted.

In order to postpone the arrival of this day, on the one hand, policymakers must do their best to deepen reforms and stimulate innovation to improve the investment return rate of the economy. On the other hand, the central bank should enter the market as soon as possible and directly trade government bonds, so that (click):

First, it can relatively flexibly regulate the yield curve.

Second, in the long run, it can cooperate with the fiscal authorities to finance fiscal deficits. Although I personally hate deficit monetization, this is a choice that has to be made.

Third, it accumulates experience for future QE.

(XI) The gap between rich and poor will widen, and the Gini coefficient will rise.

As mentioned earlier, theoretically, before the economy reaches the “Lewis turning point”, the gap between rich and poor will widen; after crossing the “Lewis turning point” and entering the “golden age”, the gap between rich and poor will narrow; after crossing the “Koo turning point” and entering the “attacked from both sides stage”, the gap between rich and poor will widen again. This situation has been confirmed in the United States, France, Germany, India, Thailand, and other countries (click).

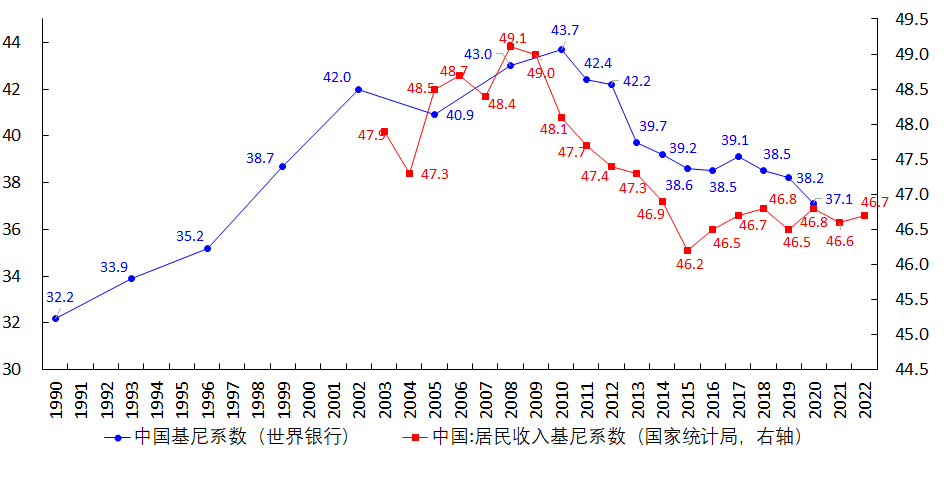

Judging from the data in China, from the 1990s to the 2010s, with the rapid growth of GDP, some people became rich first, the gap between rich and poor widened, and the Gini coefficient quickly rose to over 40. Around 2010, the Gini coefficient peaked. Afterwards, with the upgrading of the industrial structure and the shift from the east to the central and western regions, the “first to get rich” began to drive the “later to get rich”, the income of residents generally increased rapidly, and they shared the dividends of economic growth, and the Gini coefficient began to decline.

Figure 10 China’s Gini coefficient

Source: National Bureau of Statistics of China; World Bank

As the economy enters the “attacked from both sides stage”, economic growth slows down, the growth of total demand slows down, the growth of residents’ income slows down, or even becomes negative. Only those with advanced technology, or those with strong learning ability and the ability to adapt to the new situation, can find jobs. Those whose jobs are easily transferred abroad will easily lose their jobs and fall into difficulties. The gap between rich and poor will widen, and the Gini coefficient will rise. This will obviously cause social instability.

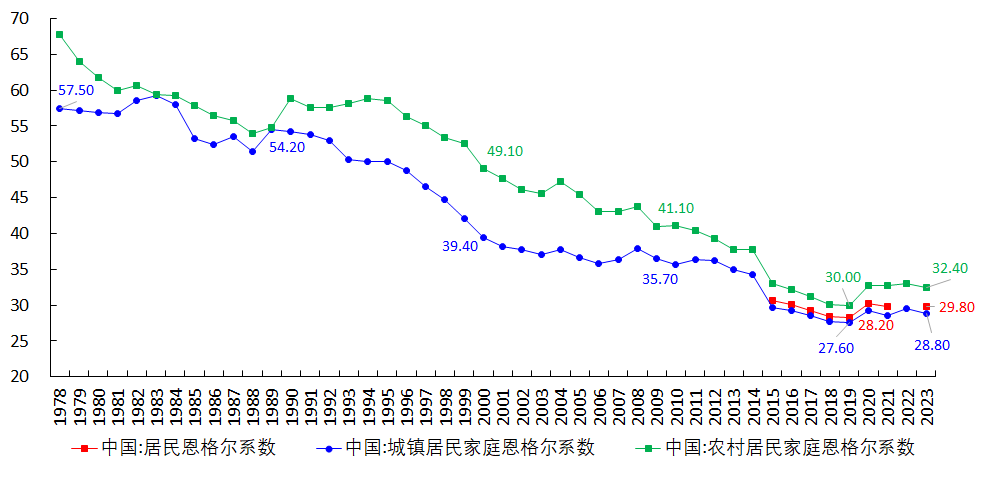

(XII) The Engel coefficient will rise, and residents will spend a larger proportion of their income on food.

Engel’s law says that the lower a family’s income, the larger the proportion of the family’s income spent on food, and the lower the proportion spent on education, cultural entertainment, and medical and health care.

Since 1978, China’s Engel coefficient has been trending downward, which is a typical manifestation of an economy in the process of urbanization/industrialization.

Figure 11 China’s Engel coefficient

Source: National Bureau of Statistics

However, I have noticed that since 2020 (click):

1. The growth rate of consumption expenditure of Chinese residents is declining, and the reasons are: 【1】The epidemic has led to the lack of consumption scenarios; 【2】Residents’ families actively shrink their balance sheets and reduce consumption expenditure.

2. Food expenditure is rigid.

This has led to a significant rebound in the Engel coefficient from 2020 to 2023.

As the economy enters the “attacked from both sides stage”, the growth of total demand slows down, the growth of residents’ income slows down, or even becomes negative. Those whose jobs are easily transferred abroad will easily lose their jobs and fall into difficulties. Logically speaking:

1. Residents will cut consumption expenditure and give priority to spending on necessities (such as food, housing, utilities, and healthcare), and cut spending on luxury goods and optional consumer goods (such as clothing, cultural entertainment services, etc.). This will lead to a rise in the Engel coefficient.

2. As the income growth rate further declines, in the event of a severe economic recession, residents will also lower their requirements for necessities, such as lowering their requirements for food, no longer pursuing “eating well”, reducing the purchase of “high-end food” and “optional food”; instead, they will aim to “eat enough” and only purchase food that meets the basic needs of life. This will lead to a reduction in residents’ spending on food. However, since income and consumption expenditure have also decreased at this time, the Engel coefficient should still rise.

3. In extreme cases, as the economy gets worse and worse, residents’ savings will be gradually consumed, and residents will also begin to cut spending on necessities, further reducing the requirements for the “quality” of necessities, and maintaining the basic quantity requirements. Even the requirements for “quantity” are reduced.

In short, I believe that the downward trend of China’s Engel coefficient has ended and it is difficult to continue to decline. With the long-term decline in economic growth, the Engel coefficient will rise.

The analysis of Japanese data found that after 1996, the Engel coefficient in Tokyo fluctuated horizontally and slowly rose (the graph is shown here), which is in line with my judgment on the Engel coefficient of “chased economies” in terms of trend. In terms of consumption structure, from 2002 to 2023, Tokyo households:

1. The proportion of spending on food, education, healthcare, and furniture and household goods in consumption expenditure has increased.

2. The proportion of spending on cultural entertainment, housing, clothing and footwear, and other items has decreased.

3. The proportion of spending on fuel, electricity and lighting, and transportation and communication has remained largely flat.

This change is largely similar to the change in the consumption structure of Chinese residents since 2020, both of which are ensuring basic living needs while reducing “optional consumer goods”. Understanding this, when allocating industries in the stock market, you can avoid those industries that have no future, see here> for details.

(XIII) The population birth rate will continue to remain low.

The population birth rate depends on the residents’ wealth stock, expected income level, and the cost of raising children. In recent years, the epidemic, the decline in income growth, and the rise in the cost of raising children have jointly led to a decline in the birth rate.

In the “attacked from both sides stage”, the income growth rate will further decline, and the pressure of life will increase, which will inevitably lead to a further decline in the willingness to give birth, and the birth rate will continue to remain low. Since the mortality rate is relatively stable, the final result is that the total population will decline year by year.

It is impossible to reverse the decline in the fertility rate by issuing subsidies and extending maternity leave, because the benefits brought by subsidies and holidays to residents are limited and far from offsetting the pain brought to residents by the decline in income growth and the cost of raising children.

By the way, what is more terrible than the decline in the total population is the deterioration of the population structure. The proportion of the Han ethnic group in the whole country, especially in some provinces in the northwest and southwest, is constantly declining, and the decline in the proportion of the Han ethnic group among children and newborns is shocking. This will inevitably seriously endanger national stability in the future.

(XIV) Populism and extreme nationalism will resurface and collude (click 1, 2)

Liu He, former Vice Premier of the State Council (2013), said when summarizing the social trends after the outbreak of the financial crisis abroad:

“After the outbreak of the crisis, policymakers always face the three major challenges of populism, nationalism, and the politicization of economic issues, and market forces constantly challenge unconvincing government policies, which makes the crisis situation worse.” (Liu He, 2013, p.11)

I think it is also appropriate to analyze China’s future.

In China, both nationalism and populism have a broad social base. The rapid economic development of China since 1978 has concealed many social contradictions. As the economy enters the “attacked from both sides stage”, those who lack learning ability will not be able to adapt to the changes in industries and the impact of the times, and will fall into unemployment, a decline in income levels, and a difficult life. Their cognitive abilities are limited, they feel confused about this impact of the times, and they cannot understand why they have fallen into this situation.

At this time, some self-media will begin to promote populism and irrational extreme nationalism, spread rumors, and advocate various fallacies, such as the economic problems and the difficult lives of ordinary people are because the government ignores the interests of the people at the bottom, because the powerful monopolize power, because of the unfair distribution system, because of technological progress (such as e-commerce impacting physical stores), because the elite deliberately plunder the people at the bottom, because of the conspiracy manipulation of capitalists, because of the infiltration of foreign forces, because globalization has robbed them of their jobs, and so on.

People who lack learning ability and cognitive ability, of course, also lack the ability to distinguish, and are more easily incited by these fallacies and become loyal followers of populism and irrational nationalism. Populism and extreme nationalism collude, which will endanger social stability.

“In the case that the space for public policy is squeezed very small, the populist policies adopted by the governments of developed countries are often the driving force of the crisis. The psychological pressure caused by technological changes and the widening distribution gap often causes public dissatisfaction. Under the influence of the inability to change the status quo during the term of office and the promotion of vote politics, the government tends to adopt more populist policy declarations to appease the people.” (Liu He, 2013, p.10). Our government should also avoid adopting populist policies and avoid using policies to please and flatter populists.

(XV) Suicide, fraud, and other types of crimes will increase.

After the economy enters the “chased stage” or the “attacked from both sides stage”, due to the decline in residents’ income growth and the rise in unemployment, the suicide rate will rise rapidly, which has been proven by the data from Japan, South Korea, and the United States (Click to view the data).

I also noticed that the rise in the suicide rate usually does not start at the beginning of the economic deterioration, but rises rapidly several years after the economic deterioration.

I guess the reason is:

When the economy suddenly falls into the “attacked from both sides stage” from the “golden age”, most people do not believe that the economy will collapse, and they retain the good memories of the “golden age”, thinking that the economy is only temporarily not good. They can rely on their savings to get through it, and after a few years, the economy will improve; or they can work harder and do more jobs to offset the decline in income.

However, the root of the “attacked from both sides stage” is the decline in the investment return rate caused by real factors. In the face of this historical trend, individual efforts are not worth mentioning. In the years after the economic deterioration, they will find that no matter how hard they try, it is difficult to change their situation. After a series of blows, they completely lose confidence, feel hopeless, and choose suicide. And a person’s suicide will have a strong “demonstration effect”, encouraging those around them who have the same idea but have not yet implemented it to follow suit.

As mentioned earlier, I judge that the Chinese economy fell into the “attacked from both sides stage” in 2022. Since 2024, the phenomenon of suicide has been observed to increase significantly. I expect: 【1】The suicide rate in China will continue to rise in the next few years; 【2】The suicide deaths in China will be similar to those in Japan and South Korea, mainly men, and men will account for about 70%.

In addition, with the increase in unemployment, residents will hope to get compensation from the lottery, and the sales of lottery tickets will increase (click). Some residents will also go abroad to seek investment opportunities.

However, when residents cannot obtain income from legal channels, they will seek to obtain income from illegal channels, so various crimes will increase (click):

【1】The number of women who have lost their way will increase, and the price will decrease;

【2】Fraud cases will increase. This is because compared with theft and robbery, fraud has low cost, low risk, and high return (click);

【3】Theft and robbery cases will increase;

【4】Against the backdrop of the widening gap between rich and poor, some people will attribute their personal difficulties to society, and they will senselessly cut people on the street, drive cars to hit people, cut children in kindergartens and primary schools, and commit vicious cases such as hate killings.

In short, the years will no longer be peaceful.

VII. Capital Market: The stock market lacks long-term systemic opportunities, and the bond market is optimistic in the long run

(I) TFP and natural interest rates suppress the Chinese stock market

Now, extend the analysis framework of Figure 1 to the capital market.

Logic chain 9: The EPS growth rate, market environment, and investors’ risk preference of listed companies together determine the valuation of listed companies.

Logic chain 10: The EPS growth rate and valuation of listed companies together determine the stock price.

Logic chain 11: The stock price of listed companies, together with factors such as the industry distribution of listed companies, the investor structure, and the trading system and regulatory system, determines the overall index. The industry distribution of listed companies ultimately depends on the economic structure.

Combining logic chains 1-8, that is, real factors determine TFP, natural interest rate, and natural output, and through affecting the real economy, ultimately determine the EPS, ROE, and valuation of enterprises, and ultimately determine the stock price.

Analyzing the data and stock markets of Japan, South Korea, Taiwan Province, the United States, and other countries, it is found that the long-term bull markets that have appeared in the history of these economies are all related to higher TFP growth rates. When the TFP growth rate declines, a bear market appears accordingly (see here> for details).

Figure 12 Extend the analysis framework to the capital market

Source: Self-drawn

From 2001 to 2007, China’s TFP growth rate was higher, and it declined significantly after 2008.

Specifically, in the take-off stage of China’s economy, 1983-1987, 1991-1997, and 2001-2007, the TFP growth rate was far lower than the level of Canada, France, Germany, Spain, Italy, Taiwan Province, Japan, Israel, Malaysia, and other economies from 1955 to 1980. The reasons are:

【1】Unbalanced development of industries and regions.

【2】The intervention of state-owned enterprises and the government distorted resource allocation and reduced efficiency.

【3】There are problems with the growth method. Growth relies more on factor inputs rather than technological progress.

【4】Population aging.

China’s TFP growth rate has been consistently low since 2008. The reasons are:

【1】Population aging.

【2】The dual financing structure of state-owned enterprises and private enterprises, zombie enterprises, and government intervention have distorted resource allocation.

【3】China’s economy is already very large, and the general technological progress brings limited TFP growth to the entire economy. Unless there is a groundbreaking technological progress to improve the TFP growth rate of most industries in the economy, the TFP growth rate of the entire Chinese economy can be improved.

【4】Chinese companies are more accustomed to imitation than innovation.

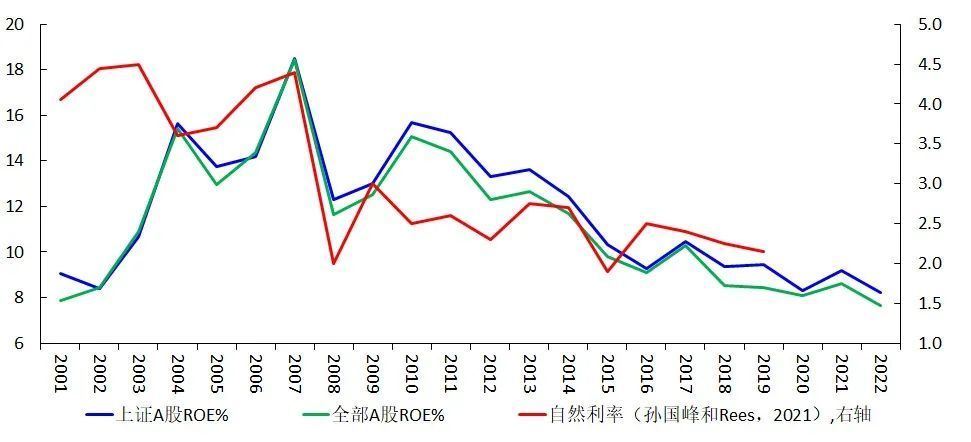

Analyzing the performance of A-shares since 1995, it is found that China’s TFP growth rate can explain the rise and fall of the Shanghai Composite Index and even the entire A-share market to a certain extent. The lower TFP growth rate has limited the level of investment return rate in the real sector, leading to the Shanghai Composite Index’s long-term difficulty in breaking away from 3,000 points. Even if it rises in the short term for some reason (such as the upward fluctuation of the inventory cycle in 2005-2007, and the large-scale water release in late 2014-H1 2015), it will eventually fall back to 3,000 points. In such an economic structure, there must be such a stock market.

The continuous decline in China’s natural interest rate has also suppressed the ROE of listed companies. In Figure 12, the correlation coefficient between the ROE of Shanghai A-shares from 2004 to 2019 and the natural interest rate is 0.70, and the correlation coefficient between the ROE of all A-shares and the natural interest rate is as high as 0.75. The previous article pointed out that the epidemic control in 2022 further lowered China’s natural interest rate and TFP, leading to a further decline in ROE, which is the root cause of the continuous bear market in the stock market since the beginning of 2022.

Figure 13 ROE and natural interest rate of each index

Source: Wind; Sun Guofeng and Rees (2021)

(II) Other reasons

In addition to the decline in TFP growth rate and natural interest rate suppressing ROE, there are also several factors that make it difficult for A-shares (including the Growth Enterprise Market) to continue to rise:

First, the efficiency of industrialization is too high, too involuted, which lowers ROE and shortens the product life cycle.

The efficiency of industrialization of Chinese enterprises is too high: 【1】They like to swarm in after new technologies and new products appear, invest on a large scale, lower the profit margin and ROE, and quickly lead to overcapacity. Taking new energy as an example, in just a few years, there are photovoltaic, wind power, lithium battery, and new energy vehicle companies all over the country, leading to a surge in performance in the short term, and then overcapacity, and everyone loses money. 【2】Quickly spread products in the market, and the penetration rate increases rapidly. The market promotion that may have taken 10 years to complete may be completed in three years. For example, the leaders of photovoltaic, wind power, and new energy vehicles are quickly pushed to the market and the penetration rate is increased under the promotion of policies.

Reflected in the stock price, it is to give a valuation of 80 times or even hundreds of times in the short term, and the stock price soars; then, with the rapid increase in the penetration rate to 30% and 50%, the expected future performance growth rate will decline, and the stock price will plummet. The slow bull market that may have lasted for 10 years or even longer is completed in 2-3 years, and then it is a sharp decline.

Second, investor behavior.

Because of the above reason, investors are afraid to hold technology stocks for a long time (worried about roller coasters), and prefer to do trend investment rather than hold them for a long time. This leads to: 【1】When hot industries and companies appear, they will swarm in, leading to a short-term surge in stock prices; then, they will sell in a swarm, leading to a sharp decline in stock prices. 【2】They place high hopes on technology stocks when they rise, and give them extremely high PE, PB, or PS; they are oversold when they fall.

Third, there are problems with the weight of the index.

As of the end of November 2023, the weighting of information technology in the NASDAQ index, the KOSPI, and the Taiwan Weighted Index is far higher than that of A-shares. Information technology accounts for 19.91% of the ChiNext Index, 30.3% of the ChiNext Composite Index, and only 12.04% of the Shanghai Composite Index. In contrast, the weighting of information technology in NASDAQ is 61.51%, in the Taiwan Weighted Index it is 59.3%, and in the KOSPI it is 39.5% (Click here).

The high weighting of finance, industry, and cyclical sectors in the Shanghai Composite Index and the Wind All-A Share Index does reflect the objective situation of low TFP growth in China. Therefore, it is normal for the Shanghai Composite Index to be difficult to break away from 3000 points in the long term; if it continues to rise, it is rather inconceivable because it violates economic laws.

(III) “The Stage of Being Besieged from All Sides”, the A-share market will lack good investment opportunities for a long time.

With the Chinese economy entering the “stage of being besieged from all sides”:

【1】The return on investment will continue to decline, and companies will inevitably become more involved in internal competition in order to compete for profits.

【2】As economic growth slows down, the growth rate of R&D investment is also declining, and the speed of technological progress will also slow down, further lowering the natural interest rate.

【3】Population aging will become more serious in the future.

【4】The reform process is slow.

Therefore, it will be more difficult to improve TFP and natural interest rates in the future.

Since the beginning of 2024, regulatory authorities have been sparing no effort to strengthen supervision and investigate illegal micro-behaviors, which led to a rebound in the Shanghai Composite Index from February to mid-May 2024, and a rebound in the ChiNext Index from February to mid-March 2024. And society seems to be creating an atmosphere that the stock market decline is caused by financial practitioners, so they should be打击, and as long as they are dealt with, a bull market will appear. This is actually a kind of populism. The most fundamental reason that determines the stock market is neither financial practitioners nor regulatory behavior, but the growth rate of TFP and the natural interest rate. In the absence of improvements in TFP and the natural interest rate, the A-share market will lack decent investment opportunities for a long time.

(IV) Investment themes to consider

First, the concept of low-volatility dividends, such as the public utilities industry. Look for stocks with high dividends, high yields, and low valuations. Some central state-owned enterprises can also be included in this category.

Second, in terms of new quality productive forces. Look for stocks with high technological barriers, large market space, and broad prospects. However, many industries (such as artificial intelligence, humanoid robots, hydrogen energy vehicles, controlled nuclear fusion, brain science, brain-computer interfaces, future displays, etc.) currently either lack widely accepted iconic products or are in the early stages of development, and short-term performance is not visible, so they are still mainly themed speculation.

Third, the concept of going global. However, the market space, political environment, and competitive environment faced by Chinese companies going global are completely different from those faced by Japanese companies 30 years ago, and careful discernment is needed (Click here).

Fourth, opportunities brought about by the rise in total demand. However, as mentioned earlier, it will be difficult for China to have a standard inventory cycle in the future, and the rebound in the growth rate of total demand will be very weak, so it is difficult to find investment opportunities from this perspective.

(V) Long-term outlook for the bond market

As mentioned earlier, in the long run, the yield on China’s long-term bonds will fall to 0, or even negative, so long-term bonds can be viewed favorably.

VIII. Policy Recommendations: Do Everything Possible to Delay the Decline in Return on Investment

(I) In terms of short-term demand management policies

1. The central bank should significantly lower the nominal interest rate by at least 70BP to bring the real interest rate in line with the natural interest rate, and restore the interest rate policy to a neutral or loose stance.

2. Do not try to raise the yield on long-term bonds, and it is also impossible, and it is not beneficial. It is recommended to maintain a lower yield on long-term bonds, so that residents, enterprises, and the government can convert the high-interest debt into low-interest debt, improve the balance sheet, which is a necessary prerequisite for economic recovery.

3. The central bank should participate in the trading of government bonds as soon as possible to accumulate experience for QE; conduct fiscal deficit monetization when necessary.

4. Do not pay too much attention to external equilibrium. When necessary, allow a more significant depreciation of the exchange rate (Click here).

5. The fiscal department should dare to significantly increase leverage and raise the fiscal deficit to (for example) 6% or even higher. Issue special treasury bonds:

【1】The central government should take the lead in investing in key national projects, especially scientific research projects, and quickly solve the problem of being stuck by the West;

【2】Establish an industrial fund (similar to the semiconductor big fund) and spare no effort to develop new quality productive forces, such as AI, humanoid robots, brain science, etc., to ensure that we do not fall behind in the technological competition with the United States.

【3】Reduce taxes for specific resident families, or even distribute cash, to stimulate consumption;

【4】Strengthen policy coordination among various government departments and prohibit the introduction of contractionary policies.

(II) Long-term solutions (supply-side policies)

Since the root of China’s economic problems is the decline in the return on investment caused by real factors, the fundamental solution is to start from the real factors and try to delay the decline in TFP growth and natural interest rates. This includes two aspects: reform and innovation.

1. Reform all systems and mechanisms that hinder technological progress. For example: promote the bankruptcy of zombie enterprises; prohibit discriminatory policies against the private economy, and enjoy the same treatment as state-owned enterprises in all aspects such as financing and market access; reform the distribution system, fiscal and taxation system, etc., and release institutional dividends.

2. Reform all systems and mechanisms that hinder innovation. For example, reform the scientific research system, education system, integration of industry and finance, intellectual property system, and business environment to cultivate an environment for innovation.

3. Streamline government staff. Abolish government activities that cannot improve economic efficiency, and reduce the number of people supported by the government; reduce government expenditures that cannot produce effectiveness.

4. Cut off the government’s “busy hands”, and put an end to the government’s arbitrary intervention in the market and industry, so that the market truly plays a fundamental and decisive role in resource allocation.

5. Reform population policies, ethnic policies, and religious policies. Abolish ethnic divisions, and there is only one ethnic group in the country, encouraging intermarriage and integration. Abolish reverse nationalism policies, especially discriminatory policies against the Han ethnic group, and everyone is equal. This is the fundamental guarantee for the long-term stability of the country.

Reform and innovation cannot stay on paper, but must be implemented. Effectively improve TFP growth and delay the decline in natural interest rates through reform and encouraging innovation. Especially in newly emerging technological fields (such as AI), we must not fall behind the United States and must seize every opportunity to improve productivity.

IX. Suggestions for Ordinary People

Finally, I would like to give a few suggestions to ordinary people like me:

The growth of the Chinese economy over the past 40 years has been a miracle in the entire history of mankind. It is brought about by the institutional dividends, demographic dividends, and broad technological progress released by reforms. We ordinary people happen to live in this era, and with our own efforts, we have shared the benefits brought by economic development. But miracles are always short-lived, and prosperity will eventually fade away. Such a large economy cannot always maintain a “golden age”. “Being besieged from all sides” and “being chased” are the norm. Understanding the characteristics of this historical stage can enable us to make better choices.

First of all, you must maintain your learning ability at all times. Through learning, you can improve your skills, adapt to industrial changes, and resist the impact of the times. Through learning, you can also improve your cognitive ability and discernment ability, avoid stepping on mines and pitfalls in times of economic downturn, avoid being misled by unhealthy trends of thought, and avoid risks, which is victory.

Secondly, do not easily invest in equities and commodities, including speculating in stocks, buying stock funds, and starting your own business (as a shareholder). Facing the pressure of long-term deflation, keeping cash and lowering expectations for returns is victory.

Thirdly, although personal efforts are insignificant in the face of the great historical trend, life should not be wasted in following the trend and giving up on oneself. You must maintain a strong inner self at all times and never give up hope.

Finally, I would like to end this article with the last sentence of the novel “Gone With the Wind”:

Tomorrow is another day!

References (Only the literature directly cited in the text is listed, and more literature can be found by clicking on the hyperlinks in the text) [US] Ming Gu, translated by Haixiang Yu, “The Great Recession”, Oriental Publishing House, November 2008. [US] Ming Gu, translated by Zhong Xu and Qing Ren, “The Economy Being Chased”, CITIC Publishing Group Co., Ltd., November 2023.

Lewis, Arthur, 1954, “Economic Development with Unlimited Supplies of Labor”, Manchester School, Vol. 22, No. 2, 139—191.

Yi Gang, “China’s Interest Rate System and Interest Rate Marketization Reform”, “Financial Research” 2021, No. 9.

Yi Gang, “The Autonomy, Effectiveness, and Economic and Financial Stability of Monetary Policy”, “Economic Research”, No. 6, 2023.

Sun Guofeng, Daniel M. Rees, “China’s Natural Interest Rate”, Discussion Paper of the Monetary Policy Committee of the People’s Bank of China No. 2021/01.

Phelps, Edmund. The Golden Rule of Accumulation: A Fable for Growthmen, The American Economic Review, Vol. 51, No. 4 (Sep., 1961), pp. 638-643. [US] Edmund Phelps, translated by Yanren Zhang, “The Golden Rule of Economic Growth”, Machinery Industry Press, 2015.

Minami, Ryoshin, 1968, “The Turning Point in the Japanese Economy”, Quarterly Journal of Economics, 82 (3), 380—402.

Edited by Liu He, “Comparative Study of Two Global Crises”, China Economic Publishing House, February 2013.

—————————-

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.