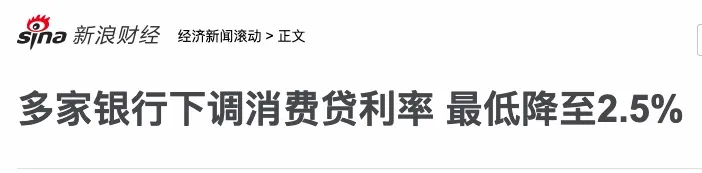

Since the announcement last week to boost consumption, banks have acted very quickly. This weekend, they lowered the interest rates on consumer loans. They did two things:

- First, they renewed loans for those who couldn’t repay, as mentioned above.

- Then, they rolled the interest rates down to the lowest in history, with the rates of most commercial banks dropping below 3%, and the lowest reaching 2.5%.

For example, according to reports, China Merchants Bank’s Flash Loan has a limit of 500,000 yuan. Recently, they’ve been running promotions, and the interest rate can be as low as 2.58%, I don’t know if any friends have tried it.

It should be the lowest consumer loan interest rate in history, only a few percent. If you didn’t have to repay the principal, it would be almost the same as giving away money. The reason for being so anxious is that the consumer market hasn’t been doing well since the beginning of this year. Don’t just focus on the fact that Nezha broke 2 billion in box office. Are there any movies released after the Spring Festival that have any buzz? I don’t even know what movies there are.

Of course, we still have to use data to speak. The price index from the statistics department in February shows that the consumer price index for residents in February decreased by 0.7% year-on-year, and decreased by 0.2% month-on-month. Considering seasonal factors, using year-on-year is more valuable, but this drop in February is far greater than the same period last year. In February 2024, it actually increased by 0.7% year-on-year.

This matter is more serious than imagined, especially considering that the friends who do statistics have directly given the drop. Combined with the art of statistics law, we can know the actual situation. You can search for how the situation is for young people aged 16-24 looking for jobs this year. Last year, many shops made short videos just to complain about consumption downgrading. This year, I’ve seen many videos saying that no one is consuming. You see, whether it’s downgrading or not is no longer important, what’s important is, why is no one going out to buy things? Many people don’t understand a question, is it good or bad for the prices of consumer goods to decrease. Why do the price decreases make everyone so anxious? The answer to this question actually depends on your identity, whether you are looking from the perspective of a producer or a consumer. This truth is self-evident, everyone is both a producer and a consumer.

For example, if the price of grain drops, are you happy? If you are a white-collar worker, of course you are happy, you can buy more grain with your current salary, but what if you are a farmer?

For example, if the delivery fee for takeout drops, are you happy? As someone who orders takeout, of course you are happy, but what if you unfortunately lose your job one day and go to deliver takeout?

The so-called ‘pulling the trigger when young, and the bullet hitting your own heart in middle age’ has a very concrete story, which is that a programmer designed a very complex algorithm for managing delivery personnel, which exhausted the delivery guys, and then he lost his job and went to deliver takeout and was almost killed by the algorithm.

The price of consumer goods itself includes the labor costs of everyone in the production and transportation of this product. If everyone thinks that a certain product should not be so expensive, then everyone in the production and sales of this product is considered to be worthless.

Considering that a product will require many links from production to circulation to sales, I remember that the textbooks in junior high school all mentioned where the profits go. When the terminal stores start to make videos saying that the cold is biting, then the manufacturers and raw material suppliers (especially scattered individual businesses) at the forefront of the chain don’t know how cold it is, and may already be shivering.

This is why it is urgent to boost consumption. In fact, there are many ways, such as what many economies often use, which is to directly give money. How much money did the US give out during the mask period? It was like scattering money from a helicopter, and consumption did indeed grow for a long time.

Or, it is a method that is very suitable for our national conditions, to increase the retirement pension for rural retirees. After they have security, the money they save, the money their children send to them, can be taken out to spend, and it can also solve the serious imbalance in retirement pensions among different groups.

But what I didn’t expect was that between giving money and raising wages, a strategy that no one noticed was used, which is lending. You think the interest is too high, right? Lower the interest rate, is it enough to lower it to below 3%? If it doesn’t work, lower it to 2.5%; worried about not being able to repay the loan, right? It doesn’t matter, we’ll renew your loan later. To be honest, this wave of loan interest rates is really sincere. A 2.5% consumer loan, when did everyone get this treatment from the bank? It can only be said that the banks are now being rolled over, but what is the biggest problem with lending to individuals for consumption? It is to repay the principal. Then many people, including you and me, have to consider the current situation, whether we can apply for a loan.

The premise of leveraging is that the expectation must be good. If the expectation is not good, I haven’t heard of anyone with bad expectations trying to reverse the expectation by leveraging consumption.

However, under the credit currency system, if you want to create a new increase in currency flowing into the market, you can only lend. It’s just a matter of whose head this account is recorded on, which is very important. For example, many economies issue government bonds and then scatter money. After the Japanese real estate bubble burst, that’s how they did it. The US also did it. In layman’s terms, this is called debt swap, by issuing money, to swap everyone’s debt into the debt of the whole society. Everyone has the motivation to consume, to buy, buy, buy, and as for the future, then repay it through other tools, if it really doesn’t work, then borrow new to repay the old.

The concept of debt being on everyone’s head and on an individual’s head are two different concepts. If it’s on one person, they have to live frugally to repay the money. If it’s on everyone, then it’s on everyone. The law does not blame the masses, and debt does not blame the masses. I think a very important reason why we haven’t done this is that the local government debt pressure is already very high. There have been many news reports about debt resolution in recent years, and the whole society has been struggling to hold up this part of the pressure. As for the individual consumption part, we can only give discounts, give encouragement, and at most give emotional value. If you are having a hard time now, who can hold up your present? The meaning is obvious, it is your future self.

You can only borrow a little from ‘him’. You say, what about the future? Li Bin will figure out the matter of Weilai. Many things cannot be sent directly in the article,

Welcome to add WeChat to chat: -END-March 24, 2025-

*The cover photo of this article is from “Beiping No War”*All-platform account: Norway TALK*Welcome to forward to Moments with one click on the left, and like and view on the right

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.