The following article is from 说财猫 Author 猫崽

The eve of 930, it boiled.

Starting from 9:30 p.m., policies emerged one after another.

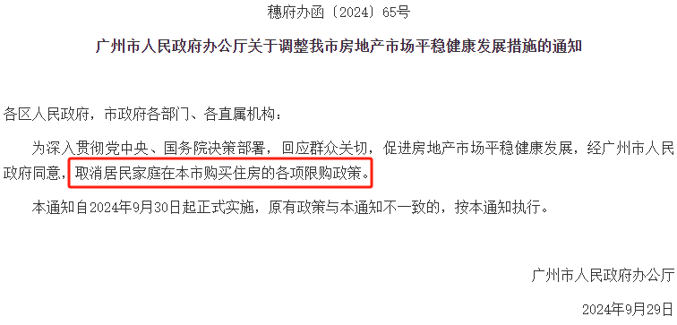

Until I saw Shanghai and Shenzhen re-launching new real estate policies, and then the news that Guangzhou had completely lifted purchase restrictions.

First-tier cities, the first to completely lift purchase restrictions, is Guangzhou.

They are all first-tier cities, but the differences are quite large.

Shanghai’s new policy this time, simply put, is Guangzhou’s previous version of the real estate policy:

5 changes to 2, first payment 15%, non-Shanghai social security continuous payment for one year, cancellation of luxury housing standards, etc.

Shenzhen is just a gesture: first payment 15%, lifting sales restrictions, etc.

Instead, Guangzhou, just doesn’t pretend.

Guangzhou’s purchase restrictions began in October 2010.

Senior people in the circle sighed that the purchase restrictions blocked many outsiders.

The purchase restriction policy, which lasted for 14 years, officially came to an end today.

Is it a relief? Not necessarily.

Why does Guangzhou become the only one among the first-tier cities to completely lift purchase restrictions?

Is it because it’s poor?

Indeed, after all, there is too much to bear.

In the first half of the year, Guangzhou’s GDP growth was only 2.5%.

2.5%, 2.5%… A first-tier city… at the bottom

In the past, real estate, automobiles, and foreign trade were all Guangzhou’s “trump cards”.

Now the auto industry is booming, and the trade war continues…

Guangzhou’s real estate development investment has also experienced 23 months of negative growth, and the longer it hovers at the bottom, the more it hurts.

Real estate, as the economic arm of Guangzhou, cannot be broken.

So Guangzhou is so determined to open up.

Guangzhou’s real estate development investment cumulative growth performance (from 2021 to present)

Most importantly, Guangzhou’s finances are poor.

First, land sales revenue has declined for three consecutive years.

And Guangzhou’s land revenue accounts for a relatively high proportion of the city’s government fund budget revenue.

It’s a lie to say that it doesn’t rely on land sales revenue.

Yesterday, the land plot of the flour mill was sold for over 10 billion yuan, but this year’s land sales revenue is still far behind compared to previous years.

Secondly, the growth of Guangzhou’s general public budget revenue (mainly taxes) has greatly declined.

Last year, Guangzhou’s GDP growth was 4.6%, and the growth of general public budget revenue was 4.8%, barely outperforming.

The most critical thing is that Guangzhou’s corporate income tax and personal income tax have both declined.

It can be seen that Guangzhou’s profit-making efficiency has weakened, corporate profits have decreased, and personal income has decreased.

In the first 8 months of this year, Guangzhou’s general public budget revenue growth was only 1.1%.

Far lower than the GDP growth in the first half of the year.

The district-level revenue decreased by 0.6% year-on-year. The municipal level may still have porridge to drink, but it is already very difficult for the district-level finances to maintain growth.

The most important point is still the “mission” of Guangzhou’s three-level finance.

The tax retention ratio is low. After paying to the central government, a portion also needs to be paid to the province.

Guangzhou is also the only city among the first-tier cities to implement three-level finance.

Cat崽 previously calculated a set of comparable data. Guangzhou’s tax retention ratio is about 28%, far lower than Beijing, Shanghai, and Shenzhen.

Therefore, we cannot just blame it. After all, it also has to take into account the provincial finances.

In the 2024 fiscal budget, Guangzhou’s total revenue and expenditure table also reflects the heavy burden it bears:

The budget for intergovernmental transfer revenue (upper-level subsidies + lower-level transfers) is 63 billion yuan.

The budget for intergovernmental transfer expenditure (subsidies to lower levels + transfer expenditure) is 84.7 billion yuan.

Net outflow of 21.7 billion.

This has also made Guangzhou, which is not rich, begin to feel anxious.

It’s just that this time, betting on the complete lifting of purchase restrictions in the real estate market, will the real estate dividend come again?

If “completely lifting purchase restrictions” is not effective, what else can be done?

Purchase a house to obtain household registration? Zero interest rate?

Don’t be surprised, many countries have done this.

What we need now is not to save the market, but to saturate the market.

The future will definitely be possible.

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.