Last week, while browsing the bank app, I noticed a detail.

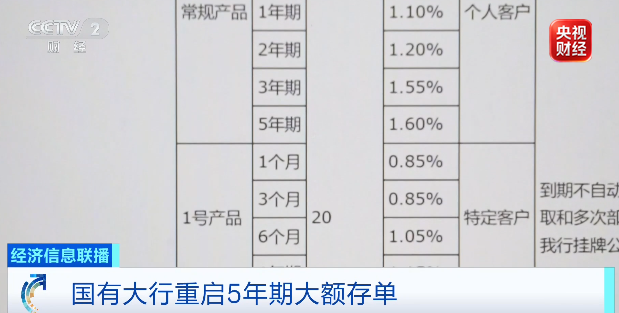

In China Bank’s new deposit products for July, 5-year large-denomination certificates of deposit have been relisted.

There are two types, with annualized interest rates of 1.6% and 1.55% respectively, both requiring a minimum deposit of 200,000 yuan.

Ping An Bank has also synchronized its 5-year product, with an interest rate of 1.65%.

This matter itself is not significant, but it is worth noting.

Because in the past two years, against the backdrop of continuously squeezed net interest margins, major banks have successively reduced medium- and long-term large-denomination certificates of deposit, and 5-year products once completely disappeared from the market.

Now it’s back, and not just from one bank.

Let’s first clarify the logic behind this seemingly contradictory move by the bank.

First, as everyone knows, the core profit model of banks is ‘borrowing short and lending long’, using low-cost short-term deposits to issue high-interest long-term loans.

But this model naturally relies on one premise: short-term deposits are sufficiently stable.

Once deposits move or market interest rates fluctuate, banks become passive.

Large-denomination certificates of deposit were once suppressed by banks five years ago because the interest rate environment was high at the time, and issuing high-interest long-term liabilities would lock in the bank’s funding costs.

But the situation is now completely reversed.

The current interest rate is in a downward trend, and a 5-year interest rate of around 1.6% is extremely low by historical standards.

By locking in a 5-year term of funds at this price, the cost of this liability will be 1.6% regardless of how market interest rates change within five years.

If deposit interest rates continue to fall next year, this funding will actually become expensive;

but if interest rates remain on the floor for a long time, then 1.6% is a cost-effective deal.

Many people are still waiting for this year’s interest rate cuts, but judging from the banks’ issuance of large-denomination certificates of deposit, there’s no hope in the short term.

The latest LPR data released by the People’s Bank of China on June 22 shows that both the 1-year and 5-year rates remained unchanged, with no reduction at all.

To translate: banks locking in 5-year liabilities are not betting on rising interest rates, but betting that interest rates will not rise significantly or fall significantly.

Banks are bearish on interest rate volatility itself, not the direction of interest rates.

More importantly, it’s about maturity matching.

Banks hold a large amount of long-term assets, such as housing loans, infrastructure loans, and local government special bonds, with maturities often spanning ten to twenty years.

If liabilities are all demand deposits or short-term deposits within one year, once depositors withdraw funds en masse or transfer them to wealth management products, banks will be forced to borrow funds at higher costs to make payments.

The role of 5-year large-denomination certificates of deposit is to add a layer of insurance to the liability side.

It locks a portion of funds into a five-year term, reducing the volatility of short-term liabilities and making the maturity structure of assets and liabilities more matched.

For banks, the value of liability stability is no less than the cost of liability.

A demand deposit that can be withdrawn at any time, even with an interest rate of only 0.3%, has a far greater liquidity risk exposure than a 1.6% deposit locked in for five years.

Of course, there’s also an accounting aspect.

There is an interest rate spread between 5-year certificates of deposit and corresponding loan interest rates.

The interest rates on loans issued by banks with maturities of five years or more, such as housing loans or long-term corporate loans, are generally above 3%.

By locking in 5-year funds at 1.6% and then matching them with long-term loans above 3%, the intermediate spread of nearly 1.5 percentage points can be locked in for five years.

With net interest margins already down to 1.4%, this spread is very attractive to banks.

Therefore, issuing 5-year large-denomination certificates of deposit is not a bet on interest rate trends by banks, but an active repair of the maturity mismatch in their balance sheets – reducing short-term liability volatility, locking in long-term stable funding, and maintaining interest margins without expanding risk exposure.

Once this logic is clear, the intention behind this move by the bank becomes very clear.

Banks themselves have no incentive to lower LPR, as net interest margins have already fallen into dangerous territory.

Local government debt has been converted into low-interest, long-term special bonds through multiple rounds of replacement operations, which are less linked to LPR, and policy resources prioritize protecting them.

Resident housing loans are fully tied to the 5-year LPR. Every interest rate cut benefits ordinary homebuyers, who are at the bottom of the priority for sharing the overall debt cost.

Coupled with the inversion of the Sino-US interest rate differential, further interest rate cuts would exacerbate capital outflow and exchange rate depreciation pressures.

With three constraints in place, interest rate cuts are basically out of the question.

Moreover, the marginal effect of interest rate cuts is diminishing.

The biggest bottleneck in the market now is not that loan interest rates are too high, but that ordinary people’s expectations for future income are weak, and they are hesitant to borrow and leverage up. Another 20 basis points reduction would be unlikely to stimulate a new wave of home buying or entrepreneurial enthusiasm.

Since interest rate cuts cannot bring in incremental loans, maintaining the status quo at least preserves bank profits and the portion of fiscal revenue from profit contributions.

But a more fundamental problem than interest rate cuts is that interest rate cuts themselves are finding it difficult to stimulate demand.

The biggest bottleneck in the market now is not that loan interest rates are too high, but that ordinary people’s expectations for future income are weak, and they are hesitant to borrow and leverage up.

Another 20 basis points reduction would be unlikely to stimulate a new wave of home buying or entrepreneurial enthusiasm.

Since interest rate cuts cannot bring in incremental loans, maintaining the status quo at least preserves bank profits and the portion of fiscal revenue from profit contributions.

In fact, looking at these matters together is quite interesting.

Banks are quietly lengthening their liability maturities, residents are silently saving money and paying off loans, and businesses are contracting investment and deleveraging.

In plain terms, all departments are repairing their own balance sheets.

Looking at things from a different angle makes them clearer.

For banks, deposits are their liabilities, and an increase in resident deposits means an accumulation of bank liability costs.

On the other hand, the contraction of the loan side means a decrease in asset returns.

Banks are caught in the middle, needing to ensure ample liquidity, operate profitably and efficiently, and reduce financing costs for the real economy.

In the past, some experts proposed the concept of a ‘reservoir and buffer zone’, and now banks are increasingly resembling that reservoir during economic adjustments.

Absorbing pressure first, suppressing profits, and digesting risks.

Even for the Big Four banks, completing various targets at local branches has become increasingly difficult, with cost reduction, efficiency improvement, and branch network contraction being routine operations.

City commercial banks and rural commercial banks are in an even tighter spot.

They rely heavily on small and medium-sized enterprise customers and individual business loans, which are precisely the areas where balance sheet repair is slowest.

Deposit acquisition costs are high, and their brands and channels cannot compare to large banks, while their asset-side risk exposure is significant.

Large banks can obtain long-term funds at 1.6% by leveraging their brand and channel advantages. Even if smaller banks want to follow suit, they may not attract deposits even by offering higher interest rates.

What if there is no room? The most likely outcome is accelerated mergers and reorganizations.

Risks are contained within provinces, institutions are consolidated, and as much as possible is digested.

Therefore, this trend line is already very clear.

Banks are repairing their balance sheets, so they are reissuing long-term certificates of deposit and tightening control over high-risk assets.

Residents are repairing their balance sheets, so they are saving money, paying off loans, and controlling consumption.

Businesses are repairing their balance sheets, so they are compressing investment, reducing debt, and holding onto cash flow. Policy sides are also repairing, with local government debt swaps, financial risk resolution, and fiscal revenue and expenditure adjustments.

The entire society is contracting risk exposure and reducing leverage levels.

This is not an isolated adjustment by a single department; it is the synchronized repair of an entire generation of balance sheets.

The relisting of 5-year large-denomination certificates of deposit is merely the latest marker on this trend line.

Once this is understood, many seemingly unrelated phenomena can be connected.

End of full text, thank you for reading. If you found it useful, please like, share, and follow.

-end-

A final note: I have created a “Planet” community group, which has been operating for 600 days. Friends with similar values are welcome to join.

I share some of my observations and thoughts in the community every day, and you can also ask me questions. Let’s strive together and enjoy the beauty of steady progress~

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.