What is the future of China’s economy in 2025? How will policies be adjusted? What are the market expectations?

Question 1: At the end of the year and the beginning of the year, the yield on government bonds fell rapidly. Is this a pre-pricing of the macroeconomy, or is it a pricing of the central bank’s interest rate cut and bond purchase?

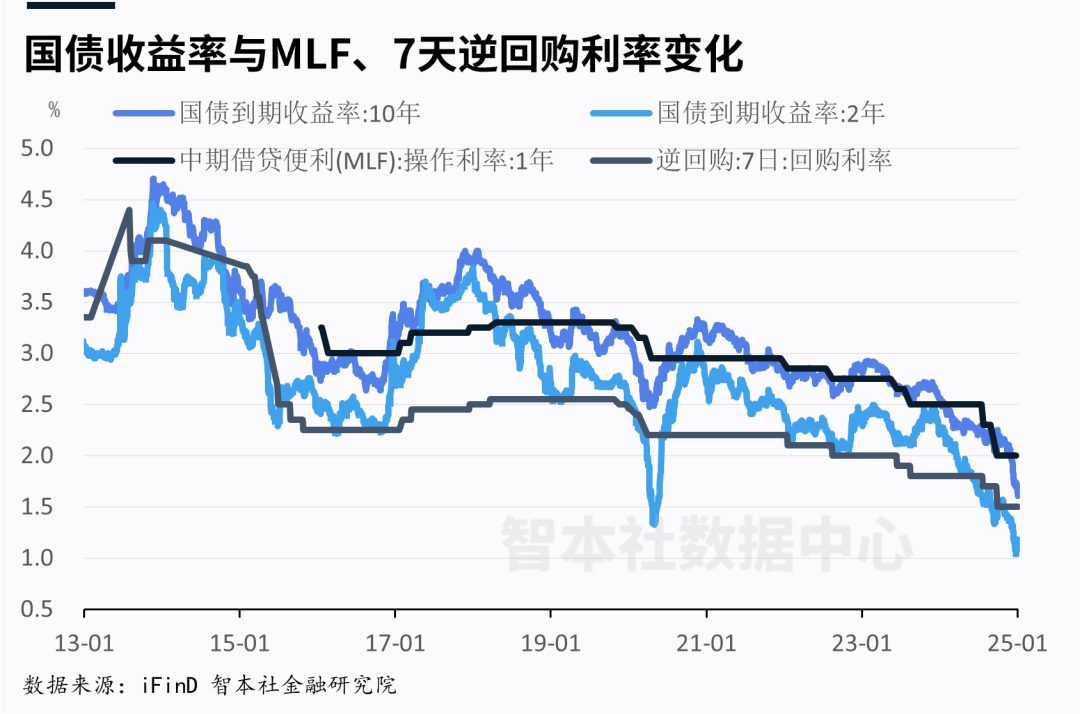

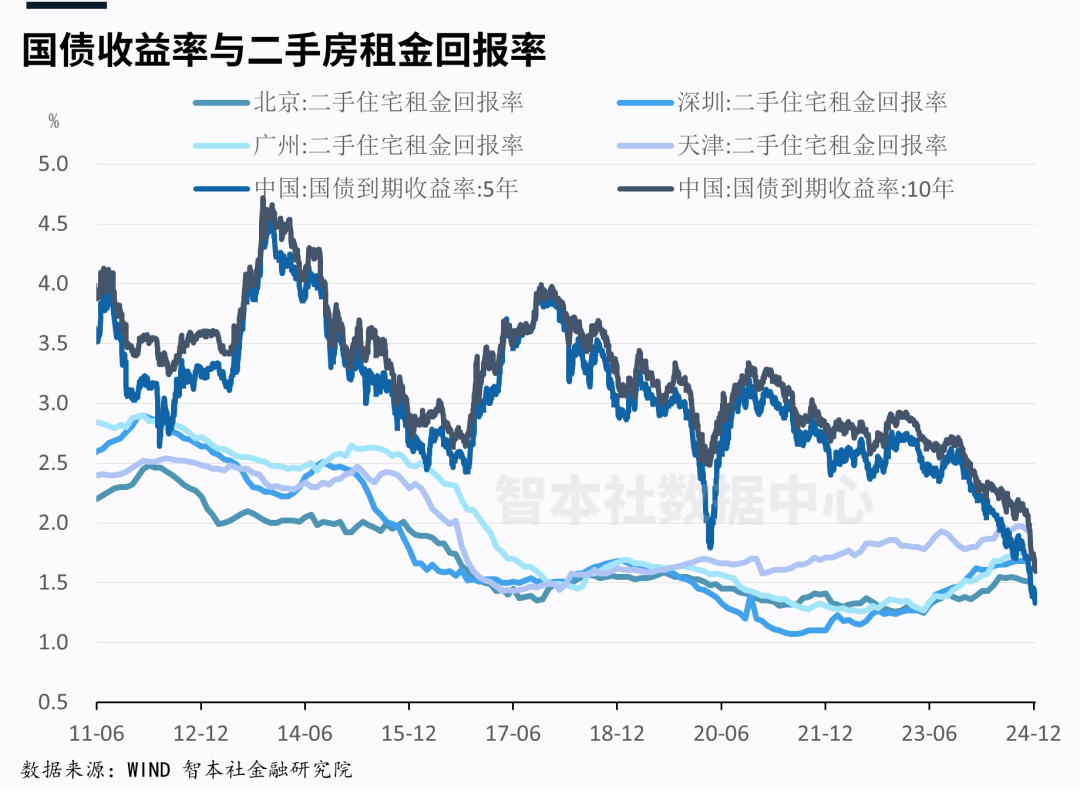

Data shows that in December 2024, the yield on 10-year treasury bonds accelerated its decline, with a drop of 40 basis points (BP) in just one month; on January 3, 2025, the yield on 10-year treasury bonds fell below 1.60% during intraday trading, hitting a low of 1.589%, once again hitting a record low.

As a price risk signal, the rapid decline in government bond yields, that is, the rapid rise in government bond prices, means that the market is heavily buying government bonds, and the risk aversion sentiment is strong, expressing the macroeconomic pressure and its expected increase.

At the same time, the central bank’s interest rate cuts, easing policies and expectations are direct factors driving the decline in government bond yields. Previously, high-level meetings have clearly proposed “moderately loose monetary policy”.

The market expects that in 2025, the central bank’s interest rate cut will be at least 40BP (7-day reverse repurchase rate), while in the past month, the yield on 10-year treasury bonds has fallen by 40BP. In other words, the yield on 10-year treasury bonds may have already factored in most of the interest rate cuts in 2025.

In the past, the interest rate on government bonds was long anchored to the Medium-term Lending Facility (MLF) rate. In 2025, the MLF may be lowered by more than 60BP, then the yield on 10-year treasury bonds may still have a 20BP decline space.

Considering that the central bank will also increase its bond purchase efforts in 2025, especially purchasing medium-term, long-term, and ultra-long-term treasury bonds, this will further push down the yield on government bonds. The current market may not have fully priced in the central bank’s bond purchases.

Since December 2023, the cumulative decline in the yield on 10-year treasury bonds has reached 110 basis points (BP). Considering the three major factors of macroeconomics, high debt/debt reduction, and aging, the bond bull market will continue, and the decline in government bond yields is a long-term trend. It is estimated that in 2025, the yield on 10-year treasury bonds will conservatively be below 1.5%, and may even fall to 1.3%.

Question 2: If the offshore RMB price exceeds 7.5, can the A-share market still maintain the performance after “9·24”?

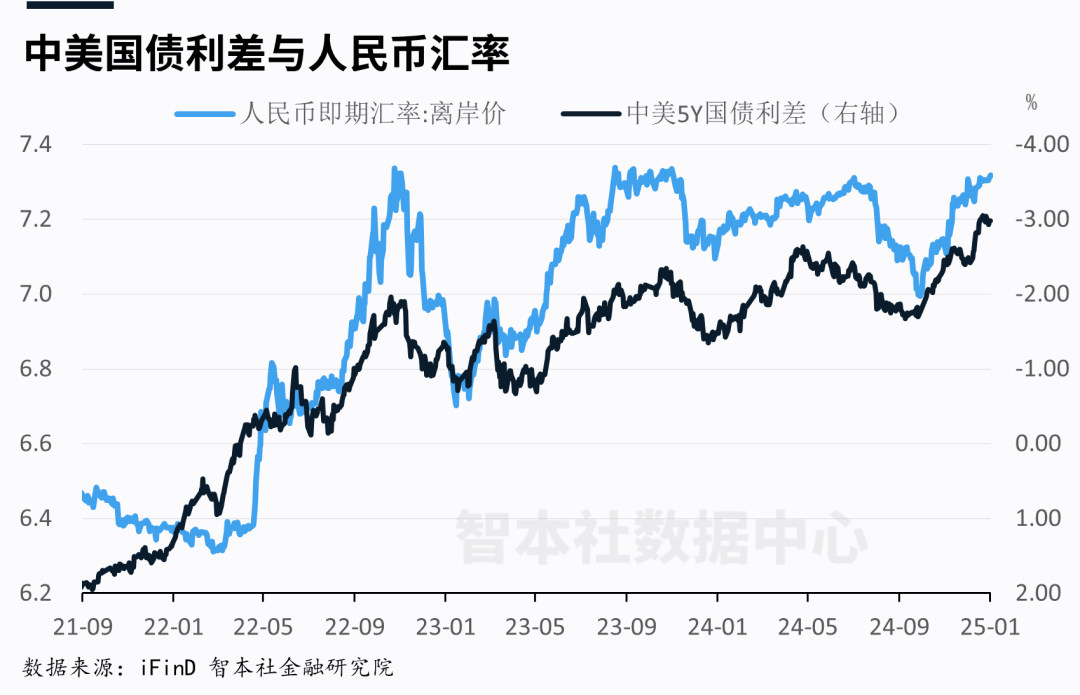

Generally, the widening of the interest rate spread between two countries will drive capital arbitrage across borders and push the exchange rate down.

Data shows that as of January 6, 2025, the yield on China’s 10-year treasury bonds is 1.61%, and the yield on US 10-year treasury bonds is 4.62%, the interest rate spread between the two is 3.01%, which has doubled compared to the beginning of 2024.

In 2025, both the central banks of China and the United States are in an interest rate cut cycle. Due to the stickiness of US inflation, the Federal Reserve may cut interest rates by 50-70BP; the People’s Bank of China may accelerate interest rate cuts, with a cut of more than 40BP. Considering that the current yield on China’s 10-year treasury bonds may partially factor in interest rate cuts, while the yield on US 10-year treasury bonds has not fully factored in interest rate cuts, the interest rate spread between the two may remain around 2.5% in 2025.

In 2025, the interest rate spread on government bonds remains high, and cross-border arbitrage motivation is expected to be strong, which is a direct factor driving the depreciation of the domestic currency.

Data shows that the interest rate spread between Chinese and US treasury bonds is consistent with the long-term trend of offshore RMB. Recently, the interest rate spread between Chinese and US treasury bonds has widened to a historic high, and the offshore RMB has also hit a historic level of 7.36 during intraday trading.

In 2025, due to the possible implementation of a comprehensive tariff plan by the United States, the expectation of RMB depreciation has increased, and some institutions predict it to be 7.7-7.8. Capital arbitrage across borders drives the depreciation of the RMB, and in turn, the depreciation of the RMB enhances the motivation for cross-border arbitrage, which will jointly reduce the valuation of RMB-denominated equity assets.

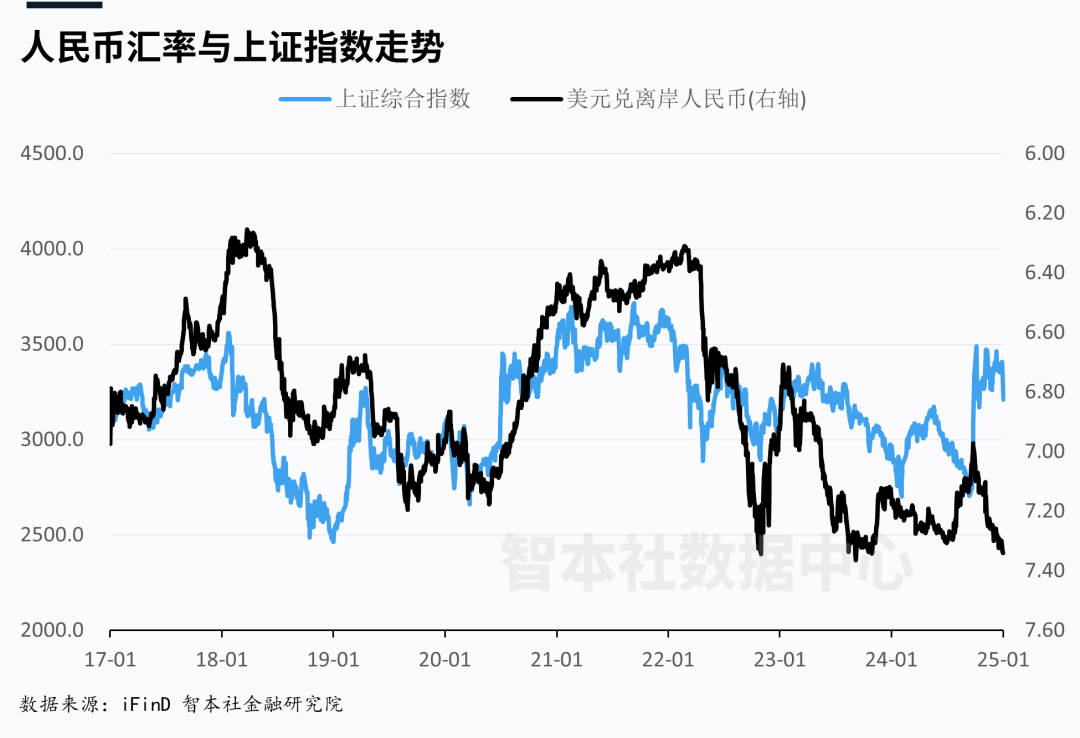

If the price of offshore RMB exceeds 7.5, can the A-share market maintain its current price and trading volume?

Data shows that there is still a certain correlation between the Shanghai Composite Index and offshore RMB. The underlying logic is that the stock market is a barometer of the macroeconomy, and offshore RMB is the price of all assets denominated in RMB, both of which are economic signals.

However, stimulated by the “9·24” policy, the trend of the Shanghai Composite Index and offshore RMB has shown a clear divergence, until the first few trading days of 2025, the two trends have become consistent again. The market seems to have suddenly realized that 2025 has arrived, and then priced in a hurry. If the offshore RMB depreciates in 2025, the A-share price should also return to the offshore RMB.

It is expected that there will be another wave of impact on the Shanghai Composite Index 3500 before the two sessions in the first half of the year, and it will return to normal in the second half of the year, but the trading volume is still higher than the first three quarters of 2024. For professional investors (individuals and institutions), there are still opportunities to make profits, but for ordinary investors, it is a market that is easy to lose money.

The strategy for ordinary investors is to choose high-dividend stocks. According to historical experience, as the interest rate spread between China and the United States widens, high-dividend stocks are more favored by investors.

Question 3: How large a scale is needed for unconventional counter-cyclical regulation, central bank interest rate cuts, and fiscal expansion to be effective?

The macro policy tone for 2025 is “unconventional counter-cyclical regulation”, “moderately loose monetary policy” and “more proactive fiscal policy”. This policy combination is unprecedented.

From the perspective of policy stimulus, what level are the current policies, and what scale is needed to produce results?

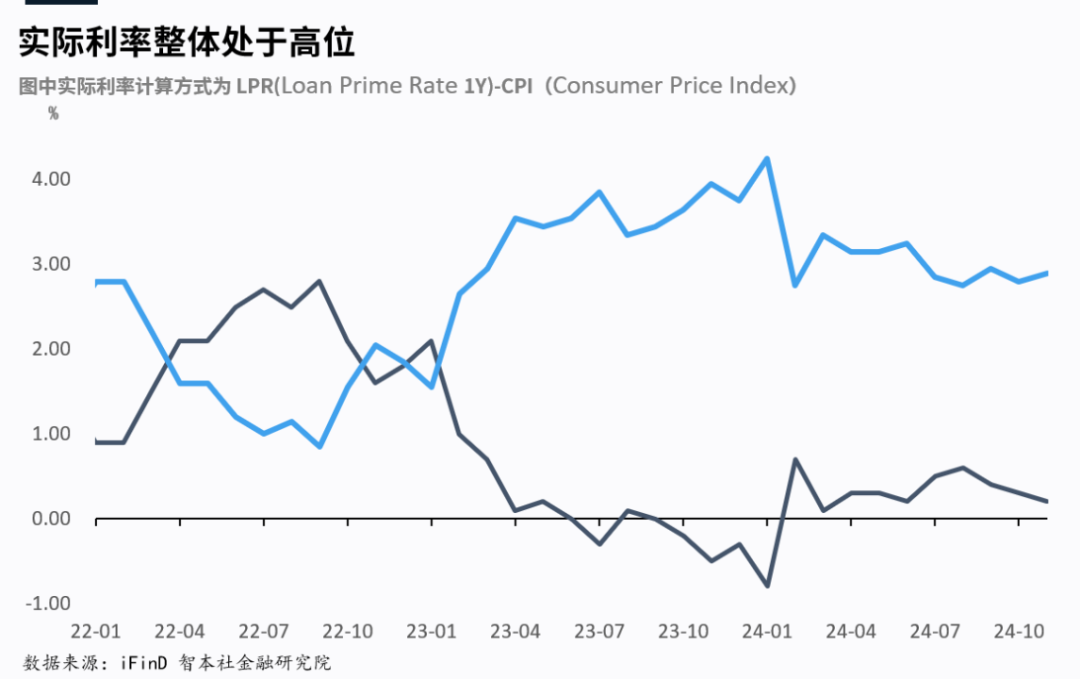

If the real interest rate (LPR-CPI) is used as an indicator, the current interest rate level in China is still relatively high, close to 3%, even higher than that in the United States.

The real interest rate reflects the real financing costs and debt burden in the market. Compared with the nominal interest rate and policy interest rate, it is a more accurate indicator to assess the strength of monetary policy.

In the past two years, the rate of price decline has been too fast, and the rate of interest rate cuts by the central bank has lagged behind the rate of price decline, and the real interest rate has been rising continuously, reaching a historic high at the beginning of 2024; after interest rate cuts in July and September, the real interest rate has decreased; but due to insufficient price repair, the real interest rate is still at a high level. This reflects the pro-cyclical characteristics of monetary policy.

If the requirements of unconventional counter-cyclical regulation and “moderately loose monetary policy” are followed to achieve the goal of stimulating price repair and investment demand recovery, the central bank should try to lower the real interest rate to below 2%. To this end, the central bank needs to cut interest rates by at least 80BP.

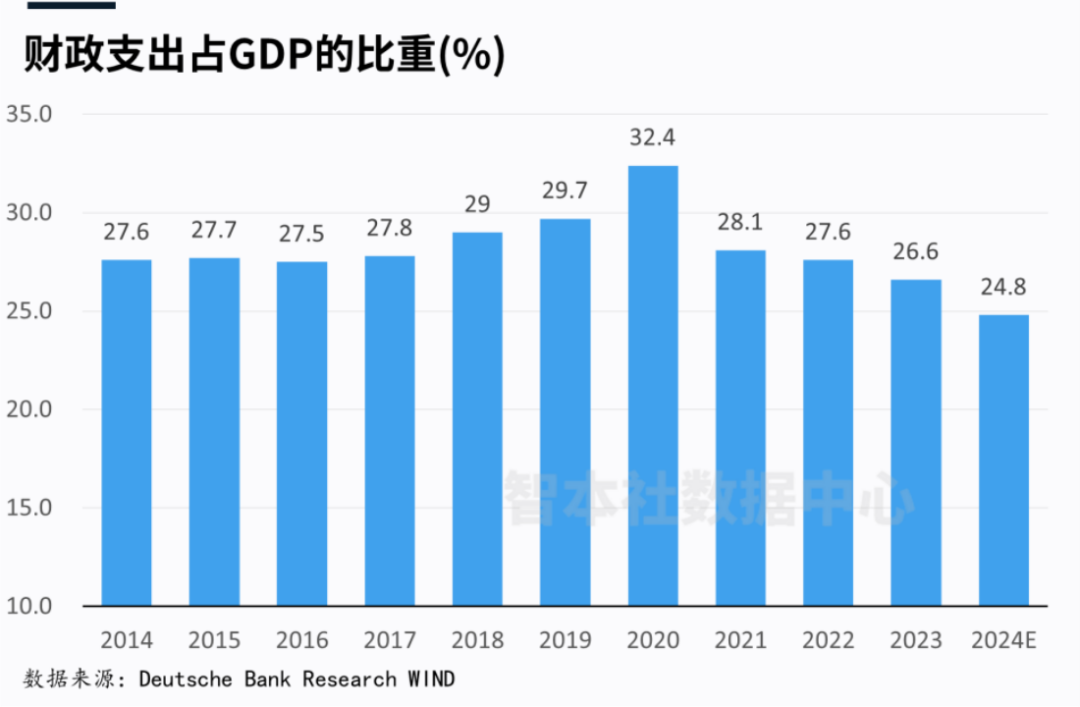

In terms of fiscal policy, if the proportion of fiscal expenditure to GDP is used as an indicator, the peak of fiscal expenditure was reached in 2020. In the following four years, constrained by real estate rectification, the decline in land transfer income, the control of city investment bonds, local debt reduction, and decision-making responsibility risks, the proportion of fiscal expenditure to GDP has continued to decline, falling to 24.8% in 2024, a decrease of 7.6 percentage points from the peak, even lower than the level 10 years ago. This reflects the cautious attitude of fiscal policy.

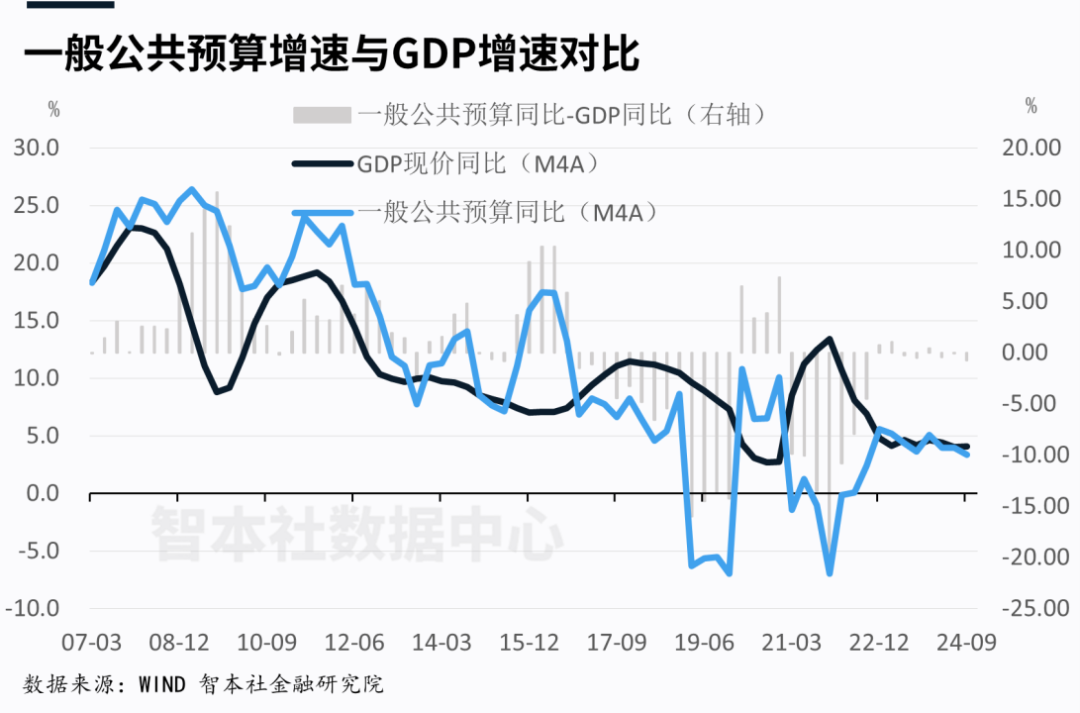

If the difference between fiscal expenditure and GDP is used as an indicator, the year-on-year growth of general public budget expenditure in the first three quarters of 2024 was 2%, and the year-on-year growth of real GDP in the same period was 4.8%, with a difference of -2.8%.

Looking at a longer period, from 2007 to 2016, the year-on-year growth rate of fiscal expenditure was basically higher than the year-on-year growth rate of real GDP, which shows that fiscal policy was in an expansionary phase at that time; from 2017 to the third quarter of 2024, the year-on-year growth rate of fiscal expenditure was significantly lower than the year-on-year growth rate of real GDP, and the difference between the two was negative for a long time; and the growth rate of fiscal expenditure decreased significantly. This shows that fiscal policy was in a relatively tight state during this period. In other words, the growth rate of fiscal expenditure lagged behind GDP.

In accordance with the requirements of “more proactive fiscal policy”, the growth rate of fiscal expenditure needs to be increased, and needs to exceed the growth rate of GDP, just as in 2020 to cope with the impact of the epidemic. If the general public budget expenditure in 2024 is 29 trillion yuan, and the growth rate of fiscal expenditure in 2025 wants to outpace the GDP growth rate, the general public budget expenditure needs to reach 30.5 trillion yuan.

Therefore, to achieve the effect of stimulating the economy, the central bank’s interest rate cut needs to outpace the rate of market interest rate decline and the rate of price decline, and also needs to outpace market expectations; the growth rate of fiscal expenditure needs to outpace the GDP growth rate. Of course, more important than speed and scale is structure and allocation—money should flow into ordinary people’s homes.

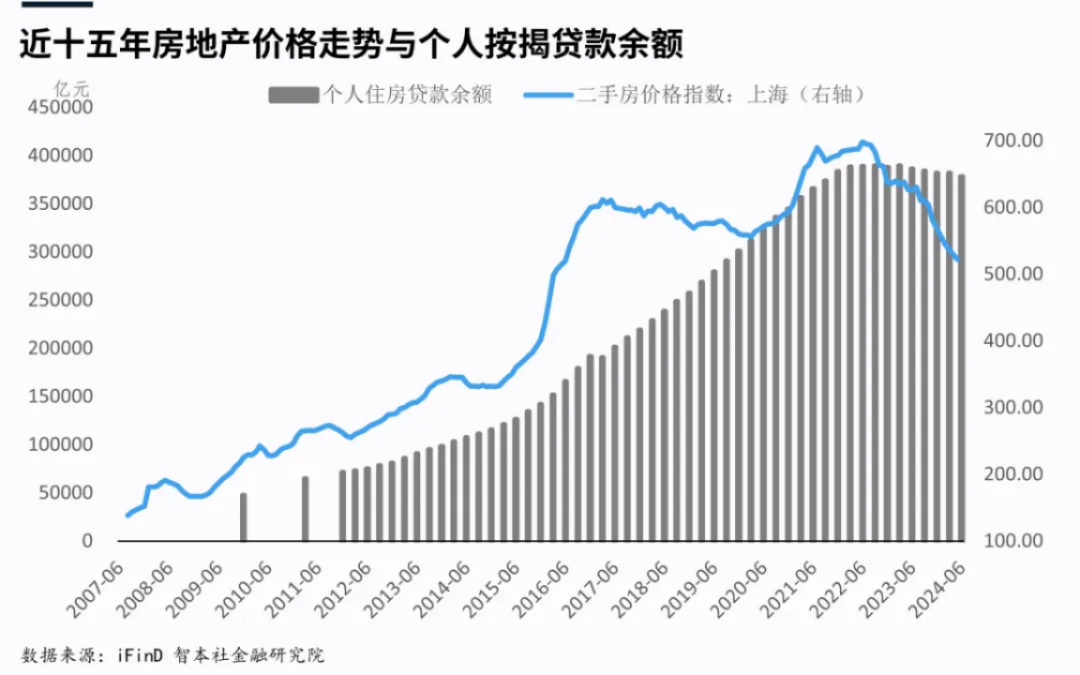

Question 4: The real estate market will gradually stabilize and recover. Is 2025 a good opportunity to buy a house?

The real estate market has gone through three years of rectification and a comprehensive decline, and has ushered in policy adjustments. The government has for the first time clearly put forward the goal of “stabilizing and recovering”.

After the “9·24” policy, the transaction volume in first-tier cities and big cities has increased significantly, and the pent-up, restricted rigid demand has been released. It is expected that the transaction volume will decrease after the release of rigid demand in the first half of 2025. However, the trend of stabilizing and recovering will not change.

In the next 2 years, the real estate market will gradually move towards “stabilizing and recovering”, with transaction volume first, followed by price, and investment and land market last.

Will the real estate prices continue to rise after stabilizing and recovering? The guiding direction of real estate policy is “stability”, not rise. The macro policy points to concentrating and mobilizing economic resources to invest in new drivers and bottleneck technologies, rather than wasting them on real estate. Considering multiple factors such as policy, credit, population, and debt, the prices of most houses in most cities across the country will no longer rise.

Regarding real estate investment and buying and selling, my view is:

First, China is entering the era of post-urbanization, post-real estate, and population aging. Most real estate has lost its asset investment value and has been transformed into consumer goods, so real estate is no longer a good investment.

Second, the proportion of real estate in household asset allocation is still too high. It is not recommended to continue to increase the allocation of real estate. The correct approach is to reduce the proportion of real estate and increase financial assets and liquid assets.

Third, if you want to invest in real estate, you can choose an optimized approach, replacing second-, third-, and fourth-tier cities, non-core areas, and old and small properties with high-quality properties in the core areas of first-tier cities and regional core big cities.

Fourth, in the stage of stabilizing and recovering, rigid demand and improvement demand can get on the bus, but try to choose high-quality properties in the core area, and at the same time try to control leverage.

Fifth, starting from 2025, the investment logic of real estate is changing: from asset investment to rent-to-sale ratio. With the decline in market interest rates and the overall decline in the yield of financial assets, the advantages of the rent-to-sale ratio are gradually emerging compared with the yields of government bonds and deposits. Considering the balance of allocation and hedging risks, some long-term funds will enter the rent-to-sale ratio of cities with population inflows, and stable properties.

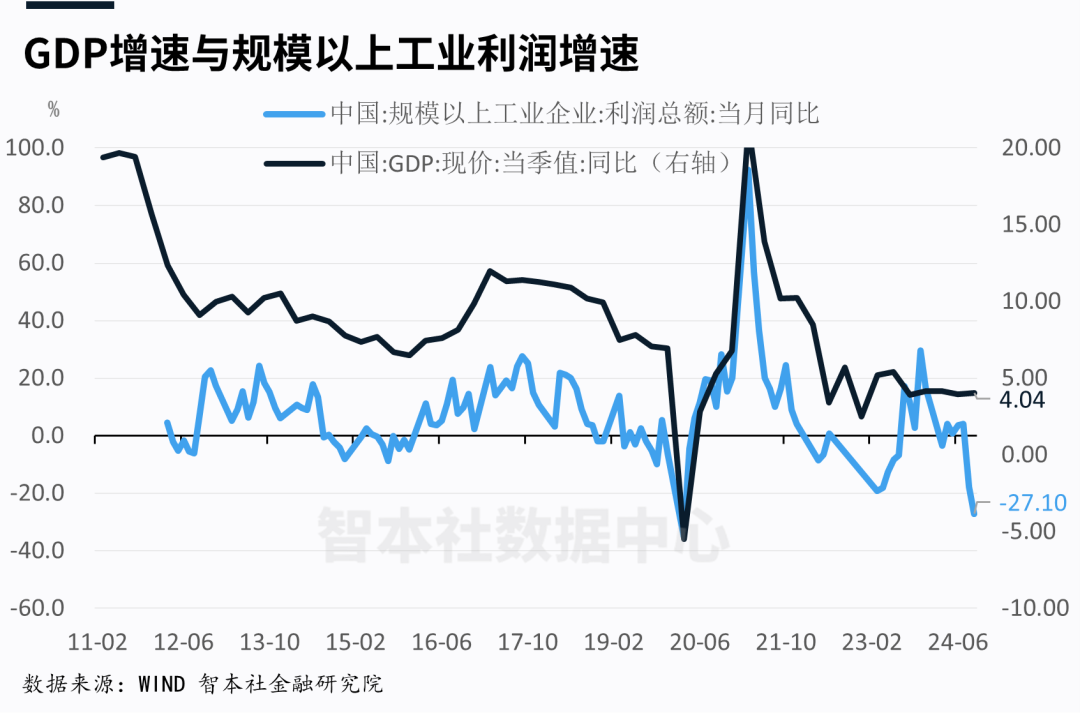

Question 5: How to understand the divergence between GDP growth and income growth in recent years?

In the long run, the trend of GDP is consistent with the trend of tax revenue, corporate income, and residents’ disposable income.

Data shows that from 2011 to the first half of 2018, the deviation degree (the difference between the year-on-year growth rates of the two) between GDP and tax revenue was only 1.79 percentage points. From the second half of 2018 to the third quarter of 2024, the deviation degree between the two widened to 11.47 percentage points. In the first three quarters of 2024, the deviation degree between the two also reached 9.3 percentage points.

Data shows that from 2011 to the first half of 2018, the deviation degree (the difference between the year-on-year growth rates of the two) between the year-on-year growth rate of GDP and the growth rate of profits of industrial enterprises above designated size was only 1.79 percentage points. From the second half of 2018 to the third quarter of 2024, the deviation degree between the two widened to 11.47 percentage points. In the first three quarters of 2024, the deviation degree between the two also reached 8.3 percentage points.

Usually, GDP cannot deviate from tax revenue and corporate profit income for a long time. It is expected that the GDP growth rate will return to the income growth rate in the future. If calculated according to the income method, GDP may be closer to the micro-feelings of the people.

In fact, GDP is the result, and income is the cause, and income is a more fundamental issue.

Question 6: Insufficient effective demand is insufficient consumption. How to improve residents’ consumption capacity and income?

After the market education and price feedback in the past two years, more and more people understand that the core problem of the current macroeconomy is insufficient effective demand, the problem of insufficient effective demand is insufficient consumption, and the problem of insufficient consumption is how to improve residents’ income.

The high-level meeting at the end of 2024 also proposed to “vigorously boost consumption and improve investment efficiency, and comprehensively expand domestic demand”.

Consumption is a function of household wealth, and household net wealth and its income expectations basically determine consumption.

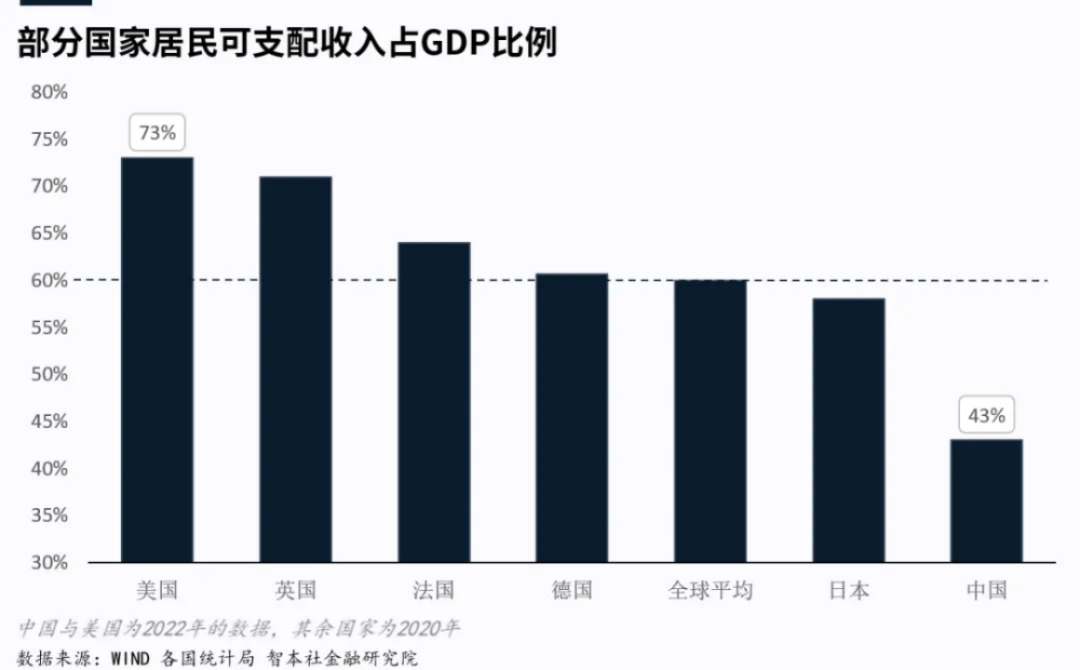

Data shows that the proportion of China’s household disposable income to GDP is 43%, which is lower than the global average of 60%.

This indicator almost determines a country’s consumption rate. The proportion of household disposable income to GDP in the United States is 73%, and the US consumption rate is also more than 70%. The average level of the proportion of household disposable income to GDP in the OECD is 60%, and the average consumption rate of the OECD is also more than 60%. The proportion of China’s household disposable income to GDP is only more than 40%, and China’s consumption rate is also only more than 40%.

The key to boosting consumption and expanding domestic demand in households is how to improve household disposable income.

On the supply side, release the vitality of enterprises, open up more investment areas for enterprises, release a more relaxed investment environment and public opinion environment, and strictly protect private property and enterprise management rights.

On the demand side, increase residents’ income, launch a national income doubling plan, directly distribute cash to residents through fiscal subsidies, enrich the social security fund through the transfer of profits from state-owned enterprises and the allocation of state-owned assets, and provide public housing for low- and middle-income families through state-owned land.

Of course, more important is institutional reform, especially the system surrounding income distribution.

Question 7: Is the market worried about inflation or deflation? Will expansionary monetary and fiscal policies trigger inflation?

In the past era of high growth, the market focused on the two indicators of real GDP and inflation rate, and worried about the economy overheating. However, in the past two years, I have repeatedly emphasized that we should pay more attention to nominal GDP and low inflation. Due to the weakening of prices, the growth rate of nominal GDP has decreased, even lower than real GDP. The decline in the growth rate of nominal GDP means a decline in nominal income. Due to the rigidity of debt, the decline in nominal GDP is an unfriendly trend for highly indebted families, enterprises, and governments.

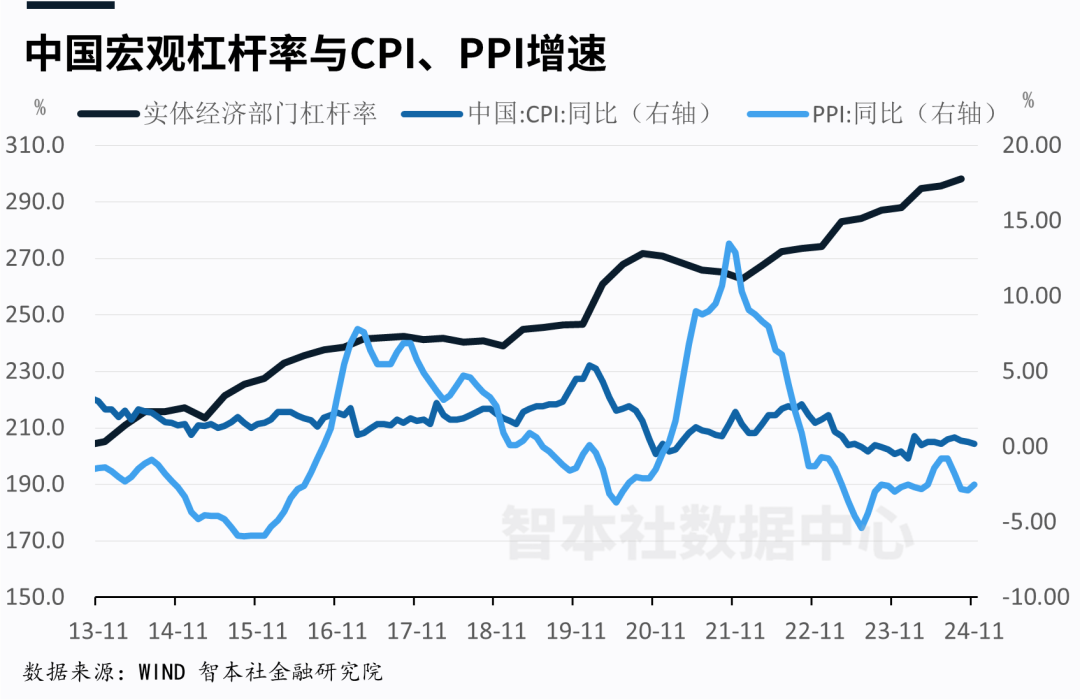

Data shows that in November 2024, the CPI increased by 0.2% year-on-year, and has not exceeded 1% for 22 consecutive months; the PPI fell by 2.5%, and has fallen for 26 consecutive months.

As this round of price declines gradually reveals the pressure on corporate income and debt, more and more people are aware of the risk of price declines. However, after the “9·24” policy was introduced, the intensity of monetary and fiscal expenditure expanded, and the market’s concern about inflation has significantly increased.

Macroeconomics has always regarded the inflation rate as an indicator to judge the macroeconomic prosperity and cycle, and the central banks of Europe, America, and Japan have set it as one of the goals or the only goal of monetary policy. In other words, whether or not there is inflation is almost equivalent to the economic situation, unless stagflation.

The core contradiction of the current economy is to boost inflation, not to worry about inflation.

In fact, issuing currency does not equal inflation, only when currency flows into the household sector is it possible to have inflation. If the inflation brought about by the growth of residents’ income and real expenditure is good inflation. If the inflation brought about by issuing currency to the household sector is bad inflation. But this is not the worst, the worst is to issue currency and not flow into the household sector and also trigger deflation.

Therefore, the central bank needs to take the inflation rate as the goal of monetary policy and strive to raise the inflation rate to 2%; more important fiscal policy needs to save more fiscal investment and transfer it to the household sector to increase residents’ income.

The market needs to think about a question: the “nemesis” of government bonds is inflation. The current government bond yield continues to decline, and the yield on 10-year treasury bonds has fallen to 1.6%. If the CPI rises to 2%, it means that the government bond yield turns negative.

In fact, a highly indebted economy is difficult to withstand high inflation for a long time. High inflation will lead to a decline in government bond prices, a rise in interest rates, and a deterioration in the debt situation.

Considering all factors, in 2025, inflation will still remain low, and the trend of declining government bond yields will not change.

Question 8: After the 9·24 policy, have the liquidity problem and the decline in the balance sheet expansion rate been resolved?

The liquidity problem is a problem that I have paid close attention to in 2024. In September, I wrote an article on the liquidity problem, “All Crises Are Liquidity Crises” (disappeared), and at the same time predicted in the social financing report that “the reserve requirement ratio cut and interest rate cut will come”.

Data shows that at the end of September, the narrow money (M1), which reflects the active flow of funds, decreased by 7.4% year-on-year, while the broad money (M2), including narrow money and savings, increased by 6.8% year-on-year.

The evolution path of the decline in liquidity is the decline in the rate of balance sheet expansion by residents—the decline in the rate of balance sheet expansion by banks—the financial accelerator effect—the decline in liquidity.

In 2024, the balance of personal housing loans continued to decline, which means that the ability of residents to expand their balance sheets has declined, and the housing loan market has shown a contraction phenomenon, which has led to the shrinking of the asset side of banks in personal mortgage loan business, which in turn weakens their ability to expand their balance sheets. Due to the accelerator effect of the financial system, the weakening of banks’ ability to expand their balance sheets has driven the decline in liquidity.

The liquidity problem is the key factor that triggered the “9·24” policy adjustment. After that, the central bank’s policy of interest rate cuts and reserve requirement ratio cuts, as well as the two monetary tools set up for the stock market, boosted market liquidity, and the trading volume of A-shares doubled.

Data shows that at the end of October and November, M2 increased by 7.5% and 7.1% year-on-year respectively, and M1 decreased by 6.1% and 3.7% year-on-year respectively, and the decline narrowed significantly compared with the end of September.

Among them, the “stickiness” of the outstanding housing loans led to the widening of the interest rate spread, triggering an early repayment wave, which is the direct reason for the decline in the balance of personal housing loans. The central bank has also canceled the system of adjusting the outstanding housing loans once a year, trying to prevent the decline in liquidity from the source.

However, the root cause of the decline in liquidity is the lack of purchasing power of residents. The lack of purchasing power of residents leads to weak investment by enterprises, and the lack of sufficient borrowing demand to boost interest rates and promote banks to continue to expand their balance sheets. It is expected that in 2025, macro policies will still focus on solving the liquidity problem.

Question 9: For the US comprehensive tariff plan and China’s response policy, how does the market expect and price?

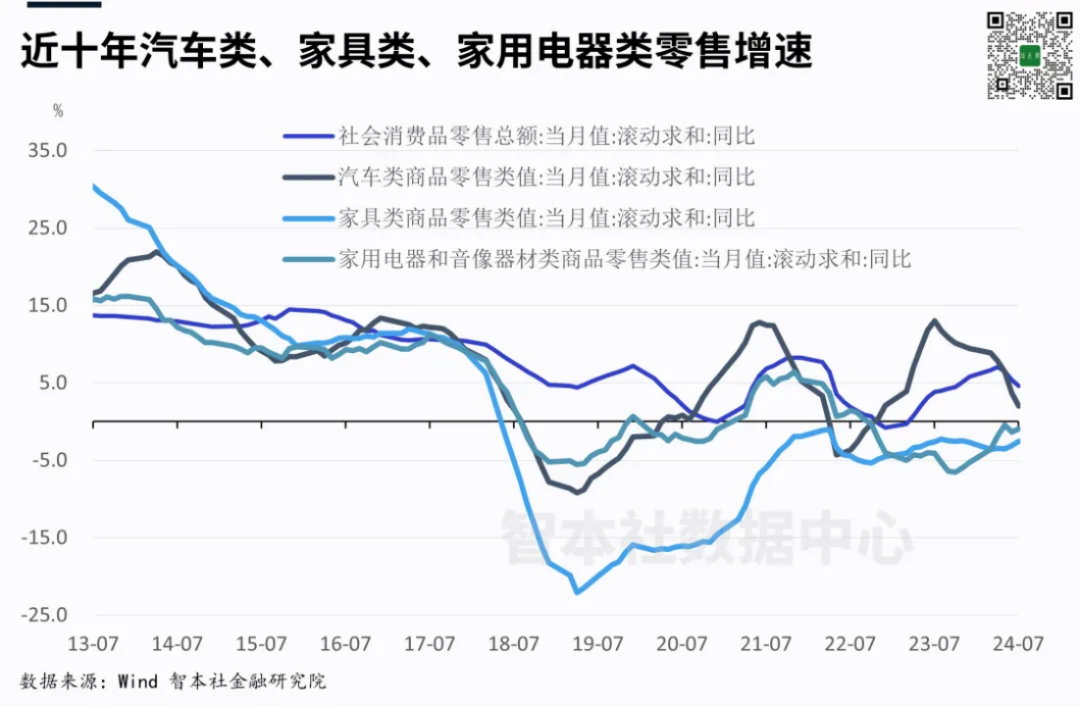

In 2025, some content of China’s macroeconomy is relatively certain, such as major categories of consumption, private investment, and infrastructure investment.

China is entering the era of post-industrialization, post-urbanization, and post-real estate. Major categories of consumption such as cars, furniture, and home appliances have crossed the inflection point, and infrastructure and real estate investment have weakened significantly. Subsidies such as the replacement of old for new can boost optional consumption, which is mainly affected by short-term income and expectations, but has limited driving effect on major categories of consumption and heavy investment. This also means that there is not enough demand to boost interest rates, and the market will enter an era of low interest rates.

There are also two major unpredictable events: first, when the US comprehensive tariff plan (and other policies) will be launched, how large the scale will be, and how it will affect China’s exports and macroeconomy; second, how large a scale of stimulus policies the Chinese government may launch to respond and what the effect will be.

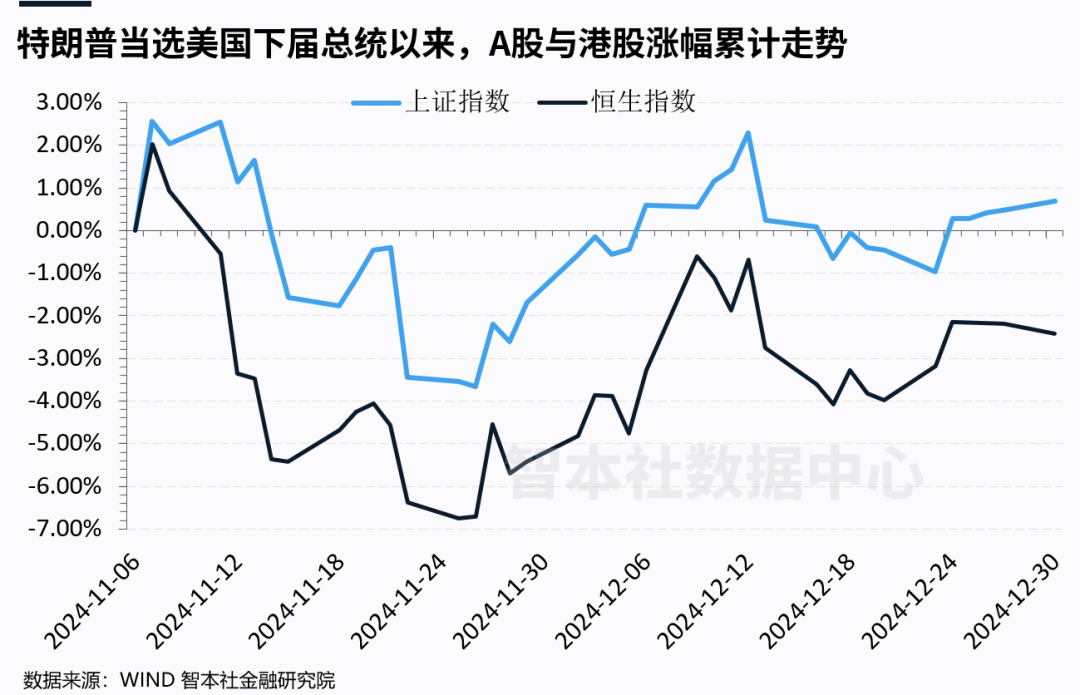

After Trump won the election, the Hong Kong stock market took the lead in pricing this risk event, and the Hang Seng Index retreated below 20000; the A-share market did not respond to this. The reason may be that many investors believe that the Chinese government will introduce large-scale stimulus policies to respond. However, entering 2025, the A-share market seems to begin to perceive the risk, and the Hong Kong stock market further prices it.

Interestingly, for the incident of Tencent being included in the list by the US Department of Defense, the US-listed Chinese stocks fell sharply, and the Hong Kong stock market also priced this risk event normally, while the A-share market regarded the bad news as good news, expecting that policies would promote the development of domestic alternative industries, and semiconductor stocks rose sharply, driving the A-share market to rise. This reflects the support of policy expectations for the A-share market. In fact, the Hong Kong stock market pricing is more sufficient, and it is expected that the A-share market will add pricing soon.

These two uncertain events and the market’s chaotic expectations are the key to influencing the trend of the macroeconomy in 2025.

Question 10: Entering the low-interest rate era in 2025, how should we invest?

Starting from 2025, major asset classes will officially enter the era of low interest rates and low yields. It is expected that the yields of most financial assets such as government bonds, deposits, insurance, and funds will fall.

Data shows that the yield on 10-year treasury bonds has fallen to 1.6%, the 3-year fixed deposit rate has fallen to 1.5%, and the insurance predetermined interest rate has fallen to 2.5%; it is expected that in 2025, the yields of these three products will fall to below 1.5%, 1.2%, and 2.0% respectively (conservative estimate). In addition, due to the sharp decline in housing prices in recent years, the rent-to-sale ratio of second-hand houses in Beijing, Shanghai, Guangzhou, and Shenzhen has increased, and will remain between 1.5%-1.8% in 2025.

This means that we will find it difficult to find major asset classes with yields above 2%.

When the yields of various assets continue to decline, what should we do?

The best way is to buy assets that can lock in yields as soon as possible. For example, government bonds and insurance are assets that can lock in yields. Buying insurance with a yield of 3% and government bonds with a yield of 2% before September 2024 can lock in the yield, and this yield will not decrease with the central bank’s interest rate cut and the decline in market interest rates. If you postpone buying these two categories of products to 2025, the yield will decrease significantly, and it is expected to be even lower in 2026.

This also means that as interest rates continue to decline, the window period for locking in asset yields is constantly shrinking.

If expanded to global core assets, the vision of household asset allocation will be broader, the yield will be more stable, and the hedging will be sufficient.

The simplest idea is to allocate the core assets of the world: the strongest and most stable currency, the sovereign bonds of the world’s most powerful countries, the stocks of the world’s most outstanding multinational companies, the policies of the world’s most powerful insurance companies, and the high-quality properties in the core areas of the world’s core metropolitan areas. If you are still not at ease, allocate a portion of gold for hedging.

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.