It does sound professional, safe, and even pretentious to attribute many of the current economic problems to “overcapacity,” making one appear knowledgeable about macroeconomics.

But the truly powerful aspect of this term is that it hardly requires further questioning.

Because as soon as you say “overcapacity,” the topic and responsibility automatically shift away from “distribution” and “income.” It’s as if the problem lies in too many production lines, companies working too hard, and people loving their jobs too much, rather than the fact that the common people’s wallets are too empty.

Therefore, the term “overcapacity” is merely a one-sided definition. From an economic perspective, it doesn’t even constitute a real proposition. But some economists seem to particularly love using this concept to talk at length, making themselves appear very knowledgeable.

The so-called “overcapacity” actually has only one implication: too many goods are produced and can’t be sold. Then the question arises, how can there be so many goods that they can’t be sold? Conversely, is the reason they can’t be sold necessarily because there are “too many goods”?

Is “too few people can afford to buy” a reason?

In fact, the so-called “overcapacity” has been taking turns, just changing industries. Twenty years ago, overcapacity was steel; ten years ago, it was cement; later, it was solar photovoltaic, LCD panels, and home appliances; then it was new energy vehicles, energy storage, batteries, and computing power…

One after another, the industries with overcapacity have changed again and again, but the variable of “insufficient income” has always remained stable.

The proportion of Chinese residents’ income to GDP has always been lower than the global average, even lower than many developing countries. So, is it the GDP that represents overcapacity, or is it that the income is not enough to buy?

OK, even if an economy is indeed producing too much, that’s still not right, because the most direct manifestation should be: goods become very cheap, residents can afford to buy anything, so consumption is highly prosperous, and the standard of living also improves rapidly.

But the reality is exactly the opposite—prices have indeed come down (because manufacturers are engaging in internal competition), but consumption has been slow to pick up. “Cheap but can’t afford to consume,” isn’t that very strange?

In a nutshell, the problem is not fundamentally about how much can be produced on the supply side, but about how much consumers can buy on the demand side.

Looking back to the early 1990s, there were indeed many things that couldn’t be produced at that time, so everything was expensive, and an ordinary TV set required more than half a year’s salary. Now? Almost everything is produced in abundance, but the proportion of income to GDP has always hovered at a low level.

Many of today’s “overcapacities” have a backdrop that seems very surprising: on the one hand, companies are desperately expanding production, local governments are also desperately attracting investment, and banks and credit institutions are desperately lending; on the other hand, there is a slowdown in the growth of residents’ income, unprecedented employment pressure, and a continuous decline in consumer confidence.

So why is income low? Everyone actually knows the answer to this question, but it’s not convenient to say it explicitly.

For a long time in the past, our growth model was essentially “lowering factor prices and raising investment returns.” Under this model, labor was cheap, land was cheap, and resources were cheap, but environmental costs were ignored, and what was exchanged was the rapid expansion of corporate profits, fiscal revenue, and investment scale.

This model is not necessarily bad—it was very useful in the early stages of industrialization. But it also has a natural aftereffect: the proportion of residents’ income to GDP has been low for a long time.

In other words, the economy is large, infrastructure and urban renewal are fast, but ordinary people will not become richer as a result.

We can also see that the most “prosperous” time for Chinese people was when housing prices soared, and consumption was indeed okay at that time, but that was a false prosperity.

Once housing prices go down, many “fake rich” immediately reveal their true colors and even fall back into poverty.

When the majority of people in a society can only maintain their living and cannot consume freely (such as ensuring one or two vacations a year, often participating in outdoor cultural and sports activities, and having more service consumption), then no matter how many cars or houses can be built, or how modern the city is, it can only be a paper prosperity—this is the so-called “overcapacity.”

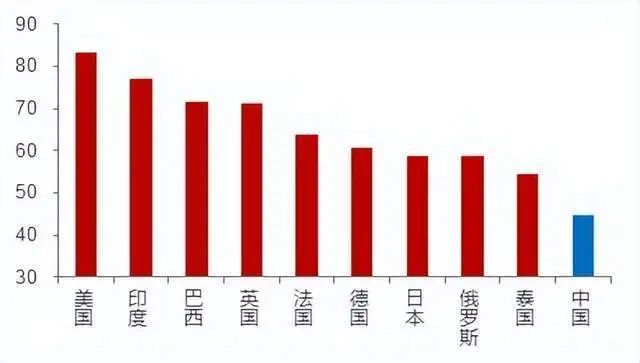

On the one hand, there is the world’s largest manufacturing industry (accounting for 30% of the global total), and on the other hand, there are the world’s most cautious consumers (the final consumption index is even lower than Thailand and India); on the one hand, there is a world-class industrial chain, and on the other hand, there is a highly uncertain confidence expectation for the future.

Capacity and demand, going in opposite directions.

The term “overcapacity” is actually an excuse, and sometimes it is even used to turn the tables: the decline in corporate profits is not due to excessive internal competition and vicious competition, but to overcapacity; the tight local finances are not due to the problem of fiscal expenditure itself, but to the “changes in the capacity environment”; the increasing employment pressure is not due to the problem of income distribution structure, but to the “downward cycle brought about by overcapacity.”

There are a group of “economists” and self-media people who explain it like this every day, and they also hope to “eliminate Europe and America” by the industry returning to a prosperous cycle.

In short, in their eyes, there is only industry, not the people.

Cycles can explain fluctuations, but not the long term.

If “overcapacity” has been occurring in different industries for more than a decade, it is not a problem of the industrial cycle, but a problem of the distribution mechanism.

It’s like a village that has built a world-class bread factory that can produce 100,000 loaves of bread a day, but the villagers can only receive a few hundred yuan in wages every month, and it’s a bit difficult to eat bread every day. So: is it the bread factory that has overcapacity, or is the villagers’ income too low?

What is truly scarce is never capacity, but a middle-income group that can spend money steadily, continuously, and with peace of mind. The successful experiences of developed countries around the world do not necessarily include large-scale industrialization, but they must have an “olive-shaped society” and a large middle-class group.

When a society begins to frequently discuss “overcapacity,” it often means that it has not seriously discussed “income growth” and “distribution structure” for a long time.

Finally, to prevent the trolls’ comments, let’s block their mouths first: this article is not to deny the importance of industrialization, but to emphasize that while industrialization is taking place, it must be accompanied by the improvement of income distribution to ensure the continuation of the healthy cycle of the economy.

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.