On March 26, China Merchants Bank disclosed its 2024 annual report.

According to the annual report calculations, in 2024, China Merchants Bank’s employee expenses were 68.09 billion yuan, with an average cost of 581,000 yuan per person. It is worth noting that this is the second consecutive year of decline in China Merchants Bank’s employee expenses.

In the first half of 2021, the average monthly salary of China Merchants Bank employees once reached 58,000 yuan. This means that the current average monthly salary of employees is 6,000 yuan less than three years ago.

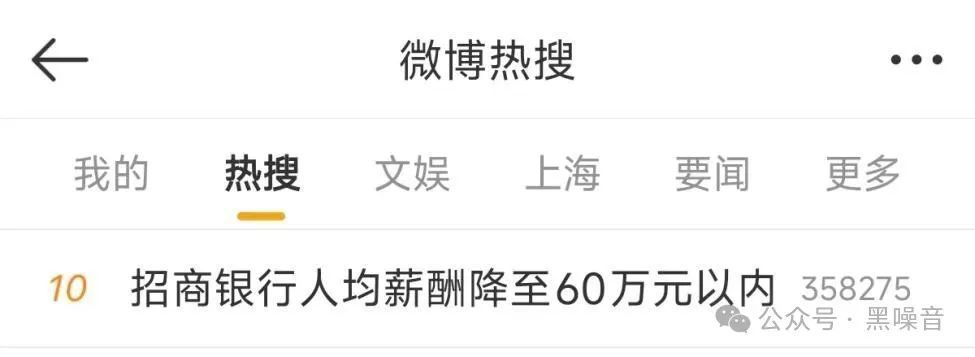

Soon, the topic #ChinaMerchantsBank’sAverageSalaryDropsBelow600,000Yuan# topped the Weibo trending list, sparking heated discussions among netizens.

At first glance, the first reaction is “Bank salaries are really high”, but in fact, this salary is just an average, the result after averaging executives and employees. In fact, the salary of ordinary employees of China Merchants Bank is not much different from that of ordinary people.

The vast majority of netizens have actually missed the point. The point is not how high the salary is, but what the salary cut at the bank means, especially what the salary cut at China Merchants Bank means. It can be said that the signals of systemic financial risks have already emerged. At this time, we must be extremely careful, otherwise, the entire financial system may be in turmoil in the future.

China Merchants Bank has a very special position in China – it is the real bellwether of China’s banking industry.

Why do you say that? Because China Merchants Bank is the best commercial bank in China in terms of service, and it has been the best retail bank in China for many years. Of course, its scale is also the largest among joint-stock commercial banks.

It can be said that in China’s banking industry, apart from the state-owned Industrial and Commercial Bank of China, Agricultural Bank of China, Bank of China, and China Construction Bank, you have to look at China Merchants Bank. In the 2024 banking rankings, China Merchants Bank ranks only after the four major banks, which shows its scale and status. As a joint-stock bank, it is not easy to achieve this level.

For this reason, the large-scale salary cut at China Merchants Bank is like a bomb. It seems a bit gossipy to be on the trending list, but the reality behind it is dangerous and heavy.

The real problem is not actually the salary cut, but the financial report of China Merchants Bank.

As mentioned earlier, China Merchants Bank is the best retail bank in China, which means that China Merchants Bank mainly reflects the advantages of its personal business. However, the 2024 financial report is not very good:

China Merchants Bank’s retail financial business had a pre-tax profit of 90.644 billion yuan in 2024, a year-on-year decrease of 9.28%. The main sources of revenue, net interest income and net fee and commission income, both decreased year-on-year.

Net interest income decreased by 1.58% year-on-year, and net fee and commission income decreased by 14.28% year-on-year.

Wealth management fee and commission income was 22.005 billion yuan, a year-on-year decrease of 22.70%.

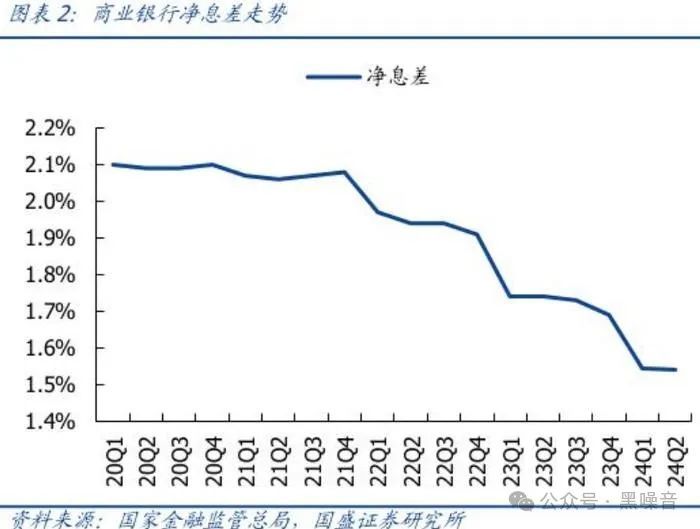

The net interest margin decreased from 2.15% in 2023 to 1.98%, and net interest income decreased by about 1.58% year-on-year. The net interest spread decreased from 2.03% to 1.86%.

Among these data, the most worrying is the last item, “net interest margin has fallen below 2%.” It can be said that this is a landmark event. Because the net interest margin is the lifeline of Chinese banks, and there is a clear warning line of 1.8%.

Net interest margin refers to the ratio of net interest income to average interest-earning assets. As of the third quarter of last year, 30 A-share listed banks were below the “warning line” of 1.8%.

Below the warning line indicates that the bank’s capital and cash flow may be at risk, and the balance sheet may have problems, so you need to be extra careful.

In the case that the net interest margins of Chinese commercial banks have fallen below the warning line, China Merchants Bank and Ping An Bank, these two “good students” were once the last to hold on, but now their net interest margins have both fallen below 2%, and are also heading towards the warning line.

From the overall performance, the growth rate of China Merchants Bank’s net profit attributable to the parent company is at least the lowest in 12 years, down 5 percentage points from the previous year’s 6.22%.

Despite this, China Merchants Bank’s financial report is still one of the best among all banks… Therefore, the salary cut this time is behind the problem of a sharp decline in the profitability of China’s banking industry, and it is a sign that the balance sheet of the banking industry may be at risk.

In the high-level economic work conferences of the past two years, preventing systemic financial risks has been a major topic.

The salary cut at China Merchants Bank is not a simple cost control, but a reflection of the overall pressure in the industry. With the instability of the financial market, banks have to cut expenses to cope with the weakening of profit growth, especially against the backdrop of the domestic economic slowdown and rising debt risks, banks have to “save their lives” by reducing salary expenses.

China’s banking industry is not healthy enough, with problems such as a single profit model, and has long had the operating model of “not paying attention to financial services but relying on loan growth”. In the past, when the economy was good, some economists warned that this income structure was unsustainable.

The reason is simple: if banks only rely on interest to survive, they will face great risks in the economic cycle fluctuations. This is also why the problems of China Merchants Bank are more eye-catching – China Merchants Bank’s profit structure is already the healthiest, but it is still difficult to escape the overall decline of the banking industry.

After experiencing the real estate downturn in the past three or four years, the banking industry has been hit the hardest. Coupled with the sluggish consumption and weak private investment, it has led to banks that rely on loan business being generally in a deep-seated operational crisis, or even a liquidity crisis.

What is even more worrying is that the non-performing loan ratio of banks is also generally rising.

In addition, the “business capital” of the four major banks, that is, the capital adequacy ratio, decreased in 2023. This is why the central bank is constantly lowering the reserve requirement ratio to reduce the operating costs of banks.

In general, in a period of economic downturn, “Under the nest, are there any intact eggs?”. At this time, no one is having a good time, and as the “headquarters” of economic liquidity, banks will inevitably face the greatest pressure.

But the problem is that in this situation, consumer loans have been vigorously promoted recently, forming a new round of leverage for the resident sector, in order to “activate funds” and deal with the urgent needs. Although this method can temporarily alleviate the liquidity crisis in the market, it is also a “time bomb”, and no one can predict when it will explode.

The biggest hidden worries of all economic problems are hidden in the banking industry and ultimately ignited in the banking industry. Only when the economy itself begins to recover can the crisis signals be truly resolved.

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.