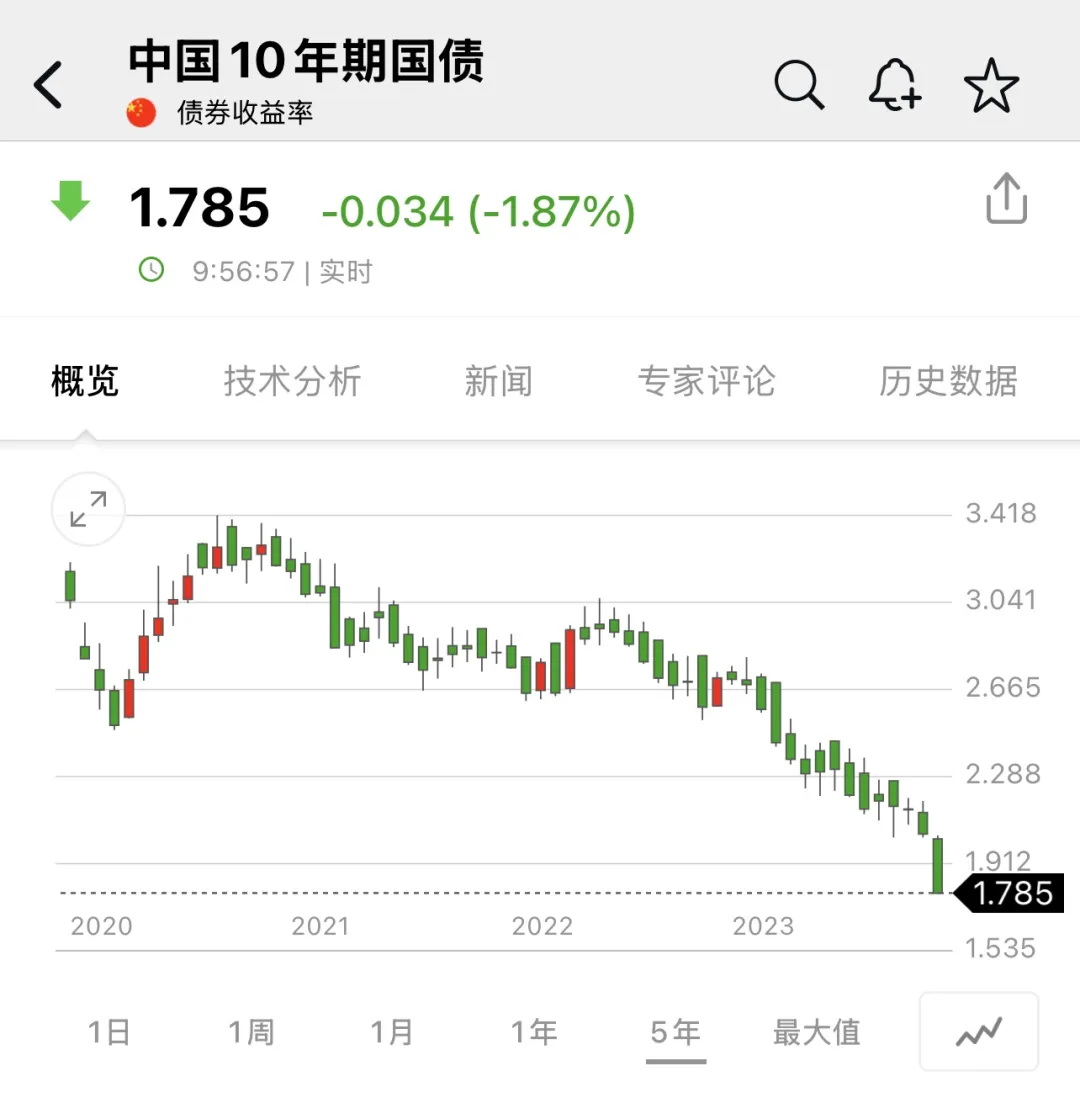

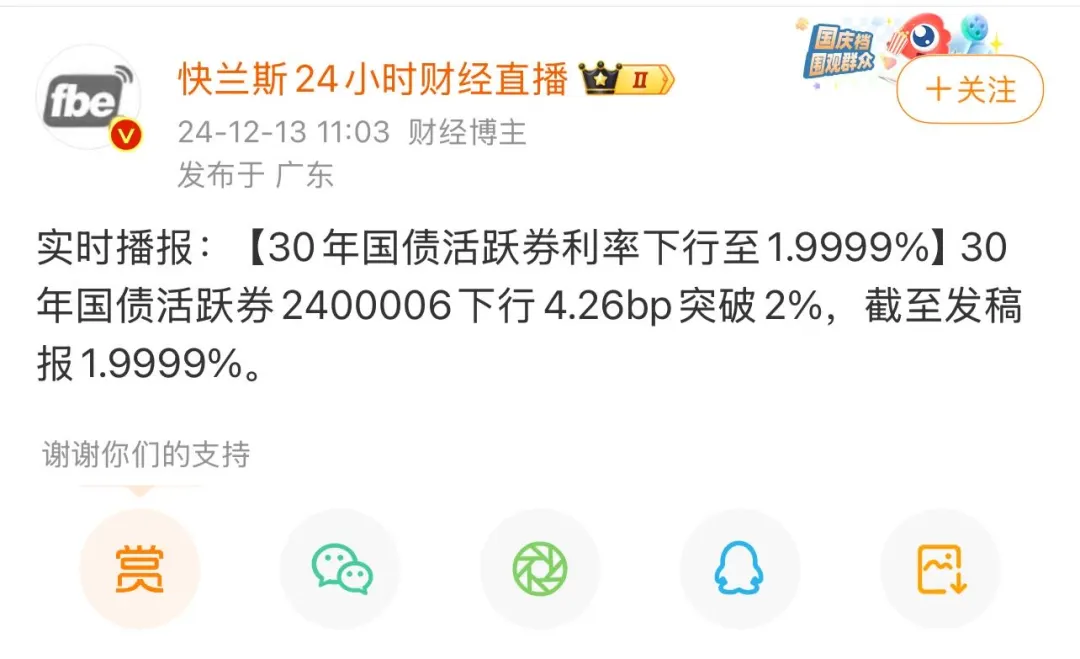

Following the inversion of the 30-year treasury yield between China and Japan (China-Japan reversal? What do low interest rates mean), the interest rates of Chinese government bonds of various maturities are still continuously declining.

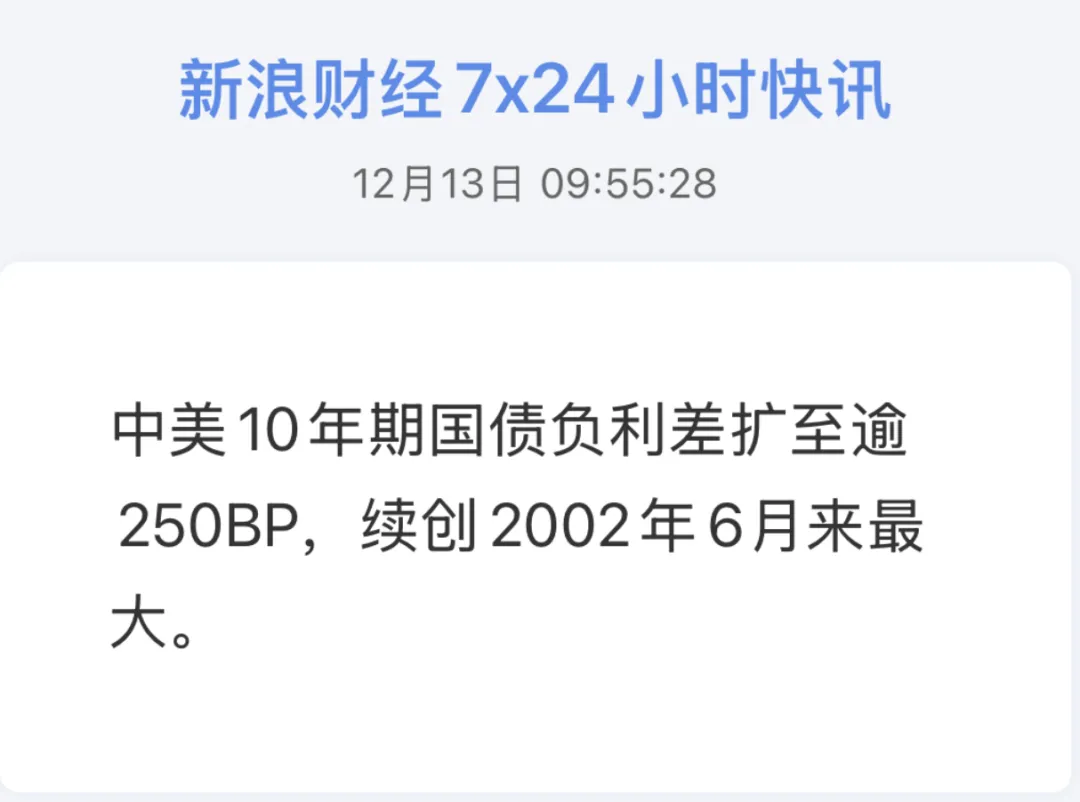

As of December 13, 2024, the yield on 10-year treasury bonds has entered the 1.7% range, the yield on 30-year treasury bonds has fallen below 2.0%, and the spread between the yields on 10-year treasury bonds in China and the United States has also hit a record.

Many friends who have just started paying attention to treasury bond yields may not know that in the past, China’s economic growth and inflation were long higher than the United States, and interest rates were long higher than the United States. The interest rate on 10-year treasury bonds was also higher than that of the United States for most of the past time. This kind of inversion is a minority, and the inversion of more than 250BP (2.5 percentage points) has created history.

Due to the decline in treasury bond yields, the net value of treasury bonds has risen sharply, and the ETF of 30-year treasury bonds in the market has risen nearly 20% in the past year.

Why are treasury bond yields continuously declining? The logic behind it has been explained in great detail in the past two topics, and we will review it now.

The blue part below is the previous theme on March 27, 2024 (Updated version) Has the housing price bottomed out? Part of the content ↓

It will definitely be easier to buy a house in the future, and interest rates will also continue to decline.

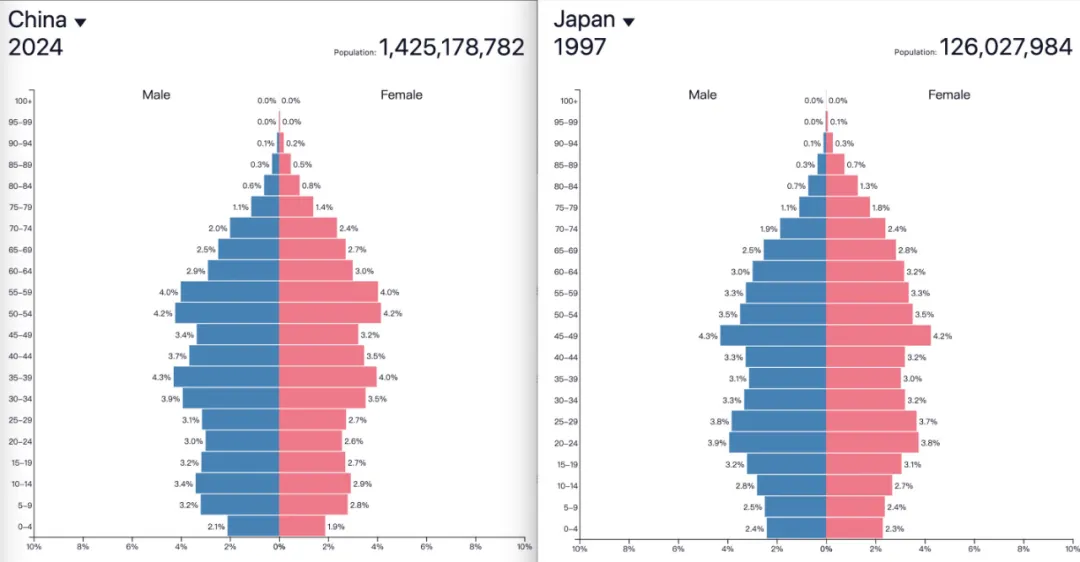

China’s population structure in 2024 is very similar to that of Japan in 1997. Coincidentally, the yield on 10-year Japanese government bonds in 1997 and the yield on 10-year Chinese government bonds today are almost the same, both at 2.3%.

China’s 2024 population structure (left) compared to Japan’s 1997 population structure (right)

This shows that the decline in interest rates is not only to save the property market, but also a necessary option to cope with the decline in demand and prices under the aging population. In the foreseeable future, the RMB interest rate will continue to decline. The current yield on 10-year treasury bonds is 2.3%. We will see it within 2.0% soon. If there are no black swan events, it will be reduced to about 1% in 10 years. So it will definitely be easier for people to buy a house in the future, because not only have house prices fallen, but mortgage interest rates have also fallen.

Referring to the performance of Japanese government bonds after 1997, there is still a lot of room for the decline in Chinese government bond yields (or the growth of net value). Chinese government bonds are now considered to be a very few RMB assets that still have investment value. Its credit risk is zero, absolutely safe, can preserve capital and earn interest and appreciate, and has good liquidity and can be cashed out at any time… Although the central bank does not want the market to form such a consistent expectation, and occasionally comes to teach investors a lesson and raise the yield on treasury bonds, any human intervention is difficult to stop the evolution of the general trend.

Later, in August 2024, the yield on treasury bonds did indeed continue to decline, leading to a sharp rise in the net value of treasury bonds, and the market was very hot, but suddenly, industry insiders threatened this phenomenon at the time, they said: the rush to buy treasury bonds is also a “shorting” of the economy.

The blue part below is the previous theme on August 13, 2024: When will the housing price bottom out? See the phenomenon from the essence

Part of the content ↓

The popularity of Chinese treasury bonds is rising, and then it is exchanged for a sentence: buying treasury bonds is also a “shorting” of the economy.

Why are people rushing to buy treasury bonds?

Here, we need to popularize the logic of bond appreciation. Most people’s understanding of bonds is that it is just a fixed-income asset, that is, we buy a bond and receive the principal and interest at maturity according to the interest rate, but the real bond market is not like this.

Because bond prices fluctuate every day with trading, for example, a 10-year treasury bond product has a face value of 100 yuan, and the determined coupon rate at the time of issuance is 3.5%. If the trading price of the product in the treasury bond trading market falls to 90 yuan, then the holder who buys the treasury bond will not receive 3.5% of the annual income, but 3.5÷90×100%=3.89%… It is easy to understand that the rise in market interest rates corresponds to the central bank’s interest rate hike, the rise in treasury bond yields, and the fall in treasury bond prices.

So why is it clear to rush to buy treasury bonds? It is because market participants have become increasingly clear about the direction of future interest rate changes: China’s risk-free interest rate is likely to continue to decline in the next ten years or even longer. The background of the decline in interest rates is the long-term decline in demand and inflation caused by the population structure.

China and Japan are surprisingly similar in population structure and interest rate trends. China’s population structure in 2024 is almost no different from that of Japan in 1997; correspondingly, China’s 10-year treasury bond yield in 2024 is also the same as that of Japan’s 10-year treasury bond yield in 1997 (2.1-2.3%).

Reviewing the content of the past period, now looking at the yield on China’s 10-year treasury bonds entering 1.7%, and the yield on 30-year treasury bonds falling below 2.0%, there is nothing particularly surprising except that the progress is a little faster. Looking ahead, a rate of 1% or even close to 0 is not impossible.

The impact of the continuous decline in treasury bond yields is two-sided.

From a good perspective, it is conducive to reducing the financing costs of the whole society, increasing the space for future national borrowing and using it to support people’s livelihood (as in Japan in the past two or three decades), and at the same time, under the background of declining interest rates, China’s export competitiveness remains strong, the purchasing power of the RMB remains strong, and under the steady advancement of financial opening (especially the convertibility of capital accounts), low-interest RMB is expected to go to the world through the channel of financing currency like the yen, and even make Chinese treasury bonds become new reliable international safe-haven assets;

From a bad perspective, the decline in interest rates is the result, not the cause. It is precisely because there are no other reliable investments that funds pour into risk-free treasury bonds, which shows that whether it is industrial operation or other major investments, it is really becoming more and more difficult to make money.

According to the “Golden Rule” of interest rates: a country’s real interest rate (r) after excluding inflation should be equal to the actual economic growth rate (g), “r=g” is an economic stable state that can maximize per capita consumption and social welfare.

The left side of the equation is the real interest rate (r), and the right side represents the actual economic growth rate (g). If inflation is added to both sides of the equation, then in the long run, the long-term nominal interest rate of an economy should be equivalent to the nominal economic growth rate.

In other words, treasury bonds are representative indicators of interest rates, and the decline in interest rates means a decline in the nominal GDP growth rate, and the decline in nominal growth means low inflation and low growth. Are you ready for this new normal?

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.