Text | Da He

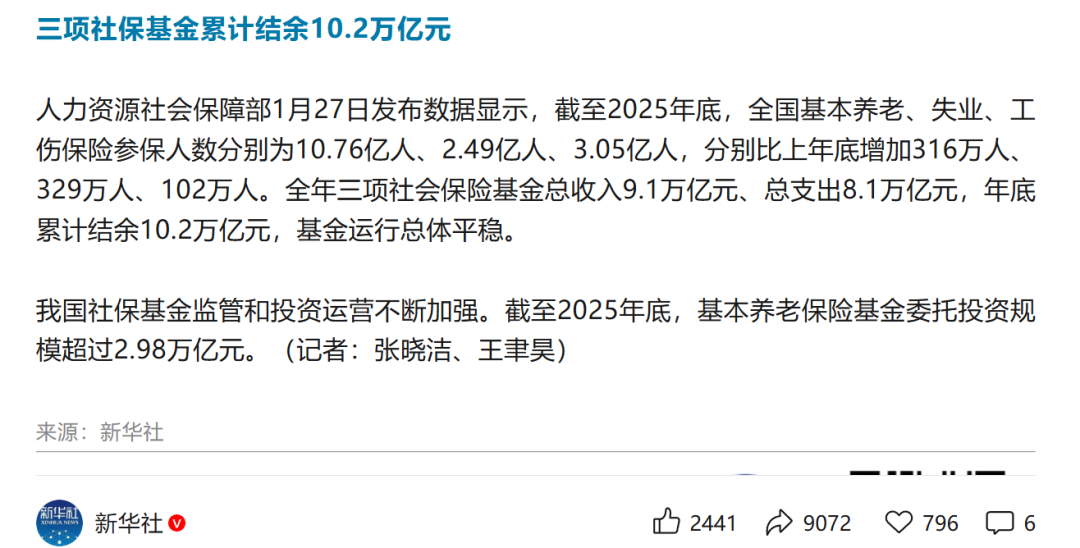

The Ministry of Human Resources and Social Security today released the social security fund data as of the end of 2025.

As of the end of 2025, the number of people participating in the national basic old-age insurance, unemployment insurance, and work-related injury insurance were 1.076 billion, 249 million, and 305 million respectively, an increase of 3.16 million, 3.29 million, and 1.02 million respectively compared to the end of the previous year.

The total income of the three social insurance funds for the whole year was 9.1 trillion yuan, the total expenditure was 8.1 trillion yuan, and the cumulative surplus at the end of the year was 10.2 trillion yuan, and the fund operation was generally stable.

Compared with the official bulletins of previous years, the annual surplus of the three social insurance funds has exceeded the 10 trillion yuan mark for the first time, and the total income, total expenditure, and cumulative surplus have all reached a record high since the open data was available.

However, a high surplus does not mean that we can rest easy, and we still need to view it cautiously.

First, a semi-public secret is that the real income and expenditure level of the social security fund is a state of deficit, and the only reason for the growth of the social security fund balance is the large-scale subsidies from the finance.

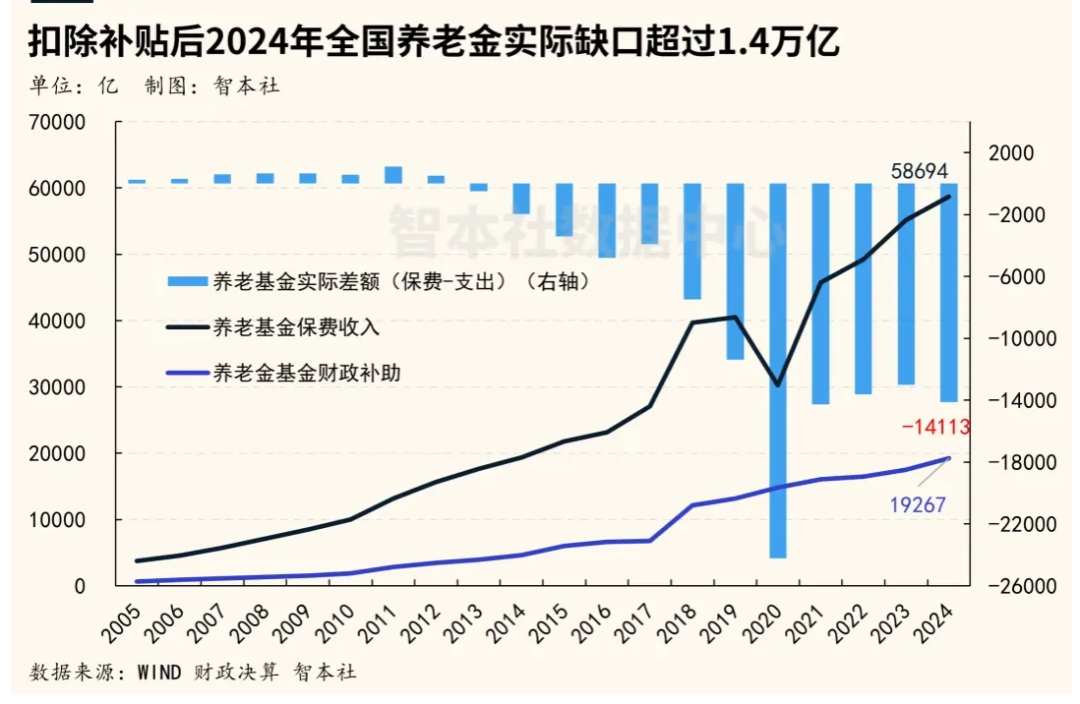

The data for 2025 has not yet been released. Taking 2024 as an example, the total income of the national basic old-age insurance fund was 8.19 trillion yuan, the total expenditure was 7.28 trillion yuan, and the book surplus was 0.81 trillion yuan.

However, this apparent surplus includes 1.93 trillion yuan in financial subsidies, accounting for 23.6% of the total income.

In fact, as we can see from the picture above, if we only consider the pure payment situation, then from 2013, the basic old-age insurance fund has been in a state of insufficient income.

If there were no subsidies from the finance for basic old-age insurance, the gap in the basic old-age insurance fund in 2024 would have reached 1.12 trillion yuan.

But according to the current trend, the data for 2025 will definitely be even higher than that of 2024.

From another perspective, the burden of financial subsidies is becoming heavier and heavier.

From 134.1 billion yuan in 2008 to 1.93 trillion yuan in 2024, it has increased by nearly 15 times in sixteen years, and its growth rate far exceeds the growth rate of public budget revenue in the same period.

This is obviously not a sustainable model, and financial subsidies will reach a limit sooner or later.

However, this is just the beginning.

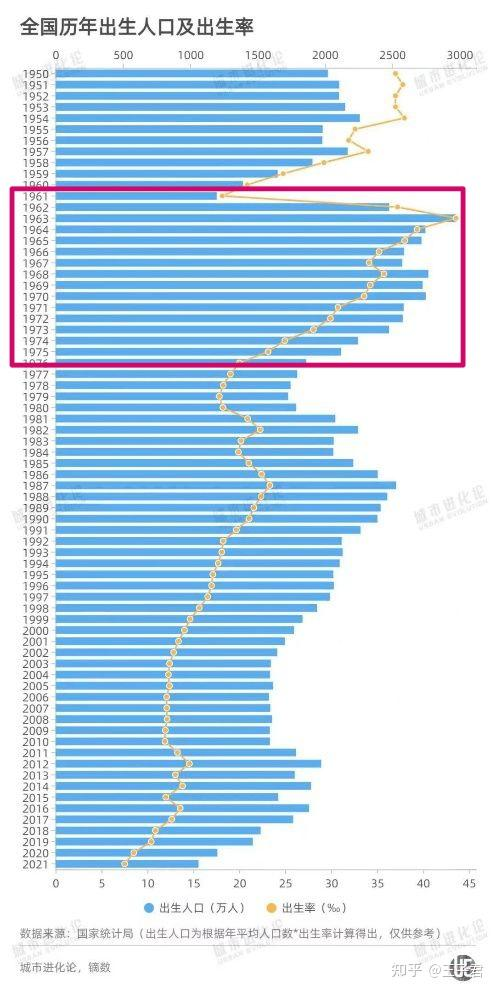

From the perspective of population structure, in the next ten years, the number of new retirees in China will be in the millions every year.

In 1962, the birth population in our country was 24.64 million, and it was 21.08 million until 1975. This is the first wave of the big Chinese baby boom;

The peak of fertility after 1962 means that if we retire at the age of 60 (average of men and women), it means that from 2022, there will be more than 20 million people retiring every year, while the number of people who die (withdraw from retirement) every year is about 10 million.

Of course, this aging acceleration is actually the highest in the next 10 years, and it will slowly decrease in the future,

It’s not because fewer people retire, but because more people die. When the negative population growth reaches its peak, the acceleration of aging will also peak.

But don’t think that it will be okay when the acceleration peaks, which means we have reached the plateau of super aging.

It can still be supported at present, because a large part of the 20 million retirees only receive a few hundred yuan per month. When these people withdraw, the pressure will be directly full.

Look at Japan for this.

As a “pioneer” in aging and low fertility, Japan’s pension system has long been deeply bound to the national finance, and a considerable part of the newly issued national debt each year must be used to fill the gap in pensions.

This rigid expenditure, like a huge black hole, continuously squeezes the government’s investment in education, scientific and technological innovation, and industrial upgrading.

Back then (1995), Japan could still casually throw out an economic stimulus plan of 14 trillion yen, and its social security expenditure accounted for only 16%.

But now, the proportion of social security expenditure has long exceeded 30%, while the budget for investing in the future semiconductors, AI, new energy and other fields seems to be stretched.

Coincidentally, in that year, the proportion of Japan’s population aged 65 and over was 14% (deep aging), and in 2025, this number has reached 15.9%.

Aging is like a silent and hard wall, slowly moving towards us.

Therefore, from the perspective of preparing for a rainy day, the current idea is to try to increase income and reduce expenditure.

In terms of reducing expenditure, there is no need to say more about delaying retirement, everyone understands.

I originally wanted to say whether we could cut the pension for government agencies, after all, you spend 640 billion yuan to support 20 million people, and the 420 billion yuan for urban and rural residents’ pensions supports 180 million people.

But recently, the priority is to protect the system, so it is estimated that this is difficult to cut.

Against the backdrop of a declining population base and the financial subsidies approaching the limit, “increasing income” has almost become the only direction.

The most direct “source” is naturally the current social security payment group.

So it can be predicted that: no matter how much you scold, the social security payment standards are estimated to continue to increase.

But this is estimated to stimulate non-compliance with social security in the opposite direction, because the base is rising and enterprises also have to pay more.

When the labor costs of enterprises increase due to the increase in the social security base, they will naturally seek ways to avoid it.

According to last year’s social security white paper, less than 30% of enterprises fully comply with social security payments.

More small and medium-sized enterprises may turn to flexible employment and labor dispatch in order to survive, making a complete labor relationship the “privilege” of a few large enterprises.

This will undoubtedly exacerbate the differentiation and instability of the employment market and damage the long-term protection of workers.

This may eventually lead to a fundamental understanding:

The cost of an aging society is far from being solved by simply increasing the collection from current workers.

This generation has been overwhelmed by the high cost of housing, education, and childcare, and their future has long been severely overdrawn.

The predicament we face today is essentially the price we must pay for the past few decades of accelerating industrialization and exchanging the demographic dividend for an economic miracle.

People will not stop and really sit down and think of ways until this wall hits them hard.

The so-called consensus is often exchanged with painful costs.

Before the policy is willing to take over the social security costs, we still have to suffer a little more.

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.