This is a public statement made some time ago by economist Mao Zhenhua. He said that current pensions are too high, even higher than salaries for those still working. He mentioned that elementary school teachers in his hometown in the countryside earn over 4,000 yuan a month while working, but can receive 8,000 to 9,000 yuan after retirement. “The retirement system should guarantee people’s basic living standards, not an elegant life.” This statement sparked a lot of discussion, with many people leaving comments about similar cases they knew, which were quite common.

However, it should be noted that not all elderly people are so fortunate. Therefore, those who are truly happy are those within the system, excluding the vast majority of farmers and most enterprise employees. “Within the system” here includes state-owned enterprises. Although state-owned enterprises do not belong to administrative institutions, they are still within the broad sense of “within the system.” The phrase “entering the system” actually includes entering state-owned enterprises, especially monopolistic state-owned enterprises like tobacco and electricity.

Let’s watch a video:

The blogger said: His neighbor retired from the Tobacco Bureau and receives a pension of 14,200 yuan, a living allowance of over 1,000 yuan, an annuity of over 2,000 yuan, and a year-end bonus, receiving nearly 19,000 yuan in total. He also calculated that this person requires 30 young people to pay social security to support him. He is likely to live to 90 years old and can receive benefits for 30 years, totaling 6.84 million yuan. Finally, he raised a question: This elderly person has 29 million peers, and this year there are 9 million newborns, less than one-third of the previous year. In 22 years, these newborns will have to pay social security. What do you think the future will be like?

This video has received over 100,000 likes and over 7,000 comments on Douyin. Many people have left comments about how good the treatment is for those who have retired from state-owned enterprises. His specific wording may be debatable, such as whether 30 young people are needed, whether he can live to 90 years old, and that the truly burdened among the 29 million elderly people are about 10% of the retirees within the system. However, in general, what he said is largely correct, and the problem is a real one.

Over the past year, such online hot topics have emerged one after another, appearing in various forms. I previously summarized them briefly:

The excessively high retirement income has become a social hot topic every now and then: scenarios include “my social security is dancing on the way home from overtime,” individual cases include “my grandfather can bring in 566 yuan of income for the family for every extra day he lives,” phenomena include “the elderly are becoming the biggest spenders in Shanghai’s shopping malls,” and the overall situation is “China is full of vibrant elderly people, while young people are lifeless and middle-aged people are despondent.”

Peng Yuanwen, Public Account: Past Events and Thoughts You can indeed receive a pension without paying—On the nine reasons why China should implement a universal pension

All the problems point to one thing: pensions within the system can no longer continue to rise like this!

The starting point of the current pension system is to divide people into different classes based on whether they are inside or outside the system and between urban and rural areas. The endpoint is a gap of several times, ten times, or even dozens of times. I have talked about this many times in the past, and this article will discuss the adjustment mechanism in the middle.

In October 2024, the ten-year transition period for the pension integration reform will end. Although the system of institutions and enterprises has nominally been unified, the result is a complete failure: the purpose of the reform was to narrow the gap in treatment between those inside and outside the system, but now it is even more disparate than ten years ago.

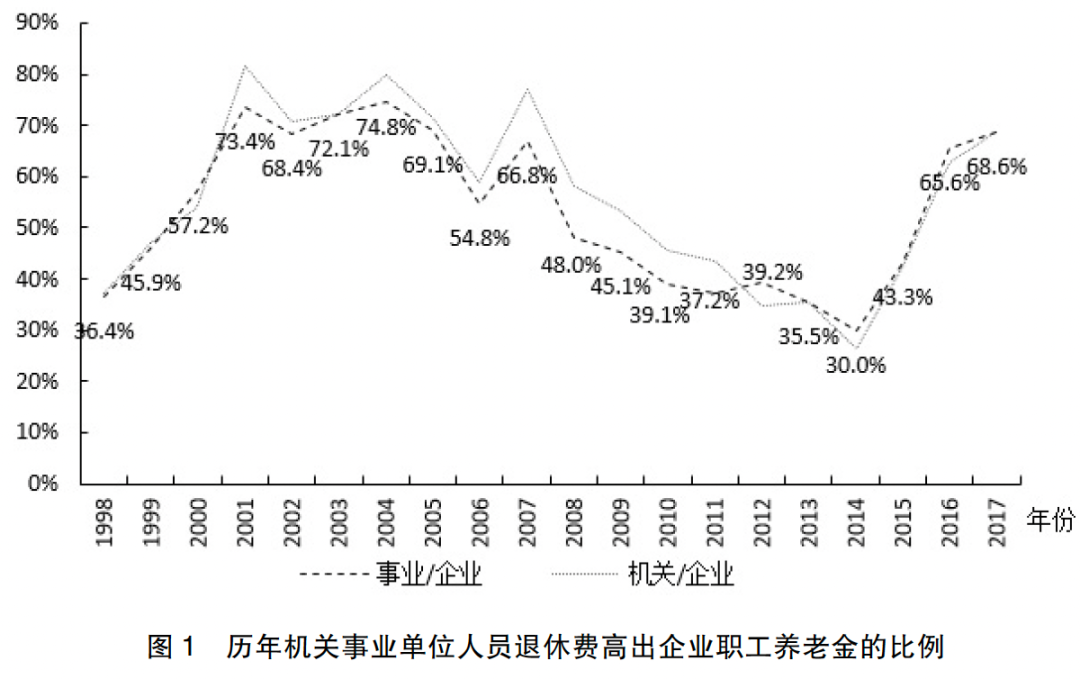

This chart comes from a 2021 paper titled “Will the Pension Insurance Reform for Institutions and Enterprises Bring New Pension Gaps?” It shows that when the pension integration reform began in 2014, the gap in pensions between administrative institutions and enterprises had already dropped to a low point of 30%. However, after the reform, it quickly rose to nearly 70% in just three years. The article statistics up to 2017, and now, the gap has further widened to double.

In my article “Five Common Sense of China’s Pension System,” I have reviewed the pension growth of different groups over the years, from 2009 to 2023:

The monthly pension within the system increased from over 2,000 yuan to over 6,000 yuan, an increase of about 4,000 yuan, with an annual increase of about 285 yuan.

The monthly pension of enterprise employees increased from over 1,000 yuan to over 3,000 yuan, an increase of about 2,000 yuan, with an annual increase of about 140 yuan.

The monthly basic pension for urban and rural residents (farmers) increased from 55 yuan to 223 yuan, an increase of 168 yuan, with an annual increase of 12 yuan (more than half of the provinces are below 150 yuan, with an annual increase of about 6 yuan)

The rate of pension growth within the system is so large that it inevitably leads to more and more financial subsidies. According to the “2023 National General Public Budget Expenditure Final Accounts Table,” the per capita pension financial subsidy for retirees within the system exceeds 3,000 yuan/month, which is 18 times that of farmers.

This is the most frequently cited report, and on September 4, the Ministry of Finance released the data for 2024. As expected, the funding gap has further increased.

In the “2024 National General Public Budget Expenditure Final Accounts Table,” “Expenditure on pensions for administrative institutions” is 1,588.32 billion yuan, which exceeds the budget by 72.813 billion yuan, of which “subsidies to the basic pension insurance fund for institutions” is 643.919 billion yuan, an increase of 77.346 billion yuan compared to 2023.

What is the concept? In 2024, the pension for farmers increased by the highest amount in history, 20 yuan/month, and 180 million people would only get 43.2 billion yuan a year, while 22 million retirees within the system quietly increased by 77.346 billion yuan, and the per capita financial subsidy increase is 14 times that of farmers.

It’s not much better for enterprise employees. In 2024, enterprise employees and urban and rural residents were subsidized a total of 1,239.647 billion yuan. 180 million urban and rural residents (farmers) plus 120 million enterprise employees, the number is 13.6 times that of those within the system, and the financial subsidy only increased by 33%. The total expenditure on pensions for administrative institutions is 1,588.32 billion yuan, minus the subsidy of 656.375 billion yuan for employees within the system, the remaining 931.945 billion yuan is basically subsidies for retirees within the system.

It is worth mentioning that: Although the financial subsidy within the system in 2024 exceeded the budget by 72.813 billion yuan, the subsidy for enterprise employees and urban and rural residents (farmers) was 29.202 billion yuan less than the budget, and the actual overspending was only 43.611 billion yuan, which is still very economical.

The report ends here. For specific data, you can search for “National General Public Budget Expenditure Final Accounts Table” on the website of the Ministry of Finance and look at item eight.

Back to the point, there are many reasons for this. Simply put, it is a problem caused by proportional growth: the larger the base, the more it increases, and the gap naturally becomes larger. How big is the gap after ten years if the pension is 10,000 and 2,000, and both increase by 5% each year? This is the magic power of “compound interest.”

And from the details of the system design, it basically follows the principle of “everything is beneficial to those within the system.” For example, for “older people,” if they get more according to the old method, they will follow the old method; if they get more according to the new calculation method, they will follow the new method. This is the most direct “beneficial principle.”

There are also more complex ones, such as the new pension calculation method, which is “better” than before. According to the calculations in the article “Will the Pension Insurance Reform for Institutions and Enterprises Bring New Pension Gaps?”, the original text is quoted as follows:

“Before the pension integration reform, … staff members of institutions and enterprises did not need to pay social insurance premiums during their employment, and pensions came from financial subsidies, with a replacement rate between 75% and 90%. After the pension integration reform, when the statutory retirement age is 55 for women and 60 for men, the pension replacement rate for retirees of institutions and enterprises under different scenarios is between 76.2% and 110%. The lower limit is basically the same as the replacement rate of the original system, and the upper limit exceeds the original replacement rate, thus widening the gap in pension replacement rates between enterprise employees and staff members of institutions.”

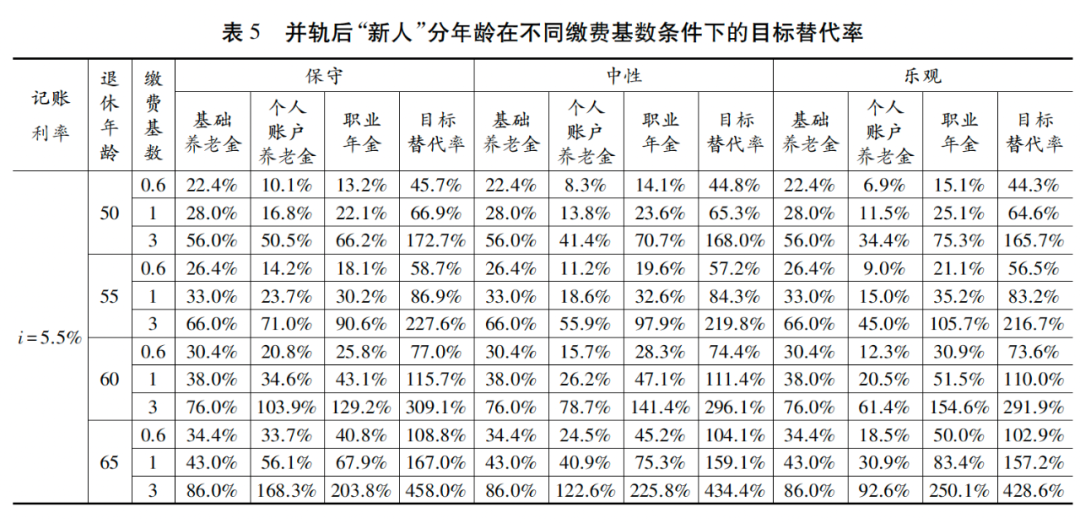

This is the calculation of the target replacement rate for “newcomers” of different ages under different contribution base conditions after the integration:

As shown in the figure, if you retire at 60, with a contribution base of 1, the replacement rate exceeds 110%; if you retire at 65, the replacement rate can even reach an astonishing 160% or so.

What is the concept again? The pension replacement rate worldwide is generally around 50%. The world-famous Nordic high-welfare countries are only 60%, and the particularly high ones like Denmark and Iceland are only about 80%. Therefore, China’s pension replacement rate within the system is “far ahead” and well-deserved.

The so-called “replacement rate” is the ratio of retirement income to salary while working. The average salary within the system is already higher than that of enterprise employees. With such a high replacement rate, it is naturally higher than most employees on the job after retirement. Speaking of this, do you understand how the pension is higher than the salary while working, as mentioned at the beginning?

I don’t need to say that this is abnormal, right? Why is the pension replacement rate in most countries around 50%? Because people who don’t work shouldn’t get more than those who do. There is an intergenerational fairness issue here, and we need to leave a way out for young people.

So I also want to say to young people: In the past, I have been talking about farmers, farmers, farmers. Don’t think this has nothing to do with you, don’t think you can hide within the system. The system cannot accommodate so many people, and even if you can hide in now, problems will arise sooner or later… An unfair system harms the majority, and there is only one solution, which is fairness, fairness, fairness.

What is fairness? In terms of the social security system, it must take on the function of “correcting deviations.”

“The way of man is to diminish what is lacking and supplement what is in excess, the way of heaven is to diminish what is in excess and supplement what is lacking.” This sentence, put into modern society, means that the social security system should make up for the deficiencies of free competition, and the system design must “rob the rich and give to the poor.”

There are various system designs in this regard. One method is through the “discriminatory” policy of universal pensions. For example, in Canada, the old-age security benefits that can be received without paying are set with an income threshold. If it is higher than a certain level, it should be reduced, and if it reaches a certain amount, it should be zeroed. Australia is even stricter. Universal pensions will conduct strict income tests and asset tests, and will also decrease or even zero based on higher income and assets. In this regard, it must not be “pay more, get more, pay less, get less, and not pay, get nothing.” The reason for this is detailed in my article “Why can’t pensions be “pay more, get more”?“.

As another example, even the United States, which emphasizes free competition the most, also has a similar design in its pension system, using a tiered progressive replacement rate to achieve the purpose of “robbing the rich and giving to the poor”: Simply put, take a person’s highest income over the past 35 years as a standardized wage level, multiply the replacement rate by 90% if it is below a certain level, 32% for the middle value, and only 15% for the replacement rate above a certain level—you can understand it by reversing the personal income tax threshold. I used ChatGPT to calculate that a pension replacement rate of $30,000 per year can reach 58%, with an investment return rate of 2.7 times; while a pension replacement rate of $150,000 per year is only 29%, with an investment return rate of 1.35 times. In other words, although wealthy people pay more pension insurance premiums, the actual pension they receive is not proportional. The ultimate result of the system design is: the higher the income, the lower the replacement rate, and the lower the income, the higher the replacement rate.

In contrast, our ultimate result here is: the highest replacement rate within the system (including state-owned enterprises) is the highest, reaching 80% to 100% or even higher; enterprise employees who create the most wealth but have average income have a replacement rate of 40% to 50%; farmers with the lowest income (average income is less than half of urban residents) have a replacement rate of only about 10%. So, what kind of system design will lead to such a result? Please think about it yourself.

Let’s study the “Social Insurance Law of the People’s Republic of China” together, focusing on the bolded text:

Chapter 1 General Provisions

Article 1 In order to regulate social insurance relations, protect the legitimate rights and interests of citizens to participate in social insurance and enjoy social insurance benefits, enable citizens to share the fruits of development, and promote social harmony and stability, this law is formulated in accordance with the Constitution.

Article 3 The social insurance system adheres to the principles of broad coverage, basic protection, multiple levels, and sustainability. The level of social insurance should be commensurate with the level of economic and social development.

Public Account: Chen Qi Social Security Center Full text of the Social Insurance Law of the People’s Republic of China

I think the legislative purpose of the Social Insurance Law is correct, but it has gone astray over the past ten years and should return to the right path. Raising the basic pension for farmers and implementing a universal pension system, not seeking to rob the rich and give to the poor, but seeking to distribute subsidies equally, is the most basic requirement and the right path.

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.