A Deep Dive into the Chinese Economy: A 6000-Character Analysis

The past two weeks can be said to be the most pessimistic two weeks since the pandemic.

Macroeconomically, various economic indicators have all plummeted. In terms of total retail sales of consumer goods, apart from a slight month-on-month increase in catering in April, all other industries have declined, some even with double-digit drops.

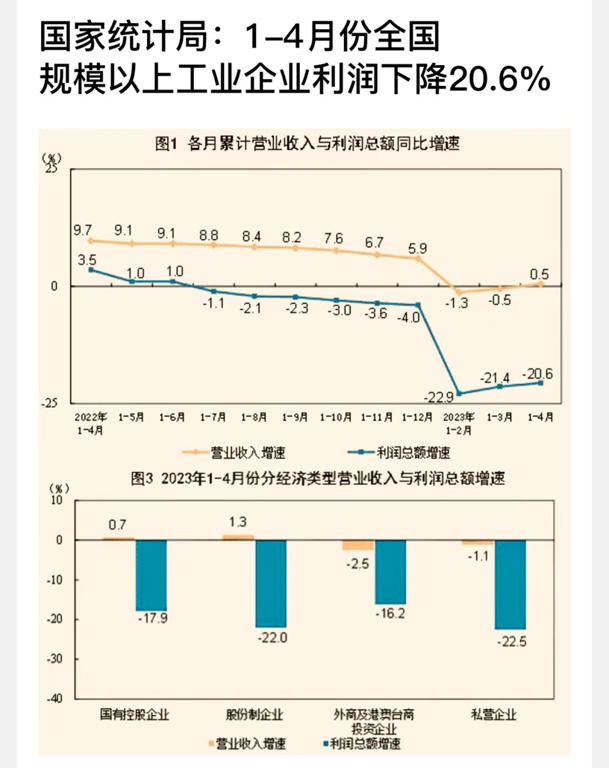

Regarding corporate profits, in the first four months, regardless of state-owned enterprises, private enterprises, or foreign enterprises, all continued to decline on the basis of last year’s low base, with private enterprises experiencing the largest drop, exceeding 20%.

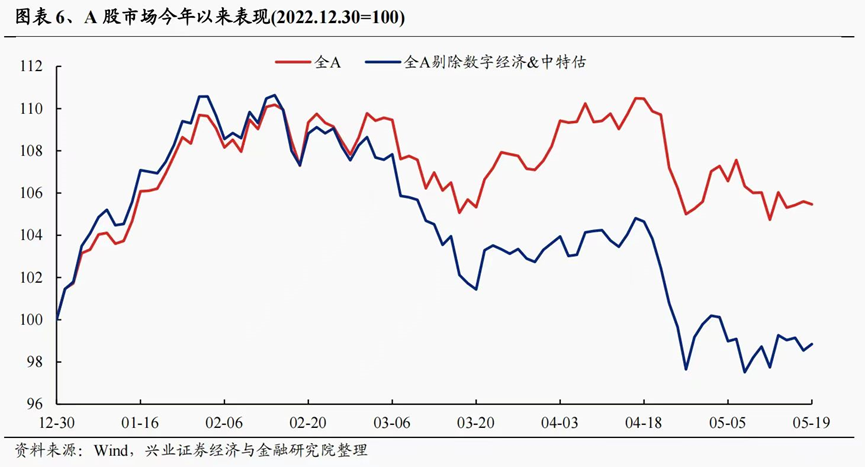

The stock market goes without saying. Since the beginning of the year, the Hang Seng Index has already shown negative returns, and the portion of A-shares excluding “China characteristics valuation” is basically also showing negative returns.

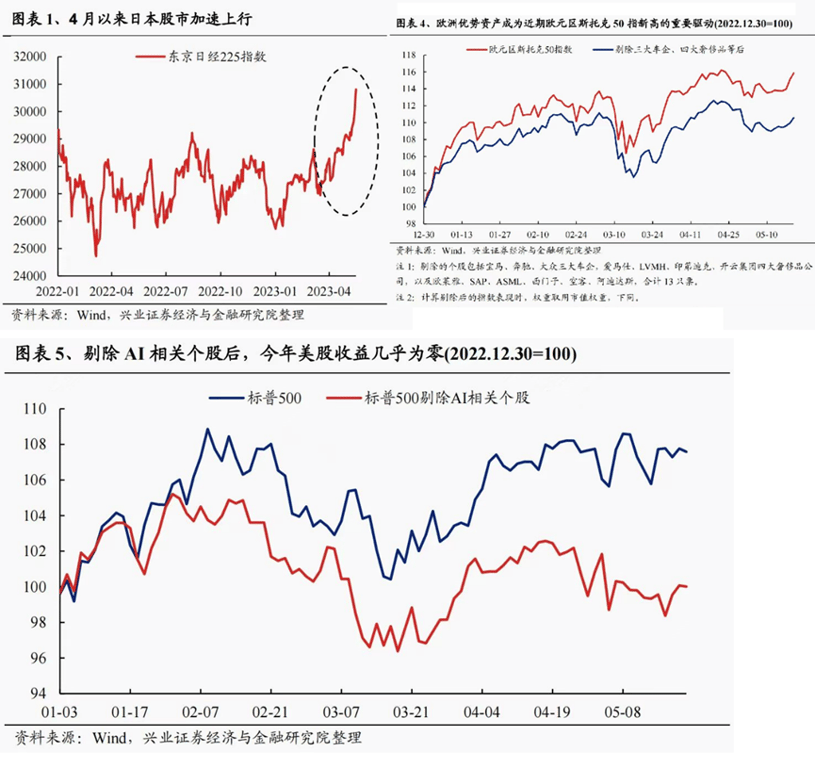

Meanwhile, the U.S. Nasdaq has risen nearly 30% this year, and European and Japanese stock markets have also hit new highs. Even in Turkey, where inflation is exploding, the stock market’s return after being priced in U.S. dollars far exceeds that of A-shares.

Microeconomically, major companies like Alibaba have laid off employees, a provincial capital’s city investment bond is on the verge of collapse, multiple housing projects have seen a cliff-like price drop and then been halted, and even the per capita consumption during the May Day holiday has decreased significantly.

The other day, I was jogging in the neighborhood and chatting with the guy selling roasted goods at the entrance. His daily sales used to be three or four thousand yuan, but now it’s less than 1,000 yuan. The supermarket next to his stall, which occupies over 1,000 square meters, used to have daily sales of fifty to sixty thousand yuan, but now it’s only seven or eight thousand yuan.

He complained that even the security guards in the neighborhood had been cut from 200 people at the peak to 50, and this is still a relatively high-end community in a first-tier city.

Frankly speaking, at the relatively optimistic time at the end of January, I considered the possibility of a market correction and took some risk-averse measures, but I didn’t expect that the change in sentiment would be so great just a few months later.

The most common explanation is: people used to think that the economy would improve after the pandemic, but now that the pandemic is over, they’ve found that not only has it not improved, but it’s even worse—the last hope is gone.

The Chinese economy is at a very critical crossroads.

Domestically, the long-term impact of deleveraging is still emerging, confidence in the post-pandemic era has not fully recovered, and the contraction of industries such as real estate and the internet will continue to bring downward pressure on the economy; externally, the Federal Reserve’s benchmark interest rate has hit a 20-year high, the US dollar is selling off Chinese assets, and emerging industries such as semiconductors are facing unprecedented sanctions from the United States.

This is a perfect storm.

And once a rapidly growing economy experiences a recession, there are basically two outcomes: one is to become like Japan, where young people collectively lie flat and the birth rate plummets; the other is to become like Brazil, where young people are collectively unemployed and the crime rate rises sharply. Regardless of the outcome, the economy will stagnate for at least 20 years. As mentioned in previous articles, the birth rate issue is actually within our expectations and is an acceptable range. But the safety issue is definitely not within the bottom line we can accept. And the news in recent months clearly makes us feel that there are more violent crimes and more safety accidents, which is no longer just an economic problem, but a matter of long-term stability.

If saying that protecting the economy has always been a must-do rather than an option, then what I want to say today is: not only must we protect the economy, but it is now time to protect the economy at all costs.

Why say “at all costs”? Because any option comes with a cost.

In 2008, we used “four trillion” to protect the economy, and the cost was the subsequent real estate finance and local debt predicament; in 2020, we protected the people’s lives and health, and the cost was that the opening up was later than most countries in the world, and the recovery cycle of the service industry was prolonged. Of course, if we review it afterwards, our decision-makers are of course absolutely wise.

So, how should we protect the economy now? And what price do we need to pay?

Here, I want to divide it into three dimensions: protecting asset prices, protecting growth, and protecting employment.

First, let’s talk about protecting asset prices, and the first thing here is housing prices.

Many people may have scoffed at high housing prices in previous years, but in the past two years, everyone has realized that the decline in housing prices has not made everyone live better, and has not even reduced the anxiety of young people in first-tier cities who cannot afford to buy a house—because even if housing prices have fallen by 30%, those who cannot afford to buy still cannot afford to buy, but with the economic downturn, most people’s incomes have decreased.

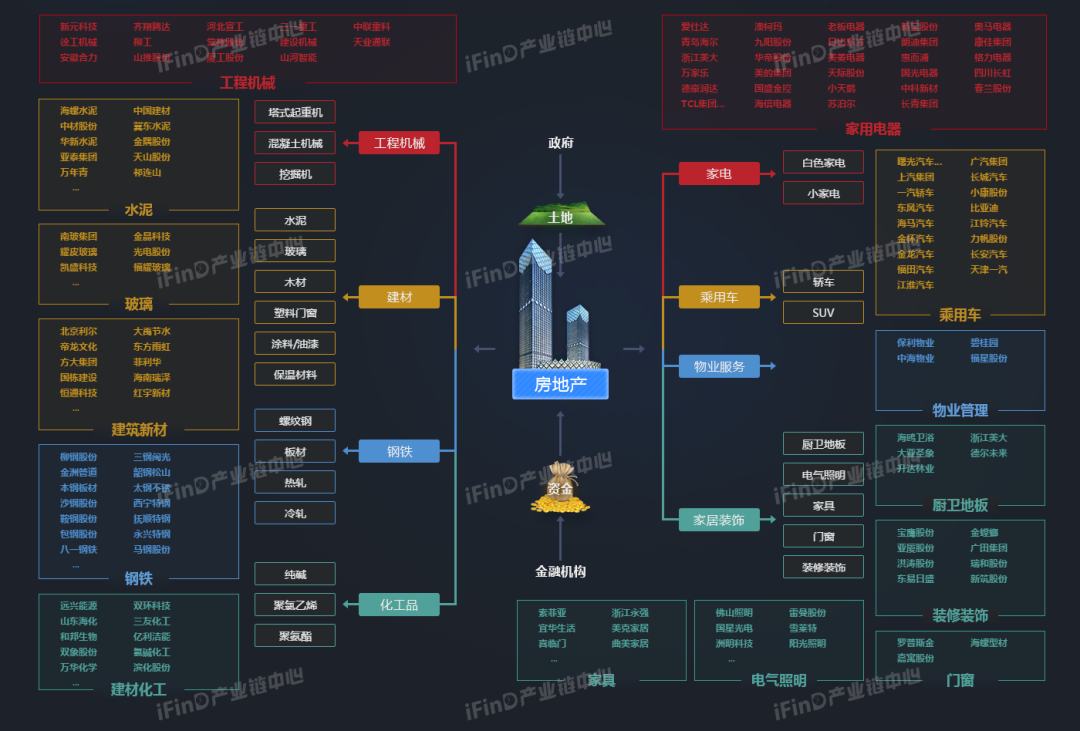

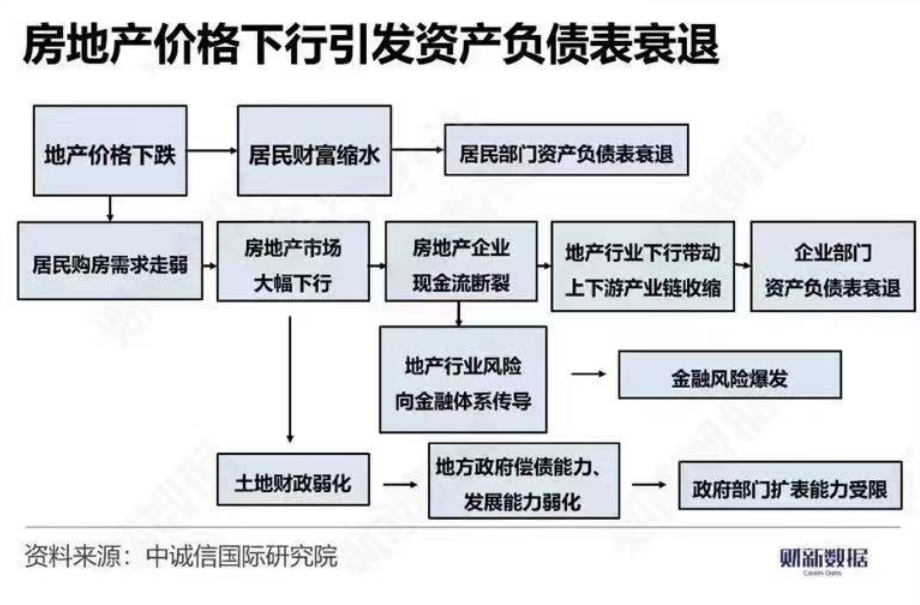

From the above diagram, we can see that real estate’s reputation as the “mother of cycles” is not for nothing. The upstream supports industries such as building materials and construction, and the downstream is closely linked to industries such as decoration and home appliances, and most importantly, it provides a continuous stream of cash flow for government finances.

Especially in China, real estate also has a special meaning as a general collateral for the banking system. We all know that the general collateral for the US banking system is US Treasury bonds, while real estate in China’s banking system plays the role of US Treasury bonds. Some time ago, the decline in US Treasury bonds brought down a batch of small and medium-sized banks. At that time, there was a voice in China that was quite proud of the safety of our banking system. Little did they know that, compared to US Treasury bonds, which are backed by the credit of the US government, the theoretical space for the decline in domestic real estate prices is greater. Therefore, once prices continue to fall, the risk exposure of China’s banking system will far exceed that of the United States.

The government certainly knows the importance of real estate, so since last year, relevant departments have given some policies, including “guaranteeing the delivery of buildings” and lifting purchase restrictions, lowering interest rates, etc. In summary, the idea is “protecting prices, sacrificing volume”, trying to lift purchase restrictions and other means, hoping to form a new equilibrium as soon as possible on the basis of a low level of transactions, avoiding a “hard landing” of housing prices that leads to large-scale risks in the banking system, and at the same time, using price control measures to enhance the market competitiveness of new houses, ensuring developers’ willingness to acquire land and government financial revenue.

But what about the results? Obviously, it’s not optimistic.

The reason is simple: the price of new houses can be fixed by limiting the price of developers, but with the decline in the income of residents, especially the middle class, more and more people will choose to sell their houses to solve cash flow problems under the pressure of mortgage payments, and the price of second-hand houses is difficult to directly intervene.

I watched the video of the Chongqing couple selling their new house, which they had just bought two years ago, and losing their entire down payment the other day. To be honest, it’s painful to watch it once. But there’s nothing we can do. This is the reason why the number of second-hand houses listed in Beijing, Shanghai, and Guangzhou in April hit a record high—selling at a loss or waiting for mortgage defaults to be foreclosed. Weighing the two harms, we can only choose the lesser one.

But the decline in second-hand housing prices will lead to two more serious problems: first, in the face of the continuous decline in second-hand housing prices, more and more people will choose to sell at a loss or even default on their mortgages, and the bad debt risk of the banking system will only increase; second, because second-hand housing prices are constantly falling, the government, in order to make developers willing to buy land, can only sell land at a lower price, which not only reduces financial revenue, but also leads to an inverted price difference between new and second-hand houses, making second-hand houses even harder to sell.

And these two problems will only lead to a further decline in second-hand housing prices, forming a vicious cycle. Of course, the corresponding is that the price of new houses will fall synchronously, and developers’ investment willingness will further decrease or even continue to go bankrupt and close down on a large scale. The final result is to become the next Japan.

When the bottleneck lies in the ability and willingness to buy a house, rather than purely demand, any policy that starts from the demand side alone cannot solve the problem, and given the imminent degree of this risk, the window of policy adjustment is only a year or even half a year at most.

To be honest, it’s really tricky, and there are solutions, and the cost will be great.

First, significantly reduce the interest rates on deposits and loans.

What I’m talking about here is not the previous 0.1% reduction each time, but to reduce the five-year LPR to within 3% in one step, and of course, the deposit interest rate will also be lowered synchronously.

The core of monetary policy is to act quickly. Look at the trend of the Nikkei Index since the early 1990s. From 1991, interest rates were cut until the discount rate was as low as 0.5% in 1995, but the decline in asset prices never stopped during this period. Because once the trend is formed, confidence will not come back.

A successful case is the United States, which continuously and urgently cut interest rates during the pandemic and successfully protected the economy.

Second, on the basis of lowering the LPR, give existing and new mortgages a subsidy of about 1% per year for the next 3-5 years.

This subsidy is only a few billion yuan per year, and most banks bear it themselves, with a small part subsidized by the government. To put it more directly, it is to legalize the “mortgage loan to business loan” that many intermediaries are doing now, reducing transaction costs and rent-seeking space. For banks, although the interest rate spread has decreased, the bad debt rate has decreased, and the pressure to repay loans early has also decreased, the overall account is still calculated.

Third, after the first two steps are completed, the monthly mortgage payment for houses in first-tier cities is basically not much higher than the rent. On this basis, some new solutions can also be explored for some residents who have defaulted on their mortgages, such as changing the repayment of principal and interest to interest-only first, or turning the foreclosed house into a shared housing, where the part you paid for the down payment is still yours, and the ownership of the remaining part is transferred to the bank or AMC, and you pay them rent in proportion every year, and you can buy it back in the future if you have money. In addition, we also call on the government to introduce corresponding measures to protect the right to use the only housing under an individual’s name, even if you still owe the bank money after being foreclosed, you can still live there indefinitely, avoiding the situation of mass displacement.

On the basis of the above three points, there is also a fourth point, which is to restart the monetization of old housing renovation. There are still many old, broken, and small communities with low plot ratios in first-tier cities, and most of the residents purchased them in full many years ago. In the past, this group of people had assets, but due to their low incomes, they did not have enough loan repayment capacity and could only be forced to live in a worse environment. But with the reduction of interest rates, their income is already fully able to support the mortgage.

By restarting the monetization of old housing renovation after eight years, on the one hand, it will help expand the base of people who need to improve their housing, and improve the living standards of the whole people. On the other hand, the increase in plot ratio brought about by the old housing renovation will also help local governments increase revenue and improve the balance sheets of city investment.

In short, the core of our thinking is to reduce the willingness to sell existing second-hand houses and use time to exchange space. Once everyone’s expectations of housing price declines are gone, asset prices will begin to reverse, and the biggest short-term risk will also be resolved. But note that our goal is to stabilize the economy, not to fuel the bubble, so on this basis, if housing prices rise, purchase restrictions should be implemented, and sales restrictions should be implemented, and do not relax.

After all, our goal is still to avoid a hard landing of the economy rather than to promote bubbles, and we must not put the cart before the horse.

Next, the second part, protecting growth.

This problem is actually very complex, because economic growth includes investment, consumption, and exports, of which exports involve many international aspects, especially the issue of Sino-US relations. After all, the main subject of this article is the economy, not politics, so I will not go into detail here, but only focus on investment and consumption.

Currently, investment and consumption are sluggish, and these two actually stem from a common problem, which is that there is currently a considerable expectation of deflation, leading to the fact that high-yielders basically don’t invest, and the middle class has also begun to reduce consumption. I know a lot of small and medium-sized business owners with assets of several hundred million yuan. Although their companies’ operations have not been as good as before in recent years, they have some personal savings after working hard for so many years. However, they now prefer to use the money to buy low-risk financial products or even hoard gold and Maotai, rather than investing in company operations or investing in equity projects, or even buying stocks.

At this time, the consumption of this type of people has actually increased. They used to work diligently and save every day, but now they drink Maotai and play golf. However, they are, after all, a very small number of people. This group of people has very limited driving force for the overall consumption, but it is very critical in terms of investment. Once they don’t invest, it will inevitably lead to a decline in the income of the middle class, a decrease in income expectations, and coupled with the expectation of deflation, everyone will naturally increase savings and reduce consumption.

So, to sum up, the overall consumption is still shrinking very badly. And if you look at the financial reports of A-share listed companies in the first quarter, you will find that the most severely declining sector is “the discretionary consumption of the middle class”, such as snacks, etc.

This is also the important point we mentioned in the above text about lowering the LPR, because only in this way will the expectation of inflation arise. Under the current predicament of tightening, appropriate inflation expectations should be welcomed, or even sought after. Refer to the figure below. In the past ten years, the prices of essential consumer goods for Chinese residents, such as rice, flour, meat, milk, and eggs, have increased very little. Considering that internet platforms have reduced the price difference between wholesale and retail, and the price reduction of clothing, electronic products, and other goods, the overall inflation, excluding housing, can be almost ignored. And this also reserves considerable space for our current monetary policy.

Appropriately promoting the return of the consumer price index to marketization is not only conducive to the recovery of asset prices, but will also greatly increase investment willingness—if the current several hundred million yuan in cash is the “ten thousand yuan household” of the 1980s, then even high-net-worth individuals, if they do not continue to invest in developing their businesses, the wealth on paper will be unsustainable. In addition, appropriate inflation will also have some other benefits, such as stimulating everyone to consume in advance, guiding the reasonable depreciation of currency to stimulate exports, and even increasing residents’ willingness to have children (this logical relationship is very complex, and we can discuss it in a separate article if we have the opportunity).

Of course, it is far from enough to stimulate investment only through inflation expectations. We must pay attention to the other two types of investment entities in society, namely state-owned enterprises and local governments. Although both belong to the public ownership economy, the situations are completely opposite. Only by solving their problems can the entire link be completely connected.

The problem with state-owned enterprises is that they have extremely strong financing capabilities and good operating conditions, but they do not have a matching valuation system in the secondary market, which leads to long-term reliance on indirect financing and a lack of direct financing channels, making it impossible to inject “living water” into the market.

I joked with a friend the other day that the so-called “Chinese characteristic valuation” that has been hyped this year is essentially “Chinese special price valuation”—taking the construction industry as an example, similar companies in the world’s top 500, such as France’s Bouygues, Spain’s ACS, and Japan’s Daiwa, basically have a price-to-earnings ratio of around 10 times and a price-to-book ratio of around 1 time, while Chinese state-owned enterprises of the same type, such as China Railway Construction Corporation listed in Hong Kong, have a price-to-earnings ratio of less than 3 times and a price-to-book ratio of only 0.3 times. In terms of growth expectations, I believe that China’s infrastructure level still has considerable market space compared to Europe and Japan; in terms of operating risks, the risks of enterprises backed by national credit and supported by policy banks are obviously lower.

So, “China characteristic valuation” is essentially buying better things at a three-fold or five-fold discount to the international fair price.

What does this have to do with the investment we are discussing? The answer is here. In the past, many state-owned enterprises were listed in Hong Kong, which was a historical legacy of the 1990s when overseas financing was urgently needed. And now, due to the continuous low stock prices below the net asset value per share, the Hong Kong market no longer has the ability to refinance, and due to the average dividend yield of nearly 7% and the Hong Kong dollar-denominated dividends, it has instead led to the loss of state-owned assets and foreign exchange. At this time, if the central government can privatize the state-owned enterprises listed in Hong Kong at a certain premium to the market price, the price will still be far below the net assets, thus realizing the appreciation of state-owned assets. And this part of the equity held by the government does not need to be held for a long time, but can be packaged and pushed to the market in a kind of REITs, and under the current deposit interest rate of less than 2%, the yield of this part of the assets can be as low as around 2%, which can reach 2-3 times the premium of the cost of privatization.

Let’s calculate an account. As of the end of 2021, there were a total of 1,317 state-owned holding listed companies in China, with a total market value of 33.54 trillion yuan. Assuming that companies with serious negative premiums account for 30% (most of them are in Hong Kong), and these companies have an average of 30% non-state-owned shareholders, and the asset package is resold with a premium of 100% after privatization, then the difference income will be as high as 3 trillion yuan. This money is the real increase in state-owned assets.

This will have two very direct positive effects. First, because of the premium of privatization in the Hong Kong stock market, it leads to a profit-making effect in the Hong Kong stock market, and the proportion of foreign capital in the Hong Kong capital market is high, and the generation of the profit-making effect will drive foreign capital to further increase its holdings of Chinese assets, including A-shares. And this will bring a new benefit, which is to increase the common interests of the elite class in the United States with China. You must know that the “American imperialism” that we often criticize is not a monolithic block, and there are also “pro-China factions” and “pro-China factions”, and the “revolving door” in the US political system also determines that the Wall Street system has a very strong influence in Washington.

If Chinese assets represented by Hong Kong stocks and Chinese concept stocks take the lead in warming up, then this part of the force will be more consistent with China’s interests, which is a very important bargaining chip for us to return to the normalization of Sino-US relations in the future.

The second benefit is naturally that the central government has an extra 3 trillion yuan in funds. What will this 3 trillion yuan be used for? It goes back to another market entity mentioned in the above text—local governments. In the past few years, the city investment bond pressure in many cities and counties in the central and western regions has been very high. Using the method of “borrowing new to repay old” and “robbing Peter to pay Paul” to “guarantee public disclosure” is only a temporary measure to quench thirst, and breaking the rigid payment is only a matter of time.

In our view, the current time is precisely the best time to solve the city investment bond problem. For example, the city investment bonds at the county level can be extended for 10-20 years at 50% interest-free or low interest, and the remaining part can be converted into city-level city investment bonds; the city-level city investment bonds can be extended for 5-10 years at 40% interest-free or low interest, and the remaining part can be converted into provincial-level platform bonds; the provincial-level platform bonds can be extended for 3-5 years at 30% interest-free or low interest, and the remaining part can be converted into national bonds. And this 3 trillion yuan of “SOE asset package income” as the balance of the central government’s finances is specifically used to solve the local debt problem.

Through the above-mentioned leverage effect, the city investment bonds of about 14 trillion yuan can be solved, which is similar to the scale of 13.84 trillion yuan of China’s existing city investment bonds as of the end of 2022. In this way, creditors can receive part of the principal on time, local governments get rid of the burden, and everyone is happy.

In other words, the above idea kills two birds with one stone, solving both the valuation problem of state-owned enterprises and the city investment debt problem, and coupled with the LPR reduction mentioned above, the investment capacity and investment willingness of each party have been greatly enhanced.

With the city investment bond problem solved, the annual financing cost of local governments will be greatly reduced, and the surplus funds can be used to do many things. In addition to the monetization of old housing renovation mentioned above, there is also equity finance. In the past one or two years, the difficulty of fundraising in the VC/PE industry has greatly increased. The financing of domestic alternative enterprises in many “chokehold” industries mainly relies on the surplus of investment institutions’ fundraising in the past few years, but this state is obviously unsustainable. Under the background of the socialist market economy with Chinese characteristics, only by organically combining government investment and social investment through equity can the enterprise sector have a stronger investment willingness and ability.

And only when all sectors of the national economy have the ability and willingness to invest and consume can we be qualified to talk about the last point, protecting employment.

The employment problem is the most severe problem in the current situation, and it is also the most difficult problem to solve. If the asset price problem and the economic growth problem are not solved, it is basically impossible for employment to rebound. Currently, the unemployment rate of young people aged 16-24 in China exceeds 20%, which is higher than during the pandemic, and with the continuous development of artificial intelligence technology represented by ChatGPT, the employment suppression of mid- and low-end white-collar workers will only increase.

Of course, we assume that the asset price problem and the economic growth problem can be better solved in the way mentioned above, then the pressure on employment will obviously decrease significantly. Then on this basis, I think there is also a point that is crucial, which is to put the “streamlining administration, delegating power, improving regulation, and providing better services” reform into practice, especially for some enterprises with problems in development, to give them a higher degree of tolerance.

The degree of tolerance here is not indulgence, but based on the principle of “punishing the past and preventing the future, curing the disease and saving the person” rather than the principle of “one size fits all”. If administrative means can be used to solve it, then judicial means should not be used; if it can be solved at the individual level, then it should not be solved at the enterprise level. Take a fictitious example (if there are similarities, it is purely coincidental), a company in a certain province in the central region was shut down due to the alleged violation of law by individual employees, resulting in the closure of the entire company and the unemployment of thousands of people. The law enforcement department’s protection of public interests was a good intention, but in the end, the company went bankrupt, the employees were unemployed, and the government’s tax revenue decreased, and no one was the real winner.

In the future, whether the enforcement of economic cases involving certain national or internet enterprises should take into account the consideration of ensuring employment and maintaining judicial fairness, and whether the tolerance for the expansion of the capital market can be higher and the attitude can be more positive, this concerns whether countless jobs can be guaranteed, and it is also about whether the private economy can regain confidence. State-owned enterprises can do it, private enterprises dare to venture, and foreign enterprises are willing to invest. When we provide strong guarantees for every market entity, we believe that the recovery of employment will definitely come.

Finally, back to our title: It’s time to protect the economy at all costs.

That’s right, every decision has a cost.

If asset prices rise, will it possibly lead to housing prices rising again? If the city investment problem is solved, will new over-investment problems arise? After inflation occurs, will it affect the basic life of low- and middle-income people? Even, if the economic engine restarts, will our wealth gap further increase.

We have the world’s strongest government in terms of governance, the world’s most intelligent leaders, and the world’s most diligent and brave people.

All the costs are for getting through the most difficult and cruel transition period that the Chinese economy will face in the next three to five years. And we also firmly believe that our great motherland will come out of the confidence trough in the near future and step onto a new stage of high-speed development!

Discover more from 自由档案馆

Subscribe to get the latest posts sent to your email.